Latest Stainless Steel Market Dynamics: Nickel Prices Continue to Rise, Indonesia's Tsingshan Chases the Rally, Cumulative Price Increase Nears US$100/MT

April 27th: LME Nickel rose by $15 from the previous trading day. LME Nickel opened at $19,090, reached an intraday high of $19,540, a low of $19,050, and finally closed at $19,140, up 0.08% from the previous trading day. The Middle East crisis sparked economic and demand concerns, dragging metals lower, but LME Nickel maintained an upward trend. The market is mainly concerned that Indonesia's nickel supply is already experiencing a shortage of the sulfur required for nickel production.

On Monday, spot stainless steel prices surged significantly, with the price hike starting ahead of schedule last Saturday. Major news from the raw material side last week ignited bullish market sentiment. On April 23, French nickel company Eramet officially announced that its Indonesian Weda Bay Nickel (PT WBN) mine, affected by a substantial reduction in mining quotas for the year, will officially enter a shutdown and maintenance phase in May. Stimulated by this major news, Shanghai nickel and stainless steel futures initially pulled up strongly, driving spot prices up synchronously. Today, the futures market surged higher again, further boosting spot quotations.

On April 24, Indonesia's Tsingshan raised its export quotation for cold-rolled stainless steel 304 by $30/ton. This price adjustment was mainly because the quota for Eramet's Weda Bay nickel mine in Indonesia will exhaust its full-year allocation in mid-May, after which the mine will enter maintenance and care, triggering expectations of tightening supply. Nickel and stainless steel prices rose in tandem.

After Indonesia's Tsingshan stainless steel 304 rose by about $30/ton on April 24, it was pulled up again by about $60/ton on April 25, after which the steel mill immediately announced a suspension of trading. It is reported that Indonesia's

Tsingshan remained closed for trading on April 27, with a strong wait-and-see sentiment in the market.

On April 27, market trends diverged; the upward momentum of Shanghai nickel slowed down, and stainless steel dipped narrowly after opening high in early trading. As of the close, the SS2606 main contract was reported at US$2269/MT, an increase of 1.29%; the main Shanghai nickel contract was reported at US$22120/MT, an increase of 3.05%.

In the Wuxi area, the mainstream quotation for private 304 cold-rolled 4-foot rough edges was US$2350/ton, up US$67/MT from last Friday; the private hot-rolled price was US$2310/MT, up US$74/MT from last Friday.

Nickel and chromium raw materials strengthened together, directly consolidating the bottom support of stainless steel from the cost side, becoming the core driving force for the upward movement of futures and spot prices in this round.

News from the Indonesian nickel ore market continued to ferment. After the implementation of Indonesia's new HPM (benchmark price) policy, the profit pattern of the nickel industry chain is shifting from downstream smelting to upstream mines — smelting enterprises relying on purchased ore are under cost pressure, while integrated enterprises with their own mines offset the cost impact through internal synergy.

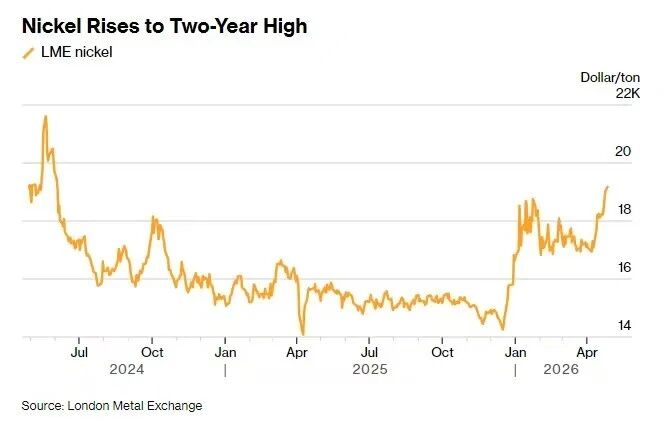

Raw Material: Indonesia's Nickel Ore Quotas Plunge 71%, Nickel Prices Rise to Two-Year High

With major nickel producer Indonesia reducing mining quotas and a global sulfur shortage, the supply outlook for battery metals has tightened, pushing nickel prices to their highest level in nearly two years.

On Monday, nickel prices jumped by as much as 2.6%. Other base metal prices were mixed following reports that Iran had proposed a new plan to the US to reopen the crucial Strait of Hormuz, with traders assessing the possibility of the war ending.

According to a CNBC Indonesia report, affected by Indonesia's cut in nickel ore production quotas and tight global sulfur supplies, international nickel prices recently rose to a near two-year high.

The report stated that Indonesia's Ministry of Energy and Mineral Resources expects to cut the nickel ore production target to about 250 million to 260 million tons this year, lower than the 379 million tons in the 2025 Work Plan and Budget (RKAB).

The Indonesian government previously stated that cutting mineral production quotas is one of the measures to stabilize commodity prices.

Tri Winarno, Director General of Minerals and Coal at Indonesia's Ministry of Energy and Mineral Resources, stated in early April that, up to that point, the Indonesian government had approved about 190 million to 200 million tons of nickel ore production in the 2026 RKAB. He admitted that cutting nickel production is one of the strategies to drive nickel prices back up.

He said: "RKAB approvals are almost complete. For nickel, it's about 190 million to 200 million tons."

Besides the tightening of Indonesia's production quotas, tight global sulfur supplies have also exacerbated market concerns about nickel supply. Sulfur is an important raw material used in the processing of battery metals like nickel and cobalt. Recent unrest in West Asia has disrupted sulfur supplies, driving up related costs and affecting market judgments on the nickel supply outlook.

Indonesia's supply policies have already affected some mining companies. Reuters previously reported that the PT Weda Bay Nickel joint venture project—involving China's Tsingshan Group, French mining company Eramet, and Indonesian state-owned enterprise Antam—had its approved production for 2026 at 12 million wet metric tons, significantly lower than the initially approved 32 million wet metric tons for 2025; the quota for that project in 2025 was later raised to 42 million wet metric tons. Eramet stated it would apply for a quota increase.

Regarding whether production quotas will be relaxed, Tri stated that the government does have a plan for "measured relaxation," but the specific mechanism has not yet been decided. He emphasized that the government will remain cautious when relaxing quotas, because if supply becomes excessive again, nickel prices may fall back.

He said: "This is a supply and demand issue. Once supply is overabundant again, the price will definitely drop again."

According to Trading Economics data, nickel prices rose to their highest level since June 2024. A CNBC Indonesia report indicated that nickel prices once reached $19,350 per ton, the highest level in nearly two years.

Weekly Review of the Chinese Stainless Steel Market (Apr 20th – 24th)

Last week, stainless steel prices in the Wuxi market experienced a "deep V" shape. With the disturbance of overseas macroeconomic sentiment, prices first fell and then rose. As short sellers concentrated on closing positions and exiting, the main contracts for Shanghai nickel and stainless steel welcomed another rally. Tsingshan agents maintained a price-limit shipping policy, and low-priced resources in the market saw hot transactions. As of last Friday, the price of the main stainless steel contract rose by US$15/MT from the previous week to US$2249/ton, an increase of 0.66%.

Stainless steel 300 Series: Futures and Spot Fluctuate Between Red and Green, Strong Bullish Sentiment Before the Holiday

This week, cold-rolled and hot-rolled stainless steel 304 prices operated with fluctuations. As of Friday, the mainstream basis price for private 4-foot cold-rolled stainless steel 304 in the Wuxi area was quoted at US$2280/MT, up US$7/MT from last week; the private hot-rolled stainless steel price was quoted at US$2235/MT, flat compared to last week.

Due to the fermentation of Indonesia's new HPM regulations for nickel ore, the main contract opened high with a gap at the beginning of the week, and under the resonance of futures and spot, the price was reported at US$2280/MT. Subsequently, because Iran explicitly refused to extend the ceasefire, the breakdown of negotiations caused a poor overall sentiment in metals, and the spot price fell slightly by US$7/MT. However, due to weak enthusiasm for downstream procurement, some traders locked in profits, leaving an actual transaction negotiation room of US$7/MT. Towards the end of the week, funds continuously poured into the futures market, the main contract continued to pull up, and the price generally recovered the earlier declines.

Stainless steel 200 Series: Spot Prices Stabilize at High Levels, Stronger Transactions Drive Two Consecutive Weeks of Destocking

This week, futures prices broke through the 15,200 high, market bullish sentiment continued to heat up, and 201 spot prices stabilized at high levels. Agents from Desheng and Beigang quoted Stainless steel J5 at a US$1235/MT basis, and Tsingshan cold-rolled stainless steel 201J2 was quoted at a US$1245/MT, with firm agent quotations. Approaching the weekend, as the futures market returned to highs, the market's willingness to adjust prices was not strong. Looking at inventory, cold-rolled resources were digested quickly during the week, while hot-rolled inventory mainly saw a slight destocking.

Stainless steel 400 Series: Rigid Demand Released, Destocking Pattern Continues

This week, stainless steel 430 prices operated weakly but stably. As of Friday, the quotation for state-owned cold-rolled stainless steel 430 in the Wuxi spot market was US$1265/MT, and the state-owned hot-rolled stainless steel quotation was US$1130/MT, both flat compared to last week's quotations. During the week, the futures market operated with fluctuations, downstream procurement sentiment leaned toward caution, and market transactions were still mainly driven by the release of rigid demand, driving continuous declines in spot market inventory.

Conclusion: Stainless Steel Prices Expected to be Robust in the Short Term

In summary, last week stainless steel spot prices fluctuated with a strong bias. Raw material prices performed firmly. Social inventory continued to be digested, and future pressure was somewhat relieved. Market arrivals slowed down during the week. Downstream demand maintained a normal procurement pace. Going forward, attention should be paid to social inventory situations, raw material prices, and the progress of policy rollouts. It is expected that stainless steel will run strong in the future.

Stainless steel 300 Series: Overall, it is expected that 300 series stainless steel coil prices in Wuxi next week will maintain a volatile and slightly strong trend. The effects of Indonesia's new HPM policy for nickel ore will continue to ferment, ferronickel prices are expected to rise further, and the cost transmission effect will strengthen, supporting stainless steel prices. At the same time, spot inventory is gradually digested, driving the release of demand and alleviating supply pressure.

However, it is also necessary to be alert to the high-level fluctuations of Shanghai nickel prices, as long-short divergences may increase; if a pullback occurs, it will drag down stainless steel prices.

Stainless steel 200 Series: From the raw material side, after copper prices returned to US$15111/MT, the fluctuation range narrowed. Manganese and high-chromium prices remained mostly flat, and high costs provided solid support for spot prices.

With the May Day holiday approaching, phased procurement demand is expected to be released centrally, boosting the 201 market trend. However, continued attention is still needed regarding post-holiday market inventory conditions. If transactions do not keep up with the accumulation rate in a timely manner, under high supply pressure, the market may yield profits to promote shipments, and prices will face downward risks.

Stainless steel 400 Series: Overall, high-chromium prices on the raw material side remain stable, and TISCO's May bidding price for high-chromium steel increased by US$7/50 reference tons month-on-month, forming strong cost support for 400 series stainless steel, with obvious bottom support for spot prices. Currently, the spot market inventory has been destocking for two consecutive weeks, and short-term market inventory pressure has been somewhat alleviated. Moreover, with the May Day holiday approaching, downstream stocking demand may be gradually released. It is expected that short-term prices will run stable to strong, and later focus will be placed on changes in steel mill production scheduling and the release of downstream demand before the holiday.

Sea Freight | Multiple Shipping Companies Issue May Freight Rate Adjustment Notices, Reaching up to $7,200

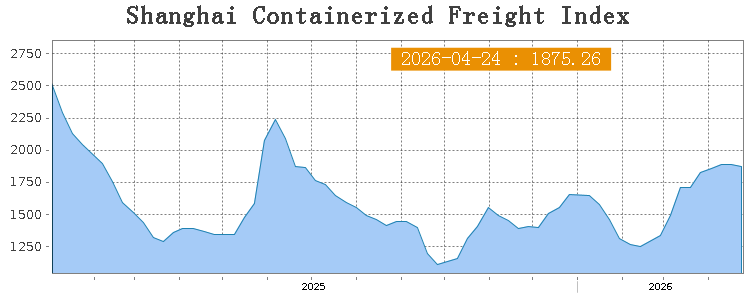

The military conflict in the Middle East continues to maintain a ceasefire, but the future situation still faces significant uncertainty. This week, China's export container shipping market was generally stable, freight rates on most routes fell slightly, and the composite index fell slightly. On April 24, the Shanghai Containerized Freight Index (SCFI) was 1875.2, down 0.6% from the previous period.

Geopolitical conflicts continue to disturb key shipping channels in the Middle East, elongating route transportation times. Comprehensive logistics costs have risen rigidly, and industry operational pressure continues to increase.

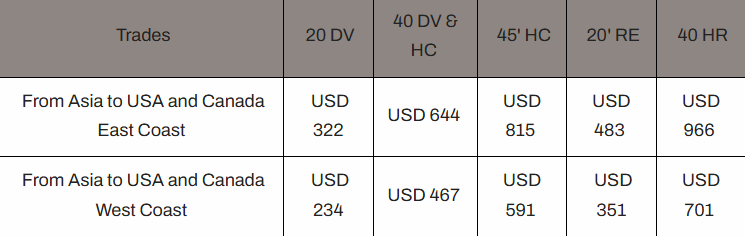

Against this backdrop, top shipping companies have densely announced May price adjustment plans. MSC, Maersk, CMA CGM, and Hapag-Lloyd have issued notices to centrally raise freight rates on multiple routes such as Asia-Europe and Trans-Pacific, while also charging multiple additional fees, with freight rates on some routes reaching up to $7,200.

1. Mediterranean Shipping Company (MSC)

MSC announced it will increase emergency bunker surcharges on routes from Asia to the US and Canada, applicable to all ports from Asia to the US East Coast, US West Coast, and Canada, effective from May 1, 2026 (based on the gate-in date).

2. Maersk (MAERSK)

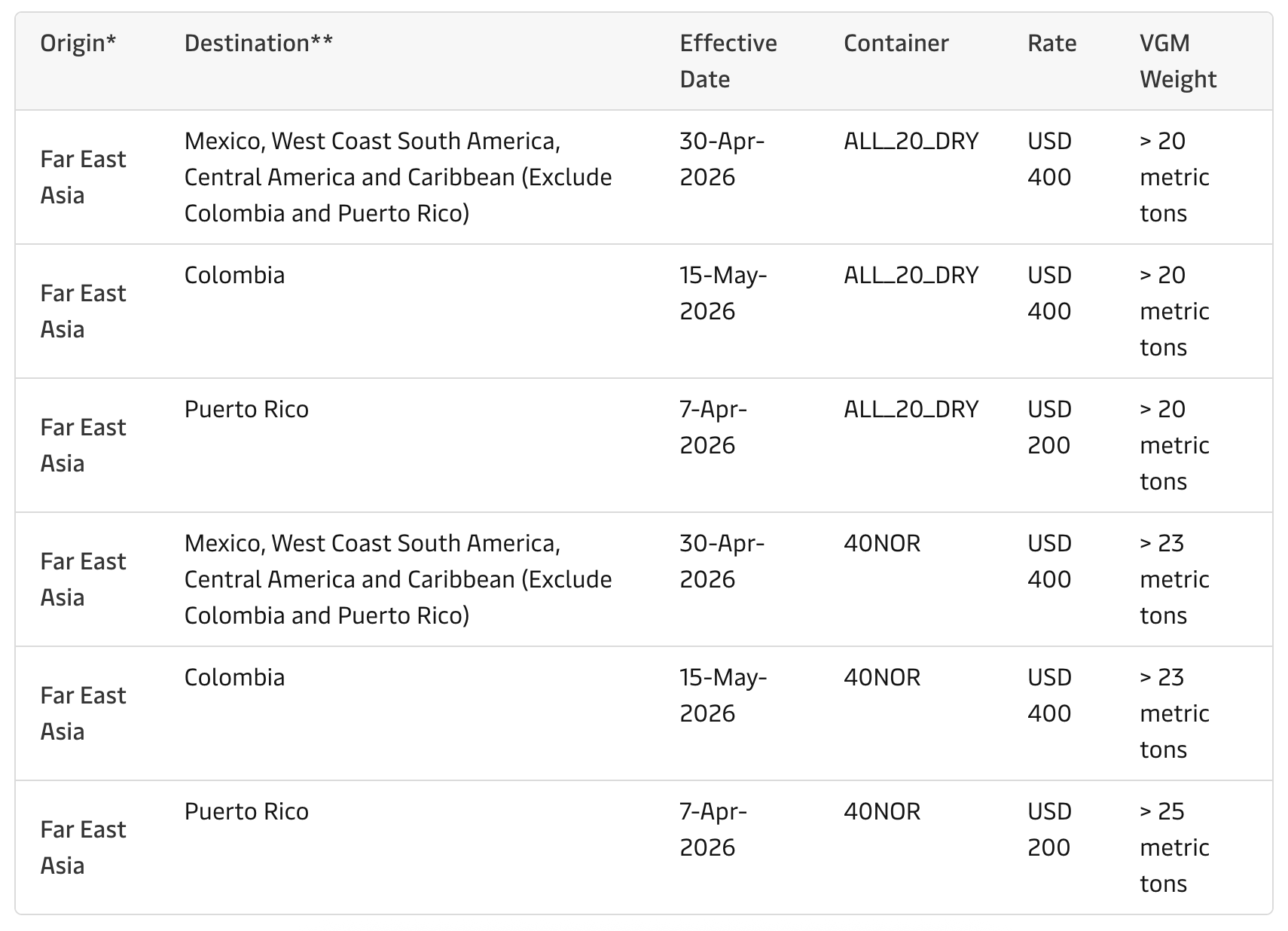

Maersk will adjust the Heavy Weight Surcharge (HWS) for cargo traveling from Far East Asia to Mexico, the West Coast of South America, Central America, and the Caribbean (excluding Colombia and Puerto Rico). For all 20-foot dry containers with a Verified Gross Mass (VGM) exceeding 20 metric tons, and 40-foot non-operating reefers with a VGM exceeding 23 metric tons, the new standard for the heavy weight surcharge will be implemented, with a billing effective date of April 30, 2026.

3. CMA CGM

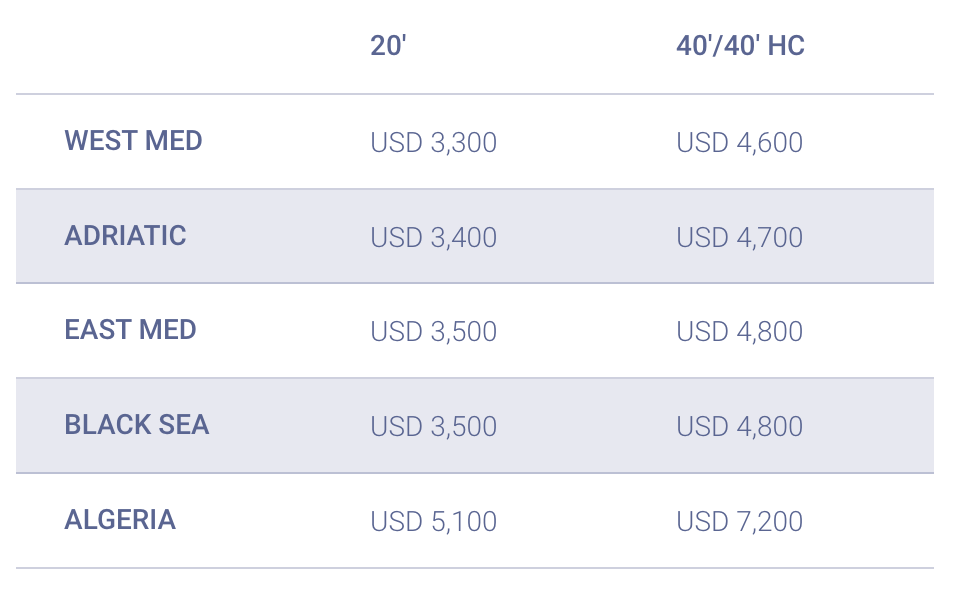

CMA CGM announced an increase in the Freight All Kinds (FAK) rates for various goods from Asia to the Mediterranean and North Africa routes from May 15 to May 31, 2026. This adjustment applies to dry containers, reefers, Out of Gauge (OOG) containers, and paying empties from all major Asian ports to all Mediterranean regional ports (West Mediterranean, Adriatic, East Mediterranean, Black Sea, Algeria).

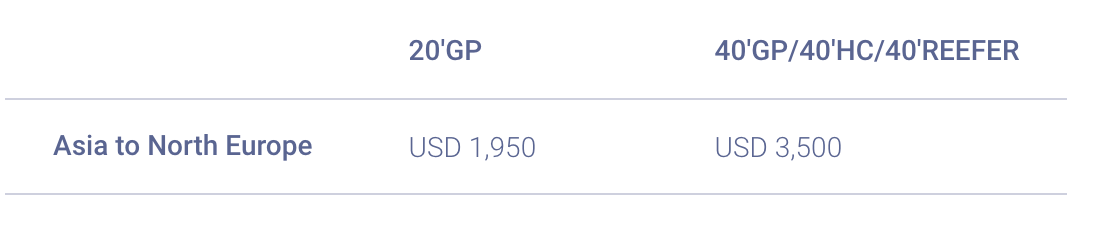

CMA CGM announced that from May 15, 2026 (loading date), until further notice, all Asian ports to all Northern European ports for 20-foot general purpose, 40-foot general purpose, high cubes, and reefers will implement the newly effective Freight All Kinds (FAK) rates. The above are base port to base port freight rates; outports require additional conventional TAO/TAD surcharges.

4. Hapag-Lloyd

Hapag-Lloyd will raise the Freight All Kinds (FAK) rates for various goods on the Far East to Europe routes, applicable to 20-foot and 40-foot dry containers and reefer containers (including high cubes), officially effective for voyages departing from the billing date of May 15, 2026.