WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,005 | 0 | 0.00% |

| Foshan | 2,035 | 0 | 0.00% | ||

| Hongwang | Wuxi | 1,915 | 0 | 0.00% | |

| Foshan | 1,930 | 4 | 0.24% | ||

| 304/NO.1 | ESS | Wuxi | 1,845 | 10 | 0.58% |

| Foshan | 1,850 | 10 | 0.58% | ||

| 316L/2B | TISCO | Wuxi | 3,585 | -14 | -0.41% |

| Foshan | 3,610 | -27 | -0.77% | ||

| 316L/NO.1 | ESS | Wuxi | 3,385 | -11 | -0.35% |

| Foshan | 3,405 | -26 | -0.78% | ||

| 201J1/2B | Hongwang | Wuxi | 1,250 | -6 | -0.50% |

| Foshan | 1,260 | 1 | 0.12% | ||

| J5/2B | Hongwang | Wuxi | 1,135 | -6 | -0.56% |

| Foshan | 1,145 | 1 | 0.14% | ||

| 430/2B | TISCO | Wuxi | 1,200 | -1 | -0.13% |

| Foshan | 1,200 | -3 | -0.26% |

TREND | Stainless Steel Prices Halt Decline

Expectations for a Federal Reserve interest rate cut have strengthened. During the week, the non-ferrous metals sector continued to rise, and stainless steel prices saw a slight increase last week. As of the close on December 5th (Friday), the main stainless steel contract 2601 was reported at US$1905/MT, up US$19.25/MT from the previous week, a weekly increase of 1.09%. The main Shanghai Nickel contract rose 0.61% during the week to US$17040/MT.

Stainless steel 300 Series: Futures Prices Rise, Market Sentiment Improves

Last week, the stainless steel 304 market price remained stable. As of Thursday, the mainstream base price for Wuxi private cold-rolled 4-foot sheets was reported at US$1875/MT, flat compared to last Thursday; private hot-rolled stainless steel prices were reported at US$1845/MT, up US$7/MT from last Thursday. Early in the week, stainless steel prices stopped falling and rebounded, market transactions warmed up, and inventory depletion among traders and agents was obvious. Later, gains in the futures market narrowed, and downstream procurement focused mainly on restocking for rigid demand, resulting in a generally flat transaction pace.

Stainless steel 200 Series: Futures Rise Boosts Sentiment, Transaction Atmosphere Improves

The stainless steel futures market was generally strong last week, while stainless steel 201 prices showed mixed movements. Early in the week, some traders offered concessions on cold-rolled stainless steel J2 down to around the 6,950 base to promote sales. As the futures market bottomed out and rebounded, the willingness to offer further spot price concessions diminished, and the transaction atmosphere became active. According to market feedback, spot resources for cold-rolled stainless steel 201J1 are currently scarce, with stockouts in some thin-gauge specifications. In the second half of the week, futures maintained an upward trend, boosting market confidence; on Friday, prices were raised by 50 to a 7,000 base for shipment, and downstream purchasing increased slightly.

Stainless steel 400 Series: Downstream Demand Hard to Boost

Prices for stainless steel 430 ran weak last week. As of Friday, quotes for state-owned cold-rolled stainless steel 430 in the Wuxi spot market were at US$1205/MT, down US$7/MT from the previous week; state-owned hot-rolled stainless steel quotes were at US$1085/MT, flat compared to the previous week. During the week, the futures market fluctuated repeatedly, and market sentiment remained cautious, with most taking a wait-and-see approach regarding the future market. Traders mostly offered concessions to move inventory and relieve pressure; actual transactions had room for slight concessions. However, constrained by the traditional off-season for consumption, overall downstream demand was weak, and inventory digestion in the spot market was slow.

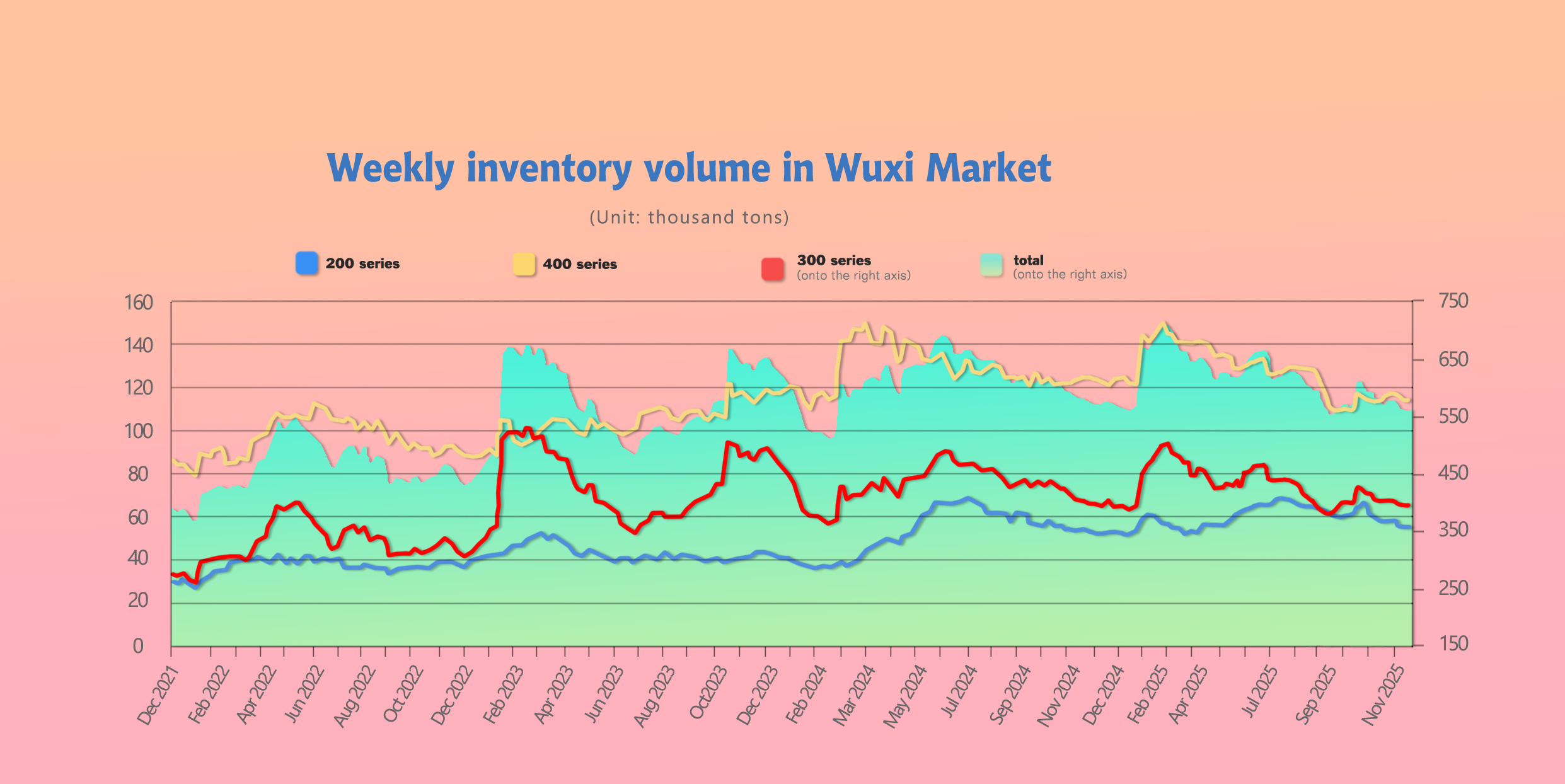

INVENTORY | Stainless Steel 300 Series Destocking Exceeds 1,000 Tons

As of December 4th, total stainless steel inventory in Wuxi sample warehouses increased by 393 tons to 560,186 tons.

Breakdown:

Stainless steel 200 Series: 710 tons up to 54,897 tons.

Stainless steel 300 Series: 1,482 tons down to 390,898 tons.

Stainless steel 400 Series: 1,165 tons up to 114,391 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Nov 27th | 54,187 | 392,380 | 113,226 | 559,793 |

| Dec 4th | 54,897 | 390,898 | 114,391 | 560,186 |

| Difference | 710 | -1,482 | 1,165 | 393 |

According to statistics, the total stainless steel inventory in Wuxi sample warehouses increased slightly this period compared to the last. Specifically, the stainless steel 200 and stainless steel 400 series saw inventory accumulation, while the stainless steel 300 series saw a decrease. After rebounding early in the week, the stainless steel futures market continued to strengthen, and market transaction conditions improved; however, stainless steel mill arrivals increased, leading to mixed inventory changes.

Stainless steel 300 Series: Halting Decline and Rebounding, Continuous Inventory Depletion

1.Recently, Tsingshan resources have arrived, leading to a slight accumulation of inventory in forward warehouses in Jiangyin and Jingjiang last week.

2.Early in the week, stainless steel prices stopped falling and rebounded, market transactions warmed up, and inventory depletion among market traders and agents was significant.

3.As the stainless steel industry is in the off-season, superimposed with the beginning of the month, agents picked up fewer goods. Stainless steel mill production cuts are beginning to show initial results, and inventory has started to slowly deplete.

Follow-up attention should be paid to the recovery of downstream demand.

Stainless steel 200 Series: Cold-Rolled Arrivals Increase, Inventory Accumulates as Transactions Weaken

1.Hongwang cold-rolled resources increased last week.

2.Early in the week, the futures market stopped falling and rebounded. As prices stabilized, downstream buyers mostly shifted to a wait-and-see status. Shipments of high-priced resources were hindered, leading to a slight accumulation of cold-rolled inventory.

3.During the week, hot-rolled stainless steel 201 prices were lowered by 50, increasing low-price transactions, causing hot-rolled inventory to shift from an increase to a decrease.

Stainless steel 400 Series: Weak Downstream Demand, Slight Inventory Accumulation

1.There were many arrivals of JISCO resources last week, increasing tradable resources in the market.

2.Last week, 430 prices remained stable, and trader quotes were firm. Downstream buyers mostly purchased flexibly based on rigid demand. The pace of trader shipments was flat, overall transaction volume struggled to break through, and spot market inventory accumulated slightly.

On the steel mill side, to cope with the current situation of slow inventory digestion, mills are actively cutting production. The crude steel production schedule for December has shrunk significantly. According to ZLJ (Zhonglianjin) statistics, in December, the planned crude steel production volume for 33 domestic mainstream stainless steel mills is 3.115 million tons, a month-on-month (MoM) decrease of 7.75% and a year-on-year (YoY) decrease of 9%.

Stainless steel 200 Series: 899,000 tons, a decrease of 108,000 tons MoM (-10.72%) and a decrease of 87,500 tons YoY (-8.87%).

Stainless steel 300 Series: 1.703 million tons, a decrease of 51,000 tons MoM (-2.93%) and a decrease of 158,000 tons YoY (-8.5%).

Stainless steel 400 Series: 513,000 tons, a decrease of 102,000 tons MoM (-16.6%) and a decrease of 62,000 tons YoY (-10.8%).

RAW MATERIAL | November High Ferrochrome Total Output Increases to 877,800 Tons, a 5.49% Increase

General Raw Materials

Regarding raw materials, CME data indicates that the probability of a 25 basis point interest rate cut by the Federal Reserve in December has risen to 87%. Boosted by macro sentiment, the non-ferrous metals sector continued to rise during the week. Superimposed with the impact of tight supply, copper prices broke through the US$12838 mark. Currently, the average price of Changjiang non-ferrous copper has been raised by US$584.8 month-on-month to US$13044/MT; manganese prices were raised by US$21/MT to US$2025.67; and high-carbon ferrochrome remained flat at US$1127/50 reference ton.

High Nickel Pig Iron (NPI)

Transaction prices for High NPI rose slightly to US$128.39/nickel point. The current production cost for Indonesian NPI is US$123.8/nickel point. Recent fluctuating increases in nickel futures have boosted market sentiment, and transaction prices are showing an upward trend. According to market news, recently a factory in East China sold domestic iron at a transaction price of US$132.66/nickel point (ex-works, tax included) for a total of 6,000 tons, with a grade of 8%-12% and delivery in December '25. Indonesian iron was sold at US$129.1/nickel point(port, tax included) for a total of 3,000 tons, with a grade of 10%-13% and delivery in December '25.

High-Carbon Ferrochrome

High-carbon ferrochrome prices maintained US$1134/50 reference tons. On the raw material side, chrome ore prices were lowered. A large South African chrome ore supplier quoted a new round of 40-42% chrome concentrate futures at $263/ton CIF, down $7/ton CIF from the previous round. The current production cost of high-carbon ferrochrome has dropped to US$1091.3/50 reference tons. Currently, downstream stainless steel mills have rigid procurement demand for domestic ferrochrome; inquiries and purchasing last week were more substantial than last week. However, ferrochrome output in December is expected to remain high, and with the downstream stainless steel market being weak, the pattern of oversupply remains. Subsequent procurement demand may decrease. Overall, the high-carbon ferrochrome market is expected to maintain a pattern of narrow fluctuations in the short term.

Ferromolybdenum (FeMo)

Last week, the molybdenum market maintained a weak but stable situation. End-user steel mills conducted procurement successively, with tender openings at US$32525 to US$32667/ton for cash and US$33024 to US$32596/ton for acceptance.

There is significant resistance to transactions for high-priced sources. Demand for FeMo in terminal fields like stainless steel is currently sluggish; steel mill purchasing strategies are conservative, and suppressing prices has become a common phenomenon. The supply side presents a loose trend; molybdenum concentrate is currently in a state of oversupply. Superimposed with an increase in domestic procurement of imported molybdenum oxide, this further exacerbates the loose situation on the raw material side, directly inhibiting the upward momentum of molybdenum concentrate prices and keeping them consolidating at low levels. The pressure of price suppression from downstream steel mills is transmitted upward to the Ferromolybdenum link, causing Ferromolybdenum prices to lack upward momentum. However, despite the loose supply, cost support from leading mining companies and production cuts by some small and medium-sized mines due to environmental factors jointly limit the downward space for raw material prices, keeping the overall molybdenum market running in a relatively stable low range last week.

SUMMARY | Supply-Demand Imbalance Intensifies, Prices Grind at Low Levels

Social inventory destocking is slow. On the stainless steel demand side, consumption momentum is insufficient and difficult to absorb supply pressure, leading to shrinking production profits for steel mills. Market confidence is weak, and prices may continue to grind at the bottom. The future outlook requires attention to follow-up policy support at the macro level, as well as changes in steel mill production schedules and raw material prices.

Entering December, the year-end off-season effect is appearing, and terminal domestic demand will likely fade further. However, exports and policy aspects may bring small variables to partially offset the impact of weak domestic demand. For example, the extension of the India BIS certification exemption (finalized on November 20), superimposed with a low export base in the previous period—China's stainless steel exports to India from January to October 2025 were 147,400 tons (a sharp year-on-year decrease of 64.4%)—suggests subsequent export volumes are expected to continue recovering. Additionally, rising expectations for a Fed rate cut and the gradual exertion of domestic steady growth policies, while capable of boosting market sentiment in stages, have a time lag in transmitting to real demand, so the actual pulling effect on December demand is limited.

300 Series: Overall, the short-term market may continue a weak and stable fluctuating trend. The cost side has no significant fluctuations for now, forming bottom support for prices. However, demand is still in the off-season, and downstream procurement is unlikely to see large-scale volume increases. Superimposed with the pressure of inventory accumulation in steel mill forward warehouses, spot prices lack upward drivers. If the futures market continues to fluctuate, spot prices may maintain their current range. Follow-up focus should be on the implementation of macro-favorable policies on the demand side and marginal changes in steel mill shipping strategies.

200 Series: During the week, raw material copper broke through the 90,000 mark, manganese prices were cumulatively raised by US$29/MT, and ferrochrome remained flat, further strengthening cost support for stainless steel 201. Steel mills maintained production cuts in December, leaving fewer circulating resources for the future. Currently, the market is paying close attention to futures and steel mill production trends. Downstream buyers are purchasing opportunistically, and with difficult-to-breakthrough off-season demand, it is expected that stainless steel 201 prices will remain mainly stable in the short term.

400 Series: Overall, retail prices for high chrome stopped falling and stabilized during the week. However, TISCO's steel tender price for high chrome in December fell by US$14/50 reference tons month-on-month. Cost support for stainless steel 400 series stainless steel is weak, market wait-and-see sentiment is strong, and transaction activity is average. Although the December steel mill production cut plans continue to alleviate market supply pressure, overall downstream demand in the off-season is difficult to boost significantly, and inventory depletion momentum is insufficient. Future focus will remain on inventory changes and market transaction conditions.

MACRO | China Steel 2025 Review: Export Support

Steel Exports Maintain High Levels

From January to October 2025, cumulative steel exports grew by 6.6% year-on-year (YoY), and steel billet exports grew by 157%. Export volumes hit a record high.

From January to October 2025, cumulative steel exports reached 97.74 million tons, a cumulative increase of 6.6% compared to the same period last year.

From January to October 2025, cumulative steel billet exports reached 11.90 million tons, a cumulative YoY increase of 156.94%. Overall exports exceeded expectations, and overseas competitiveness remains high.

From January to October 2025, cumulative rebar exports reached 3.21 million tons, a cumulative YoY increase of 49.42%.

Exports by Country

From January to October 2025, the top ten destinations for steel exports were Vietnam, South Korea, Thailand, the Philippines, the UAE, Saudi Arabia, Indonesia, Turkey, Brazil, and Malaysia, mainly concentrated in Southeast Asia and the Middle East.

Among them, Saudi Arabia saw a cumulative YoY increase of 19%, marking the largest growth among the top ten, followed by Thailand and the Philippines. Vietnam saw the highest YoY decline, but in absolute terms, it remains China's largest steel export trading partner. The combined export volume to the top ten countries decreased slightly by 4.22% YoY.

Outlook for 2026: Both the supply and demand sides of steel are unlikely to see significant changes.

Demand Side: China's real estate and infrastructure sectors are expected to remain in negative growth, while manufacturing demand will continue to maintain positive growth.

Export Side: Close attention must be paid to the impact of overseas policies on direct and indirect exports.

Risk Factors:

1.Changes in crude steel production reduction policies.

2.Changes in carbon emission progress.

3.The impact of macro policies on stimulating demand.

December 3, 2025 update: On November 26, 2025, Prime Minister Mark Carney announced that, effective December 26, 2025, the government will, for imports of:

steel mill products from countries that:

do not have a free trade agreement (FTA) with Canada, reduce the tariff rate quota (TRQ) levels from 50% to 20% of 2024 levels

have an FTA with Canada (except the United States and Mexico), reduce the TRQ levels from 100% to 75% of 2024 levels

TRQs1 will apply on imports into Canada of steel mill products in these five steel product categories:

pipe and tube

semi-finished

stainless steel

Imports into Canada that exceed specified quantity thresholds will be subject to a 50% surtax (which is in addition to any existing duties).

The quota for tariff‑free imports into Canada will depend on whether the country has an FTA with Canada. The TRQ will be based on, for:

non-FTA countries:

2024 volume levels (2.6 million tonnes), starting June 27, 20252

50% of 2024 volume levels, starting August 1, 2025

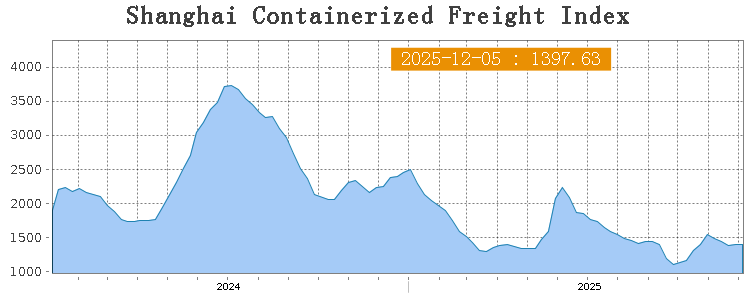

SEA FREIGHT | Freight Rates Continued a Downward Trend

On December 5th, the Shanghai Containerized Freight Index (SCFI) fell 0.4% at 1397.63 points.

Europe/ Mediterranean:

On December 5th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1400/TEU, which decreased by 0.3%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$2300/TEU, which was up by 3% from previous week.

North America:

Last week, transport demand continued to lack upward momentum, and freight rates in most trade lanes adjusted downward.

On December 5th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$1550/FEU and US$2315/FEU, reporting 5% and 4.7% loss accordingly.

The Persian Gulf and the Red Sea:

On December 5th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf gained 4.9% to US$1781/TEU.

Australia & New Zealand:

On December 5th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand decreased by 2.9% to US$1276/TEU.

South America:

On December 5th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports fell by 7.8% to US$1689/TEU.