As we approach the end of 2025, it’s essential to reflect on what has been a challenging year marked by controversial taxes, various protective measures, and volatile geopolitical factors. The stainless steel market in 2025 has seen lackluster performance, making it difficult for stakeholders to predict the long-term trend amid ongoing uncertainties and disruptions.

Looking ahead to 2026, we anticipate that Chinese stainless steel prices will remain relatively flat, similar to 2025. It is expected to be an even more challenging year for the Chinese stainless steel market, facing increased export resistance, backlash from the domestic real estate and construction sectors, and the need for industry upgrades due to overcapacity.

In this article, we will first review the price performance of stainless steel in 2025 and the factors contributing to it. We will also examine the demand and supply outlook for 2026 and discuss potential effects on the future of stainless steel prices.

2025 Price Performance: A Market Under Pressure

Stainless Steel

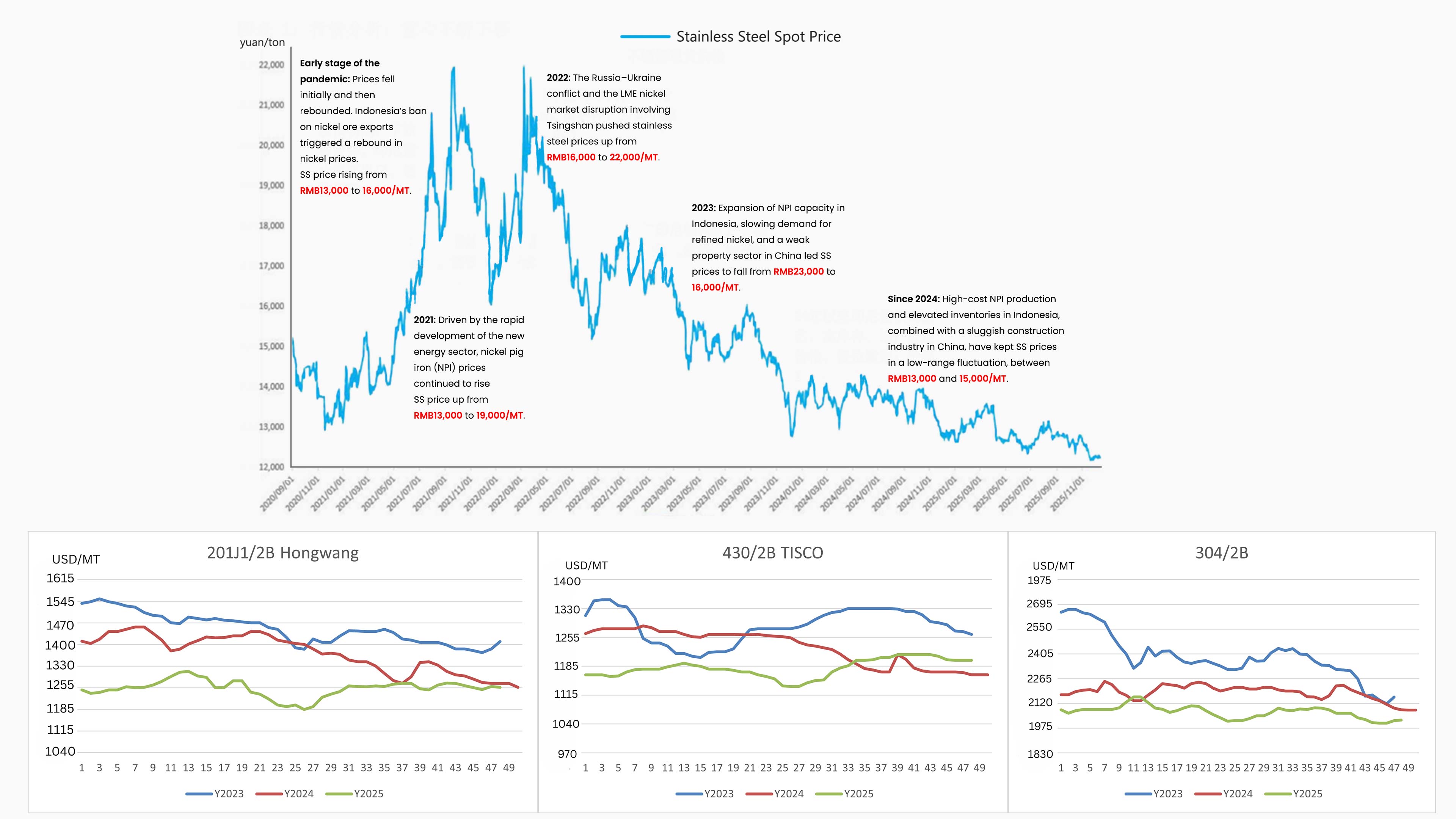

In the past year, all major grades of stainless steel have remained in a stable trend and lower price range with small fluctuations. Take stainless steel 304/2B as an example, the average price is 13648/MT, the highest weekly average price was 14250/MT, in week 11, while the lowest was 13200/MT, in week 45. The fluctuation was comparatively smaller than the prices in 2024 and 2023. The situation is similar in Grade 201 and Grade 430.

Restricted by production costs, steel producers moved between the profit margins and suffered a loss of profit; the stainless steel price appeared flat; however, market sentiment swung significantly and was very cautious under the rapidly changing trading environment.

Stainless steel price hit bottom in 2025.

Market Disruptor

Stainless steel market sentiments swung, every stakeholder are becming more cautious in buying. Among all the reasons, Trump is for sure the biggest disruptor.

In 2025, the U.S. significantly expanded its steel import tariffs on Chinese stainless steel under Section 232, raising rates from 25% to 50% and eliminating exemptions, while continuing product-specific anti-dumping investigations that add further duty layers on select Chinese steel categories.

The US tax on stainless steel is only a direct influence. Broadly, it causes larger ripple effects on the manufacturing sectors that use stainless steel, such as home appliances, interrupting the global trade flow. Not only the material supply but also the end products were both suspended.

The political and economic relations were extended to other countries, like Canada, following the US’s suit: Canada implemented a 25% surtax specifically on steel goods “melted and poured” in China and introduced tariff rate quotas with 50% surtaxes for imports above quota levels. Various anti-dumping and countervailing duties against steel imports—including products from China—added further trade barriers in 2025.

Changes and abruptions coming one after another, renewed trade policy uncertainty increased buyer hesitation. Political risk became a pricing consideration because it is difficult to make long-term plans, so long-term contracts declined while spot trading increased. To the market, policy signals amplified market volatility without improving demand.

The Core Structural Issue: Global Oversupply

Supply: Stainless steel capacity remaining large

- China

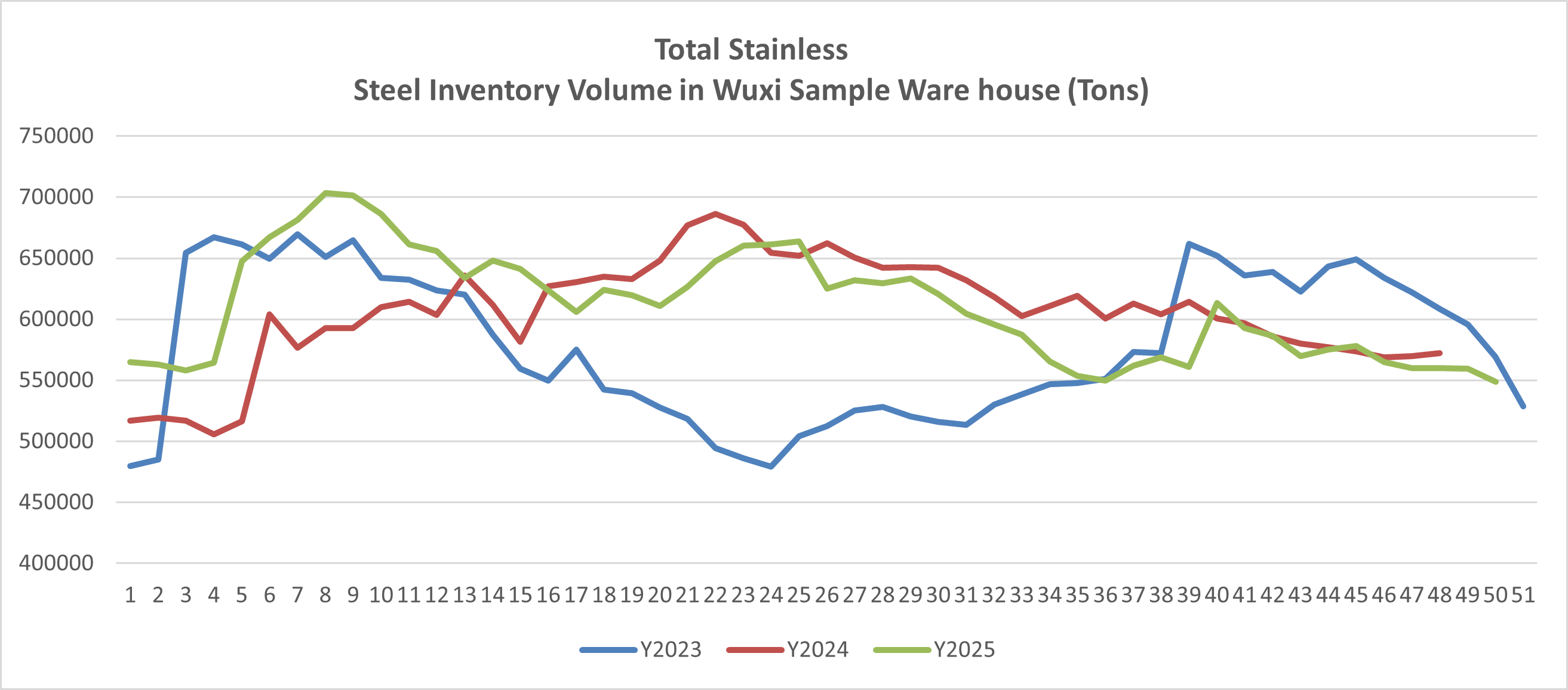

In 2025, stainless steel inventory levels in Wuxi reached record highs, prompting producers to seek production reductions. However, such adjustments proved difficult. High installed capacity and production rigidity made output cuts costly. On the other hand, due to the policies back and forth, the supply chain became more fragile and insufficient. Trading fluency was so restricted by the policy, and the digestion of the capacity was uneven on time record.

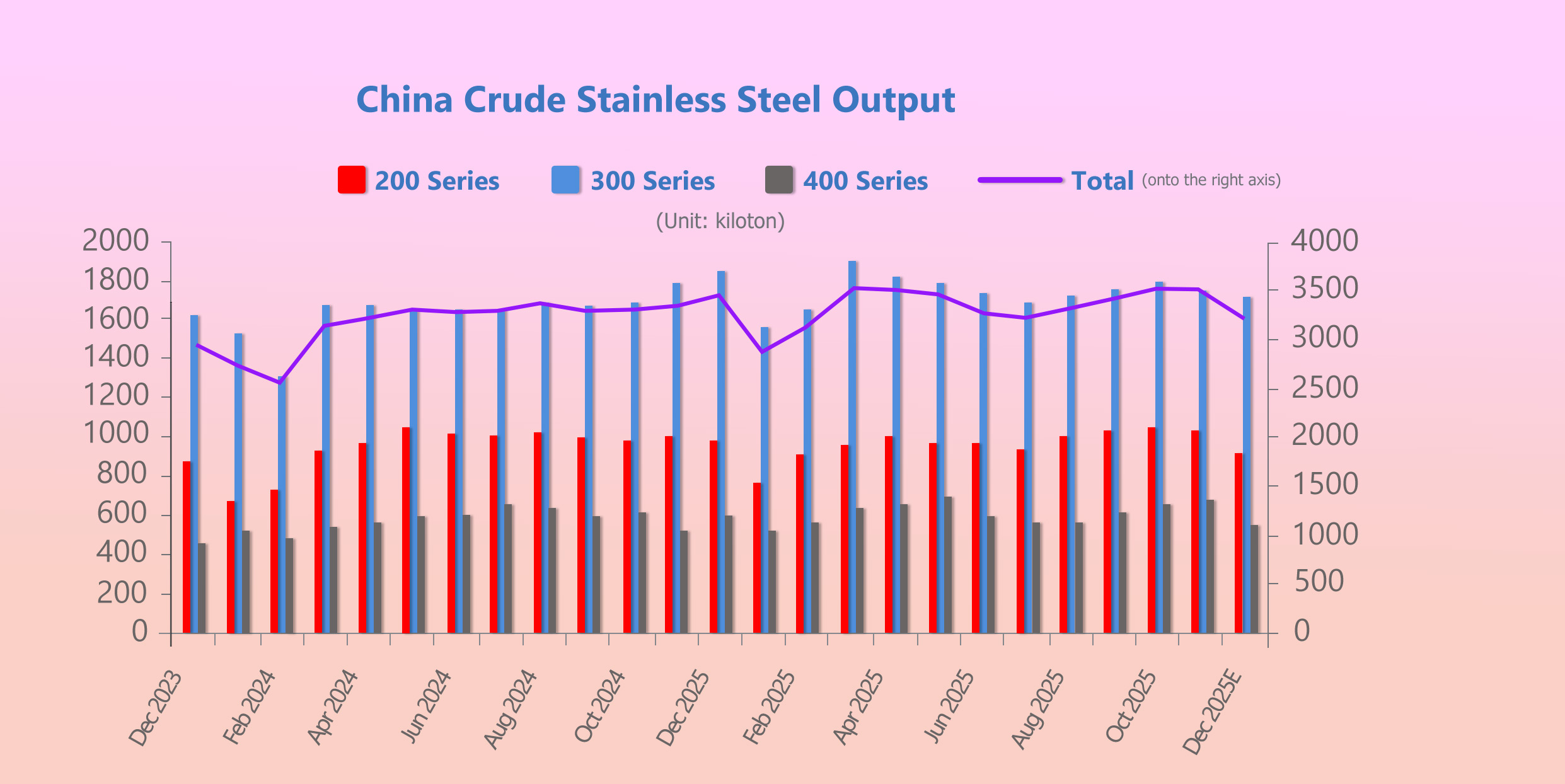

Stainless steel mills conciously reduced the production in 2025, yet output remained large

Despite policy signals to reduce output, operational and cost realities limited the effectiveness of production cuts.

According to statistics, in November 2025, crude stainless steel output from major Chinese producers reached 3.5 million tons, down 110,000 tons month-on-month but up 40,000 tons year-on-year. Of this total, the 200 series accounted for 1.09 million tons, the 300 series for 1.77 million tons, and the 400 series for 650,000 tons.

From January to November 2025, combined stainless steel crude steel output in China and Indonesia reached a record 44.57 million tons, (39.94 million tons produced in China + 4.64 million tons produced in Indonesia), up approximately 2.61 million tons year-on-year.

“In the same period of 2024, it was 41.96 million tons (37.39 million tons in China + 4.57 million tons in Indonesia).”

Noticing the overcapacity, Beijing advocated that the industry reduce production, and the policy is known as “anti-innovation” to push the enterprises to upgrade the production mode. By any means, perhaps steel mills suffered a loss, or it seems that the policy is making an effect, as in quarter 4 of 2025, the steel mills cut off the output, and spot inventory obviously fell.

Destocking is the theme of the stainless steel industry in China in 2025

Demand: Weakness at Home and Abroad

- Americas & EU

In the Americas and the European Union, stainless steel demand in 2025 was primarily shaped by policy frameworks rather than pure economic cycles. Trade remedies such as anti-dumping duties, safeguard measures, and stricter carbon-related regulations are significantly influencing purchasing behaviors.

Policy compliance outweighed price considerations in procurement decisions.

As a result, demand in these regions remained relatively stable but inflexible. Buyers prioritized supply security, regulatory compliance, and carbon exposure management, leading to disciplined procurement behavior and limited tolerance for volume expansion, even when global prices softened.

- Middle East & Southeast Asia

The Middle East and Southeast Asia emerged as relatively less-restricted and more price-sensitive markets for stainless steel in 2025. Compared with Europe and the Americas, these regions featured fewer trade barriers and greater flexibility in sourcing, allowing them to absorb incremental supply from China and Indonesia.

Demand in these markets was closely linked to construction activity, infrastructure development, and manufacturing investment, resulting in higher volatility but also stronger short-term responsiveness to price movements. While these regions provided important outlets for excess global supply, purchasing behavior remained opportunistic, with demand fluctuating alongside project timing, financing conditions, and regional policy adjustments.

These regions provided important outlets for excess supply, but demand remained opportunistic rather than structural.

Construction, manufacturing, and consumer power are the three major standards to measure demand for stainless steel.

- China Domestic Demand

The real estate and construction industry in China has not yet recovered from the collapse. The related downstream manufacturing was in gloomy demand. During the first half of the year, thanks to the government’s support, the comsumption in home appliances was strong. However, as the domestic demand was released in an advanced way, and the financial support faded away, people’s purchase demand diminished. Opinion has it that the governmental support is only a one-batch stimulus, which will consume the actual demand too quickly. From the data published, Chinese consumer power is expanding, yet the pace is shrinking.

This policy aims to solve the problem of overcapacity in the primary industries, like STEEL.

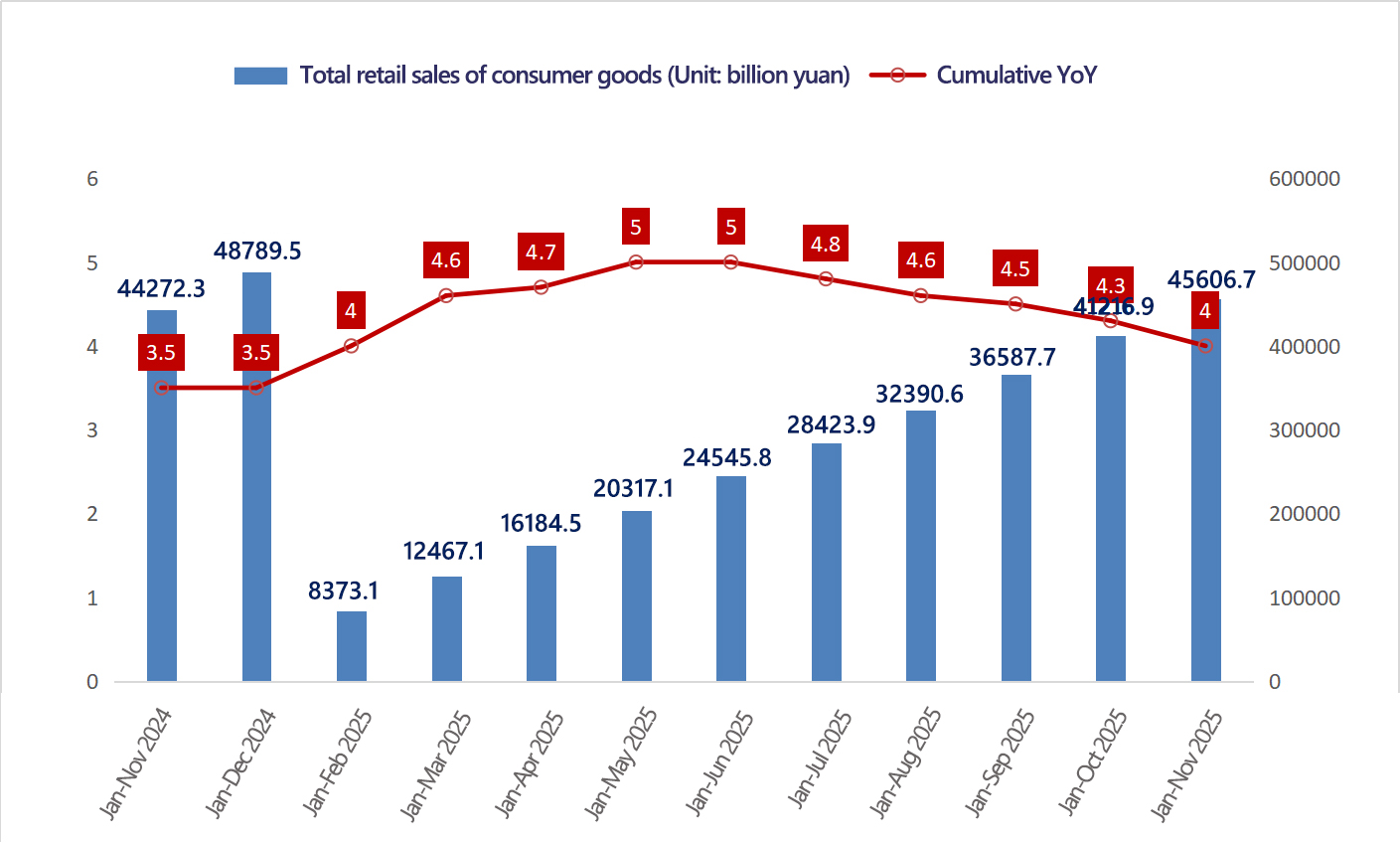

“According to data from the National Bureau of Statistics, from January to November, China's total retail sales of consumer goods reached 45.61 trillion yuan, a year-on-year increase of 4%, which is lower than the 4.3% growth rate in the first ten months, marking the fifth consecutive month of slowing growth.”

Chineses consumers have slowed down in purchasing in 2025.

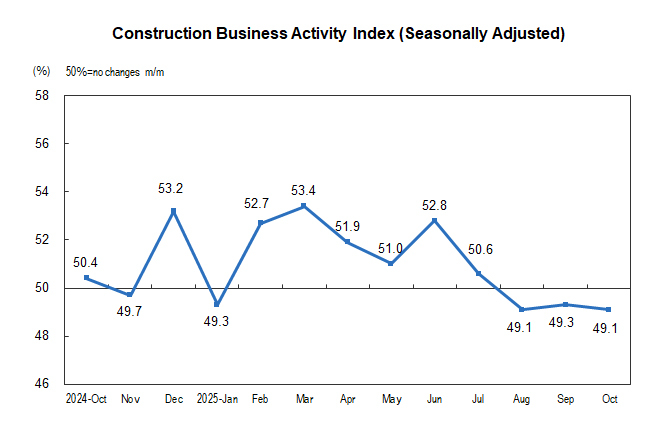

Construction index points to a shrinking momentum in the indistry in 2025.

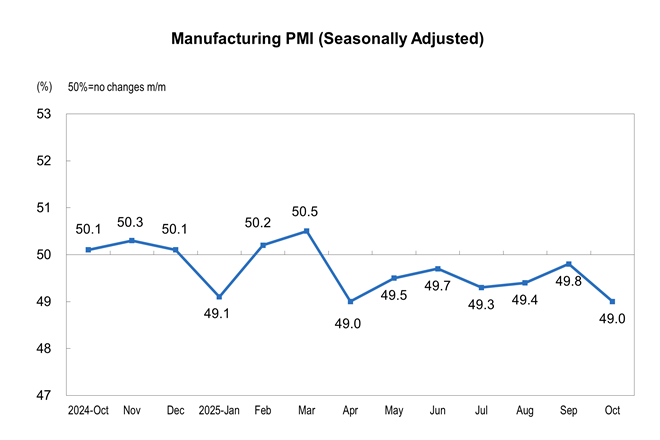

8 out 12 months in 2025, Chinese manufaturing PMI remained in contraction zone.

World: Who are the top buyers of Chinese stainless steel in 2025

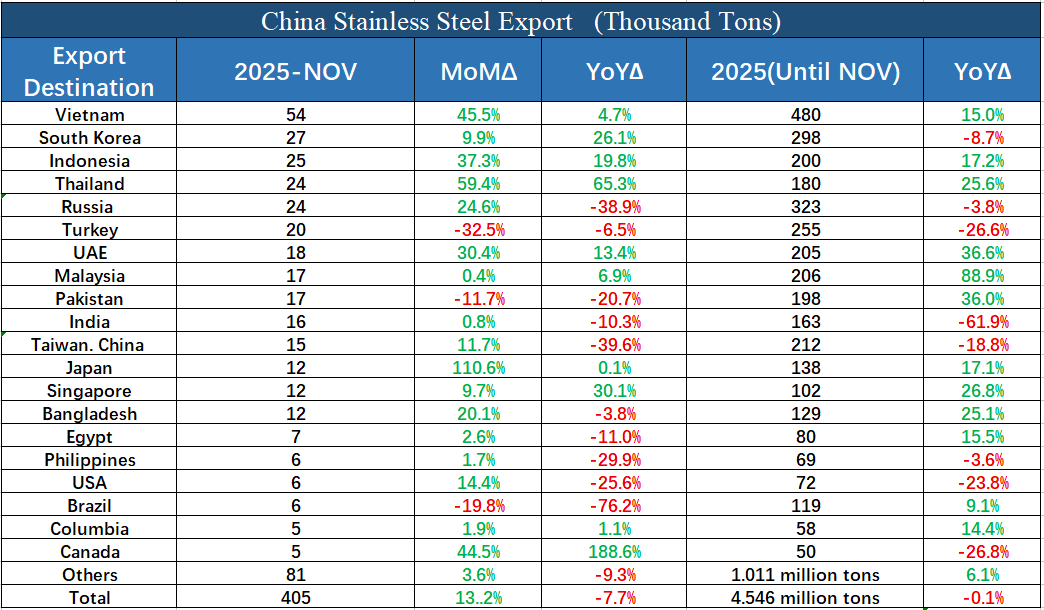

China’s stainless steel exports rose 13.2% month-on-month in November 2025

In November 2025, China’s stainless steel exports reached approximately 405,300 tonnes, representing an increase of 47,200 tonnes month-on-month, or +13.2%. On a year-on-year basis, exports declined by 34,000 tonnes, down 7.7%.

For the period from January to November 2025, cumulative stainless steel exports totaled around 4.55 million tonnes, broadly flat year-on-year, with a marginal decline of 0.1%.

Tax barriers caused large decreases in trading, eg. Turkey, USA and Canada.

Notably, exports to Southeast Asia reached a historical high in November. Volumes rose by 33,700 tonnes month-on-month to 141,000 tonnes, marking a 31.5% increase. Compared with the same period last year, exports to the region increased by 15,700 tonnes, up 12.6%.

Export growth became increasingly concentrated in regions with fewer trade barriers and higher price sensitivity.

Cost Structure and Price Floors

Since demand has remained sluggish, market sentiment was gloomy because of the negative trading policies, and stainless steel prices have stayed low throughout the year. The production cost becomes the fundamental reason for the stainless steel price changes. The production cost is closely related to iron materials, like NPI (Nickel Pig Iron), which forms the price floor and support of the stainless steel.

In a weak-demand environment, cost structure — rather than demand recovery — becomes the primary price anchor.

Indonesia is the biggest supplier of NPI.

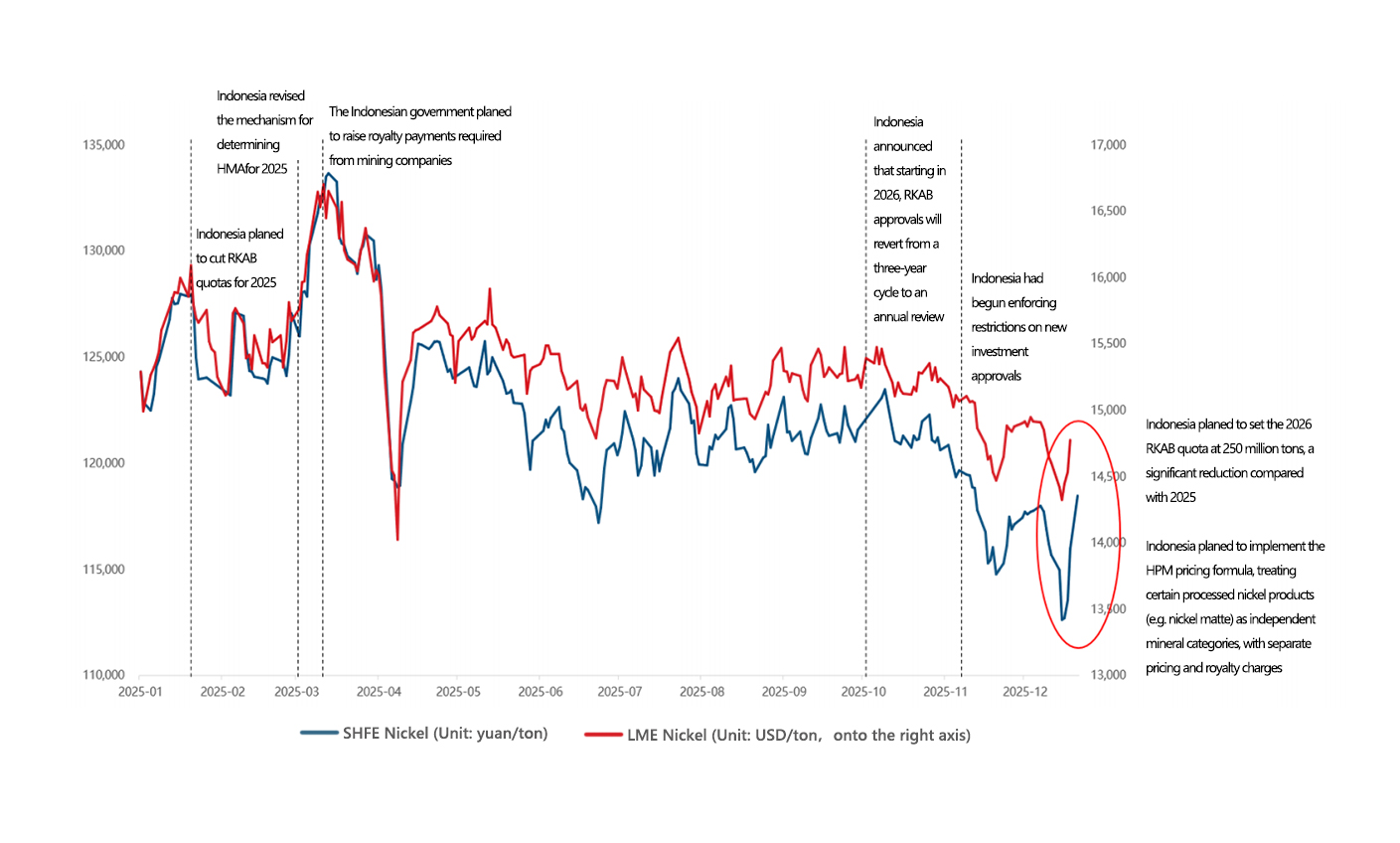

Indonesia’s RKAB system, which governs annual mining production approvals (which were required once every three years), became a more active supply management tool in 2025. Tighter RKAB allocations signaled the government’s intention to moderate nickel output growth and address prolonged price pressure, reinforcing Indonesia’s role in shaping the global cost structure of nickel and NPI rather than merely expanding volume.

The price of NPI in China last year experienced an “M” shape and now hits bottom, which adheres to the price trend of SS304 in 2025.

The prices of SS 304 and NPI have a close relation.

NPI: We tend to think NPI will be the more fundamental instructor of stainless steel prices rather than LME Ni

Indonesia's 2026 RKAB quota plan is 250 million tons, a significant decrease from the 379 million tons set for the 2025 RKAB, but the final implementation method remains unclear. Compared to the quota reduction, the Indonesian government often appears more "out of control" when dealing with RKAB approval issues.

Jakarta's implementation of RKAB greatly influenced the t tendency of LME and ShFE nickel.

Regarding the RKAB approval dynamics in early 2025: Indonesia initially stated that the RKAB quota for this year was set at 298 million tons, and indicated that further reductions might be possible in the future; however, in reality, the 2025 Indonesian RKAB quota reached 364 million tons, even exceeding market demand expectations. At the beginning of Q4 2025, Indonesia announced that it would revert the RKAB approval system from a three-year cycle back to an annual cycle, and all previously applied-for 2026 RKAB quotas would be invalidated. This repeated policy change further exacerbated market uncertainty.

Currently, due to policy instability and declining expectations for stainless steel demand, data shows that Indonesia's nickel production in November 2025 decreased by 2.4% month-on-month, pushing its domestic idle capacity ratio to 16.1%, a new high since March 2024. The production cuts were mainly concentrated in low-grade nickel pig iron (NPI) and high-quality ferronickel, with both related sub-indices recording declines. As the core source of global NPI supply, Indonesia's NPI sector production decreased by 2.1%. Although Chinese NPI activity rebounded during the same period, it was insufficient to offset the overall shortfall, leading to a further increase in the global NPI idle capacity index.

2026 OUTLOOK

The Global Economy Is Forecast to Post ‘Sturdy’ Growth of 2.8% in 2026

Goldman Sachs Research projects global GDP to increase 2.8% in 2026 (versus the consensus forecast of 2.5%). US economic growth is expected to accelerate to 2.6%, while China’s GDP expands 4.8% as strong exports outweigh sluggish domestic demand. Despite longer-term challenges, our economists predict the euro area economy will increase 1.3%, owing to fiscal stimulus in Germany and strong growth in Spain.

For 2026, the World Manufacturing PMI is expected to show continued volatility, with forecasts suggesting a slowdown in industrial output growth (around 1.9%) from 2025, driven by persistent trade uncertainty, tariffs, and policy risks, though some regions like the US might see stronger growth, while key events like the USMCA review in July 2026 pose significant upside or downside risks, with overall trends leaning towards cautious optimism for a short-lived downturn and gradual rebound.

Macro conditions suggest resilience, but industrial growth remains fragile.

Stainless Steel

Let’s be optimistic: Looking ahead, changes in overseas tariff policies and geopolitical risks remain key variables. The EU market, in particular, faces rising green trade barriers, with CBAM scheduled for full implementation in 2026. This will restrict transshipment trade and is expected to increase the cost of Chinese stainless steel exports.

However, at present, China’s stainless steel exports are primarily concentrated in Asia and other emerging markets. As industrialization continues to accelerate in these regions, demand for stainless steel is likely to keep growing. Meanwhile, stainless steel prices have remained at relatively low levels in recent years, improving cost competitiveness. As a result, China’s stainless steel exports may still remain at a relatively high level.

“These factors may support volumes, but not necessarily pricing power.”

Let’s be stoic: Oversupply pressure in the nickel stainless steel market is expected to intensify rather than ease. Indonesia’s RKAB remains a key variable affecting nickel supply, but even if quotas are reduced in 2026, capacity ramp-ups from already-approved projects will continue. This makes it difficult to fundamentally alter the overall supply expansion trend.

“Supply discipline remains the key missing variable.”

Final Outlook: The persistent oversupply could lead to new price lows. Demand recovery is unlikely in the short term, and stainless steel prices are expected to remain in a prolonged bottoming phase.

For market participants, 2026 is likely to be a year focused more on risk management than expansion.