TREND || Downstream Demand Falls Short of Expectations; Stainless Steel Shows Weak Downward Trend

Stainless Steel Market Analysis and Trend Forecast (March 16 – March 20, 2026)

Overview: Last week, the stainless steel market generally operated on the weaker side, with the price center of gravity continuing to shift downward and bearish factors dominating. The US dollar index continued to strengthen, exerting significant downward pressure on the non-ferrous metals and stainless steel sectors; cost-side support loosened slightly, weakening its overall backing. Steel mill production schedules in March returned to high levels, resulting in a generally loose market supply. Although social inventories have been depleting for two consecutive weeks, the pace of destocking has been sluggish. The release of rigid downstream demand is insufficient, and purchasing willingness remains weak. Under the weight of multiple overlapping pressures, both the futures and spot prices of stainless steel continued their weak downward trend.

I. Price Trends

(I) Futures Market Nickel prices and stainless steel futures fluctuated and weakened. As of the close on Friday, March 20, the most active stainless steel contract 2603 finally closed at US$2062/MT, marking a cumulative weekly drop of US$18.32, or a decline of 0.88%. The most active Shanghai Nickel contract closed at US$19525, a decrease of 2.75%.

(II) Spot Market

Steel Mill Pricing Policies Tsingshan Steel opened its pricing twice this week. The listed price for the stainless steel 304 dropped by a cumulative US$29/MT, and the stainless steel 316L series dropped by a cumulative US$44/MT.

Specifically: 4-foot Indonesian material was Stainless steel 304 quoted at US$2165/MT (gross base), and 0.6mm and below at US$2180/MT (gross base). The Tsingshan 304 hot-rolled coil futures guidance price was US$2135/MT.

The Tsingshan hot-rolled 316L futures listed price was US$4055/MT. The Yongjin cold-rolled 316L futures listed price was US$4150/MT (gross base).

On Friday, Tsingshan Steel raised its price limit policy for the stainless steel 304 by US$14/MT.

Specifically: The selling price for Hongwang/Shangke/Indonesian material 4-foot 304 shall not be lower than US$2190/MT (gross base); the Tsingshan hot-rolled stainless steel 304 coil price shall not be lower than US$2150/MT.

Spot Performance by Series

Stainless steel 304: Prices retreated from high levels, dropping by US$15-US$29.

Stainless steel 316L: Prices continued their downward trend, dropping by US$29-US$73/MT.

Stainless steel 201: Prices initially rose before falling, exhibiting narrow overall fluctuations.

Stainless steel 400 Series: Prices remained generally stable, with isolated minor reductions of US$7-US$15/MT.

II. Supply and Outlook

Regarding steel mills, production schedules in March have generally rebounded to high levels. Most mills are operating smoothly, and capacity utilization rates remain in a high range, ensuring sufficient overall supply.

Looking ahead to the supply situation in April, considering that the release of current downstream end-user demand remains consistently weak and the traditional peak season is underperforming expectations—compounded by the slow destocking of social inventories—the pressure on the spot market will be difficult to alleviate effectively.

If there is no significant improvement on the demand side moving forward, under this pattern of high supply and weak demand, inventory pressure may gradually be transmitted upstream. It cannot be ruled out that steel mills will flexibly adjust their April production plans based on orders and shipping conditions, which may place a certain degree of suppression on overall supply growth.

Raw Materials | Nickel, Chromium, Molybdenum

High-Nickel Pig Iron (NPI)

Currently, the intended transaction price for high-nickel pig iron has shifted slightly downward to US$161.3/nickel point, a drop of about US$1.47/MT compared to last week. Suppressed by the recent macroeconomic atmosphere, nickel futures have weakened overall. Coupled with strong price-suppression sentiment from steel mills and weak downstream demand for stainless steel, the raw material side's willingness to hold up prices has somewhat loosened.

However, nickel ore supply remains tight. The reduction in Indonesian nickel ore mining quotas, along with rising international oil prices and ocean freight rates, provides strong support for ore prices. The current market trend is primarily characterized by a phased loosening and correction, with limited downside room. At present, the production cost of Indonesian ferronickel is maintained at US$156.45/nickel point, meaning the cost side still provides a floor for ferronickel prices.

High-Carbon Ferrochrome (HC FeCr)

This week, spot quotes for high-carbon ferrochrome remained at US$1268.3/50 Reference tons. The bidding prices of mainstream steel mills for April were raised by US$22/MT/50 reference tons compared to March.

Spot quotes for chrome ore continue to rise, and the current production cost of high-carbon ferrochrome is maintained at US$1252/50 reference tons.

The continuous climb in raw material prices has pushed up smelting costs, plunging ferrochrome enterprises into deep losses. Several iron plants in northern China have announced plans for maintenance and production cuts, shifting the ferrochrome supply from a surplus to a tight balance. At the same time, the purchasing side of steel mills maintains a price-suppressing attitude, resulting in relatively mild increases in April steel bids. In the short term, market sentiment is transmitting from ferrochrome to the mining side; traders have a strong wait-and-see attitude, are cautious in taking deliveries, and exhibit a fear of high prices.

Ferromolybdenum (FeMo)

Recently, ferromolybdenum prices have seen a slight downward adjustment, with mainstream quotes at US$41202/MT, down US$146 from last week's quotes. On March 20, 2026, Dongfang Special Steel's bidding price for ferromolybdenum (60B) was US$4061/MT, a month-on-month decrease of US$366.5/MT from the previous round (acceptance price, quantity: 100 tons).

Suppressed by macroeconomic sentiment in the short term, non-ferrous metals are generally weak, and the wait-and-see sentiment in the molybdenum market has somewhat escalated. However, the tight supply pattern of molybdenum concentrates remains unchanged, and cost-side support remains effective, leaving limited room for a significant downward drop in molybdenum prices.

IV. Market Analysis and Outlook

The current stainless steel market presents an intertwined pattern of suppression from weak macroeconomic factors and demand, alongside strong support from the mining end and ocean freight costs. In the short term, the Federal Reserve's hawkish stance and a stronger US dollar index, combined with rising oil prices, have suppressed nickel prices. Simultaneously, an increased proportion of scrap usage has caused phased loosening on the cost side, resulting in weak, fluctuating stainless steel prices with a downward-shifting center of gravity. However, due to the tightening of Indonesian nickel ore quotas and high international ocean freight rates—coupled with an enhanced willingness among steel mills to support prices following losses—downside room for prices is limited, making a massive trend-driven collapse unlikely.

Moving forward, focus should be placed on two key variables:

1.Indonesia's nickel ore supply policy: The local government aims to complete all RKAB (Work Plan and Budget) application approvals by the end of March.

2.The actual recovery pace of downstream end-user demand: If the mining side remains tight and demand gradually warms up, the market is expected to step out of its weakness. However, if downstream consumption continues to languish, the momentum for a price rebound will be noticeably insufficient.

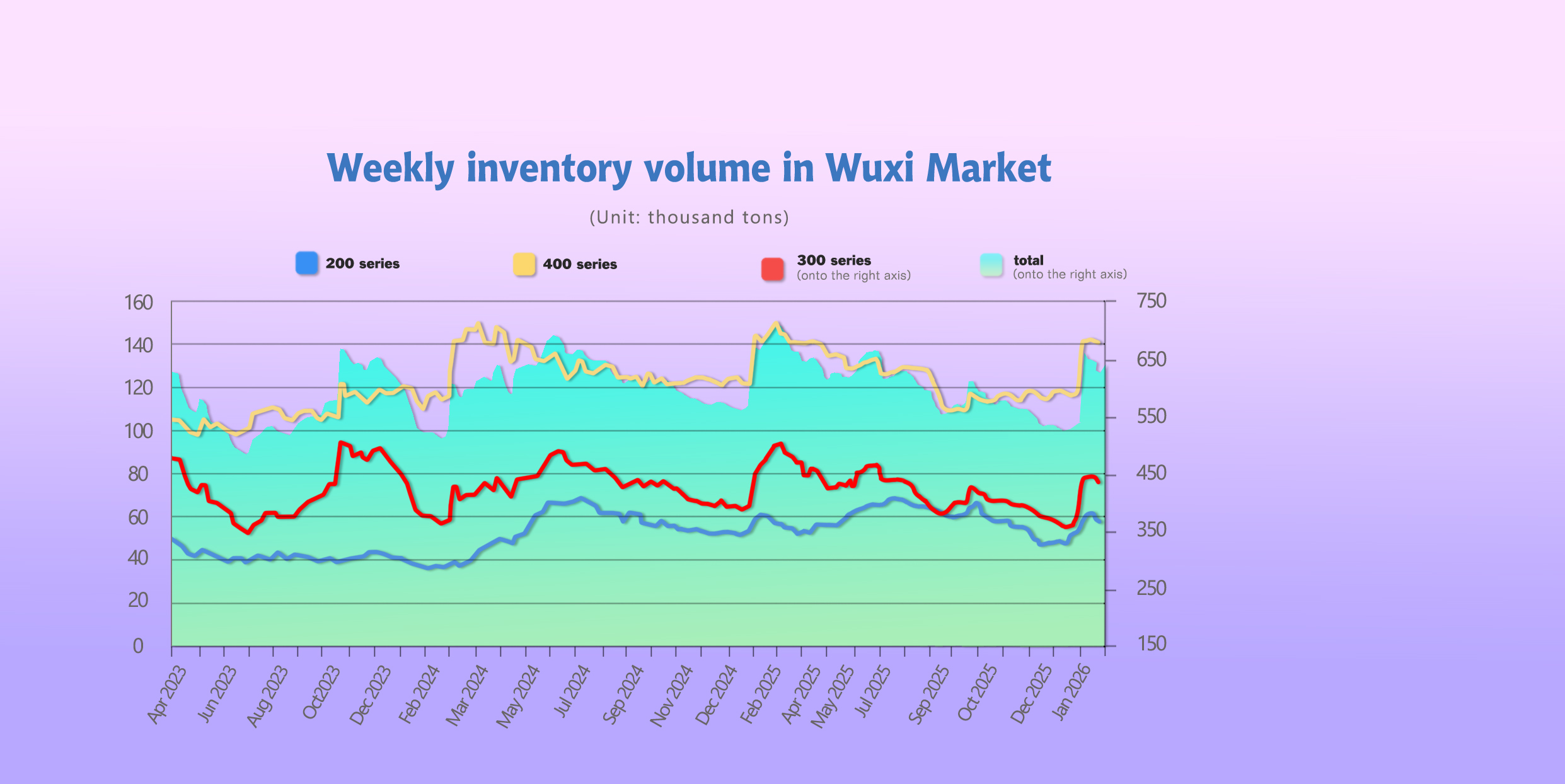

Inventory | Demand Improves at Lower Prices

March 19 News: According to statistics, the total inventory of the Wuxi sample warehouses decreased by 19,000 tons period-on-period. With steel mills opening at lower prices and futures prices falling for four consecutive days, the trading volume of low-priced resources surged, leading to the rapid digestion of front-end warehouse inventories at steel mills.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Mar 12th | 57,616 | 440,376 | 139,879 | 637,871 |

| Mar 19th | 55,156 | 424,770 | 138,829 | 618,755 |

| Difference | -2,460 | -15,606 | -1,050 | -19,116 |

200 Series: Rapid Digestion of Low-Priced Resources

From the perspective of spot inventory structure, Tsingshan, Desheng, and Beigang all maintained a normal arrival pace this week, and both cold-rolled and hot-rolled resources experienced destocking.

Overall, steel mills saw normal arrivals this week, and it will still take time for the high supply pressure following production resumption to fully materialize. After the drop in listed prices, low-priced resources continuously emerged, leaving the demand side mostly in a wait-and-see state. In the second half of the week, influenced by factors such as high raw material costs, steel mills sent price-supporting signals to the market, and spot prices rebounded slightly (by US$0.73/MT ), but actual transactions saw no improvement.

300 Series: Synchronous Massive Destocking of Cold and Hot-Rolled Coils

During the week, the stainless steel futures market closed lower for four consecutive sessions, and the quoted base price for cold-rolled stainless steel 304 dropped to US$2155/MT. As market spot prices continued to fall, bearish sentiment grew downstream, with the majority entering the market to purchase low-priced resources.

Overall, the 300 series inventory saw a massive synchronous destocking of cold and hot-rolled coils this week. On the supply side, the arrival pace of mainstream steel mills slowed down, and the accumulated post-holiday inventory was gradually digested by the market. On the demand side, overall downstream performance was unsatisfactory, and actual transactions remained driven solely by rigid demand.

400 Series: Profit-Yielding Shipments Promote Transactions; Inventory Sees Continuous Slight Destocking

From the spot inventory structure, Jiugang resources arrived normally this week, and the market digested some of Taigang's cold and hot-rolled resources.

This week, the quoted price for cold-rolled stainless steel 430 remained firm. To promote shipments, traders actively yielded profits, leading to an increase in low-priced resources in the spot market. As downstream demand gradually enters the traditional peak season, market trading activity has increased, facilitating a slight destocking of inventory.

During the week, the price of 430 hot-rolled was slightly reduced. The downstream mentality of buying on the dip increased. Coupled with the limited arrival of hot-rolled resources, shortages in certain specifications still exist.

Overall, the current arrival pace of steel mills is normal, but with expectations of a significant increase in steel mill production schedules in March, market supply pressure will persist in the later period. As the downstream sector steps into the traditional peak season, spot market inventories have seen slight destocking for two consecutive weeks. The market supply and demand pattern is expected to gradually improve. Moving forward, continued attention will be paid to the production pace of steel mills and the release of downstream demand.

China's Stainless Steel Exports Drop Significantly in Jan-Feb 2026

The import and export data for stainless steel for January–February has been released. The export volume decreased by over 260,000 tons compared to the same period last year. The volume of Indonesian stainless steel returning to China also decreased synchronously, indicating a weakening in both domestic and foreign demand.

1. Implementation of the new export license policy puts pressure on stainless steel internally and externally. According to customs data, in February 2026, domestic stainless steel imports stood at 109,200 tons, down 16.27% MoM and 31.72% YoY. Cumulative imports for Jan-Feb were 239,700 tons, a decrease of 25.53% compared to the same period last year.

In February, domestic stainless steel exports were 260,000 tons, up 11.78% MoM but down 5.51% YoY. Cumulative exports for Jan-Feb were 492,700 tons, a decrease of 34.77% YoY.

In February, net exports of stainless steel were 150,800 tons, up 47.6% MoM and 30.89% YoY. Cumulative net exports for Jan-Feb were 253,000 tons, down 41.64% YoY.

Starting January 1, 2026, Announcement No. 79 from the Ministry of Commerce and the General Administration of Customs included all stainless steel products (268 HS codes) under export license management. Customs clearance is prohibited without a license, requiring enterprises to build compliance systems from scratch. Regarding the license approval process, some clients reported it takes 1–3 working days, while others reported 1 to 2 weeks. This led to widespread delays in customs declarations and shipments in Jan-Feb, extending order cycles. Coupled with the concentrated "rush to export" by many enterprises in December 2025, stainless steel exports in Jan-Feb of the new year plummeted year-on-year.

2. Imports from Indonesia rank first, followed by Japan and Vietnam. In Jan-Feb 2026, cumulative imports of stainless steel from Indonesia were 199,800 tons, down 27.35% YoY. Among them:

Wide cold-rolled: Jan-Feb imports were 159,300 tons, a cumulative YoY decrease of 17.83%.

Wide hot-rolled coils: Jan-Feb imports were 28,300 tons, a cumulative YoY decrease of 17.64%.

Other and semi-finished products: Jan-Feb imports were 12,200 tons (including 11,800 tons of billets and 300 tons of slabs), a cumulative YoY decrease of 73.96%.

Tsingshan actively adjusted its export strategy, reducing shipments to China and diverting stainless steel resources to neighboring Asian markets. During the same period, Indonesia's exports to Taiwan (China), India, and Vietnam all rose significantly month-on-month.

3. Indonesia Tsingshan's exports of 304 hot-rolled white coil to Taiwan surged by 199%. According to the latest customs data, in February 2026, Taiwan (China)'s imports of 304 hot-rolled white coil (pickled coil) from Tsingshan, Indonesia, reached 19,958 tons in a single month—a staggering 199.5% surge from January, hitting a five-month high. Meanwhile, the import volume of billets, an upstream raw material, was halved to 6,627 tons, and black coils also fell slightly to 39,592 tons.

This shift occurred because mainland China's stainless steel exports in Jan-Feb significantly slowed down due to the new export license policy, causing some international orders to temporarily shift to Taiwan. To meet delivery deadlines, manufacturers abandoned long-process production and turned directly to procuring hot-rolled white coils.

According to feedback from multiple traders and processing plants, in Jan-Feb 2026, affected by mainland China's new export license policy, some 304 cold-rolled and white coil orders could not be shipped on schedule. Some end-customers in Europe and the US turned to Taiwanese manufacturers for inquiries.

However, starting production from billets requires multiple processes such as hot rolling, annealing, pickling, cold rolling, and finishing, which takes far longer than the customer's delivery window. Therefore, Taiwanese processing plants opted to directly purchase 304 hot-rolled white coils produced by Tsingshan, Indonesia. These require only simple cold rolling and surface treatment before delivery, perfectly matching the pace of urgent orders.

A. Mainland China's exports are under obvious pressure. The export license effectively curbed the previously prevalent "buying documents for export" behavior. After the concentrated "rush to export" in December 2025 overdrew demand, export volumes in Jan-Feb experienced a cliff-like drop, and some orders were forced to be delayed or canceled due to the inability to obtain licenses in time.

B. Taiwan quietly absorbs the spillover demand. According to statistics from relevant departments in Taiwan province, China, exports of metal products in February 2026 grew by 9.7% YoY, with exports of stainless steel products to the US, Europe, and Vietnam growing by 12.3%, 8.9%, and 15.6%, respectively.

C. Tsingshan, Indonesia, has become a key supply pivot. As one of the few global manufacturers capable of mass-producing high-quality 304 hot-rolled white coils, Tsingshan Indonesia's February quote to Taiwan was approximately US$2030/MT—roughly US$132/MT lower than similar South Korean products—with stable delivery times.

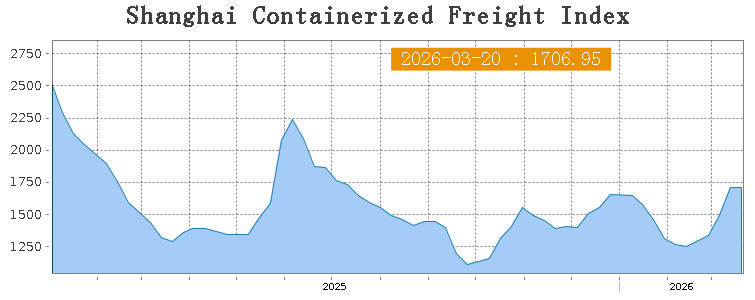

SEA FREIGHT | Geopolitical tensions persist

Last week, the China export container shipping market continued to face the test of tense geopolitical situations. The transportation markets of related routes were greatly affected, while the rest of the routes showed a divergent trend under the influence of the supply and demand fundamentals. The overall index slightly declined.

On March 20th, the Shanghai Containerized Freight Index (SCFI) fell 0.2% at 1706.95 points.

Europe/ Mediterranean:

On March 20th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1636/TEU, which increased by 1.1%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$2784/TEU, which was lifted by 4.4% from previous week.

North America:

On March 20th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$2054/FEU and US$2922/FEU, reporting 8.7% and 6.1% loss accordingly.

The Persian Gulf and the Red Sea:

On March 20th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf increased 3.2% to US$3224/TEU.

Australia & New Zealand:

On March 20th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand decreased by 0.5% to US$621/TEU.

South America:

On March 20th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports fell by 4% to US$2457/TEU.