Tsingshan Leads the Decline, Raw Materials Loosen, Stainless Steel Falls Below US$2,360/MT

Last week, stainless steel prices in the Wuxi market continued to decline. Previously, there was a strong bullish sentiment in the market, expecting prices to reach US$2510/MT; however, after surging post-holiday, prices fell sharply, even dropping below the US$2360/MT mark. The price-supporting sentiment among steel mills and traders vanished entirely, leading to a continuous downward trend. As of this Friday, the main stainless steel contract price fell by US$37/MT from last week to US$2345/MT, a decrease of 1.65%.

Stainless steel 300 Series: Cold-Rolled 304 Price Reduced by US$22/MT

Last week, cold-rolled and hot-rolled 304 spot prices showed a weak downward trend. As of Friday, the mainstream base price for 4-foot cold-rolled stainless steel 304 in the Wuxi area was quoted at US$2345/MT, down US$22/MT from last week's price; the hot-rolled stainless steel price was quoted at US$2330/MT, down US$7/MT from last week. During the week, spot prices did not closely follow the significant fluctuations of futures prices. Because steel mills opened with high prices and spot merchants had high holding costs, it was difficult for overall prices to drop deeply. It wasn't until Thursday, when Tsingshan stainless steel 304 opened with a US$30/MT drop, that market quotations became chaotic, with most merchants dropping another US$ to take orders. The price gap between cold and hot rolled /MT further narrowed, and the previous price-supporting mentality visibly loosened.

Boosted by the recent surge in ferromolybdenum, pushing up the cost support for stainless steel 316L, the price of the stainless steel 316L variety rose sharply by US$267.8/MT last week. Calculated based on the recent transaction prices of molybdenum concentrate, the cost of ferromolybdenum has risen to US$50595/MT, which obviously pulls up the cost for molybdenum-containing steel varieties. After Tsingshan Steel opened on Monday with a substantial price increase of US$104/MT, it continued to raise its price limit policy on Tuesday by another US$148/MT. The total price increase was around US$253/MT.

Spot market quotations collectively surged in tandem. Tsingshan-affiliated agents were simultaneously controlled by the price limit policy, with the Yongjin cold-rolled stainless steel 316L price limited to a minimum of US$4725/MT gross base, and the hot-rolled stainless steel 316L coil price limited to a minimum of US$4630/MT.

The mainstream quotation for TISCO and ZPSS cold-rolled stainless steel 316L reached US$4805/MT, an increase of US$178.5/MT; the mainstream quotation in the spot market for Dongte, ZPSS, and other hot-rolled stainless steel 316L was US$4610/MT, an increase of US$148/MT. TISCO's hot-rolled coil price was quoted at US$4685/MT, an increase of US$223/MT.

Stainless steel 200 Series: Stable Quotations, Yielding Profits to Promote Transactions

Last week, the futures market trended weakly, and spot quotations were adjusted downwards accordingly. Currently, prices from Desheng and Beigang are quoted at a 7650 base, while Tsingshan cold-rolled stainless steel 201J2 is quoted at a US$1265/MT. Market agent quotations remain high, traders flexibly adjust according to the futures board, and some actual transactions may have minor profit concessions. Downstream buyers mostly opted for low-priced resources for rigid demand procurement, and as transactions synchronously weakened, cold-rolled inventory accumulated slightly.

Stainless steel 400 Series: High Chromium Costs Retreat, Market Sentiment is Cautious

Last week, Stainless steel 430 prices operated stably. As of Saturday, the spot market quotation for state-owned cold-rolled stainless steel 430 in Wuxi was US$1270/MT, and the hot-rolled stainless steel quotation was US$1135/MT, both flat compared to pre-holiday quotations. The continuous post-holiday rise in futures prices drove an improvement in market sentiment, traders' willingness to be bullish heated up, and some traders slightly raised their quotations. However, in the latter half of the week, high chromium prices fell again, cost support on the raw material side somewhat loosened, and market sentiment returned to caution. Additionally, the post-holiday market mainly focused on delivering pre-holiday orders; the overall shipping pace was flat, inventory digestion fell short of expectations, and there was a noticeable phased accumulation of inventory.

Raw Material: Nickel and Molybdenum Products Expected to Maintain High Prices in the Short Term

High-Grade Ferronickel

The overall high-grade ferronickel market slightly loosened and trended weakly. Influenced by the suspension of Indonesia's implementation of some additional tax and fee policies, the market's concerns regarding the policy side somewhat eased. Coupled with a continuously sluggish spot trading atmosphere, traders' quotations followed the downward trend, and high-grade ferronickel prices showed a slight, weak pullback. On May 14, high-grade ferronickel spot transactions from Indonesian ferronickel plants landed at a transaction price of US$172/nickel point (ex-ship hold, including tax), with a nickel grade of 11 and a transaction volume of 12,000 tons. The goods were received by traders, and the center of gravity for transactions moved lower compared to the previous period. Currently, the procurement mentality of mainstream steel mills is cautious, with target prices dropping to around US$169.6/nickel point, and the bargaining room between upstream and downstream has clearly widened; the production cost line for Indonesian ferronickel has risen to US$165.7/nickel point, forming a bottom support for prices.

Indonesia's Ministry of Energy and Mineral Resources (ESDM) has officially released the Benchmark Mineral Price (HMA) for nickel for the second half of May 2026. The HMA for the second half of May is: the nickel price is 18,849.3 USD/ton (compared to 17,802.14 USD/ton in the first half of May 2026), an increase of 1047.15 USD, or 5.88%.

Ferromolybdenum

Ferromolybdenum prices skyrocketed, with market quotations soaring to US$49404/MT, representing a weekly surge of about US$3422/MT.

| Total Inventory across 89 Major Stainless Steel Physical Warehouses | |||||||||

| Series | Total | Cold Rolled Coil | Hot Rolled Coil | ||||||

| Volume (Tons) | Weekly differences | Change% | Volume (Tons) | Weekly differences | Change% | Volume (Tons) | Weekly differences | Change% | |

| 300 Series | 689,033 | -2979 | -0.43% | 445,145 | 5118 | 1.16% | 243,888 | -8097 | -3.21% |

| 200 Series | 172,782 | -6689 | -3.73% | 113,570 | -2415 | -2.08% | 59,212 | -4274 | -6.73% |

| 400 Series | 273,012 | -759 | -0.28% | 110,350 | -8335 | -7.02% | 162,662 | 7576 | 4.89% |

This round of strong upward momentum in ferromolybdenum was driven by the resonance of multiple favorable factors: international molybdenum prices continued to rise, the tight supply pattern of domestic spot molybdenum concentrate persisted, ferromolybdenum remained in a long-term cost inversion state, and downstream steel mills maintained their rigid demand restocking pace. At the same time, Peru officially issued an energy crisis emergency decree, causing local mines to face power rationing and production cuts; as a core global supplier of molybdenum raw materials, expectations of a supply contraction from Peru continued to heat up, further strengthening the market's bullish sentiment. The combination of multiple factors fueled a substantial spike in ferromolybdenum prices, forming strong cost support for molybdenum-containing stainless steel varieties like 316L and duplex steel, leading to a synchronous collective price increase across all molybdenum-related products in the industry chain.

According to market news, the bidding transaction price for ferromolybdenum at a steel mill in East China was US$49851/60 reference ton, a month-on-month increase of US$4464/60 reference ton. In the stainless steel spot market, varieties like 316L and 2205 surged by US$238/MT in a single week. After international molybdenum prices continuously rallied to high levels, prices have pulled back somewhat in the last two days. Currently, international molybdenum oxide is at 30-30.6 USD/lb Mo, and the market's pace of holding up prices has somewhat slowed.

In the short term, the overall cost of molybdenum-based raw materials has risen, and the tight supply pattern of molybdenum concentrate has not yet eased. Mining companies have a strong sentiment of withholding sales to support prices, which provides a strong bottom support for ferromolybdenum prices from the cost side. Ferromolybdenum production is dually constrained by the domestic shortage of molybdenum concentrate and overseas import supply disruptions; even with a phased decline in sentiment, the room for a deep correction is relatively limited. The market's willingness to sell off goods at low prices is weak, and it is highly likely to maintain a high and strongly volatile pattern going forward.

SUMMARY: Raw Material Costs Will Continue to Support Stainless Steel Prices

Last week, stainless steel prices in the Wuxi market continued their weak trend. Because the previous news regarding Indonesian nickel did not materialize substantially, sentiment-driven support declined.

Stainless steel 304: Prices fell under pressure, with a cumulative drop of US$30.

Stainless steel 316L: The surge in ferromolybdenum drove a significant rise in 316L prices, increasing by US$267.

Stainless steel 201: Prices maintained a narrow range of fluctuation, rising or falling by US$7.

Stainless steel 400 Series: Overall, it maintained a relatively stable operation.

In the short term, the support from the raw material side is marginally weakening; the transaction price of high-grade ferronickel has moved lower, and the transaction volume is relatively small. Coupled with easing concerns over related tax increases in Indonesia, chromium ore prices have loosened, collectively weakening the cost support for stainless steel. However, it should be noted that the overall tight pattern on the mining side has not changed, which still provides a certain bottom support for raw material prices; it is expected that the downside room for raw material prices is limited, thereby providing bottom support for stainless steel prices.

On the spot level, steel mills continue their strategy of controlling shipping volumes, and the overall tight pattern for hot-rolled stainless steel spot resources remains unchanged. Its resistance to price drops is relatively strong, further supporting stainless steel prices. Comprehensively judging, short-term stainless steel prices will continue their volatile and weak operational trend, but supported by bottoming raw materials and tight hot-rolled supply, the room for deep declines is limited.

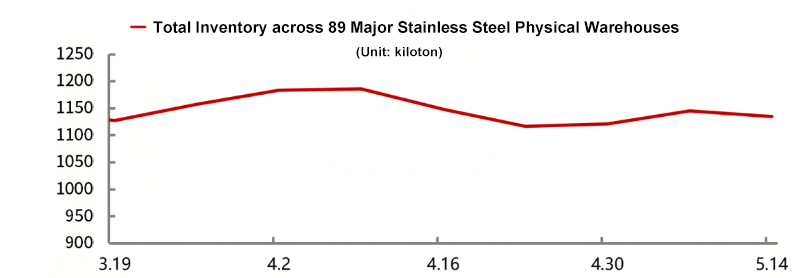

INVENTORY: National Inventory Shifts from Increase to Decrease

On May 14, 2026, the total social inventory across 89 warehouses in mainstream national markets was 1.1348 million tons, a week-on-week decrease of 0.91%, ending the accumulation trend from the previous week. Among this, the total inventory of cold-rolled stainless steel was 669,100 tons, a week-on-week decrease of 0.83%; the total inventory of hot-rolled stainless steel was 465,800 tons, a week-on-week decrease of 1.02%. Both cold and hot-rolled shifted from an increase to a decrease, with basically the same destocking magnitude.

Looking at the different series, the 200 series inventory continued to decline, while the 300 series and 400 series shifted from an increase to a decrease.

Overall, the national inventory shifted from an increase to a decrease last week, mainly benefiting from the settlement and digestion of 300 series and 400 series resources in the Wuxi market. However, some series in Foshan and other regional markets still face accumulation pressure.

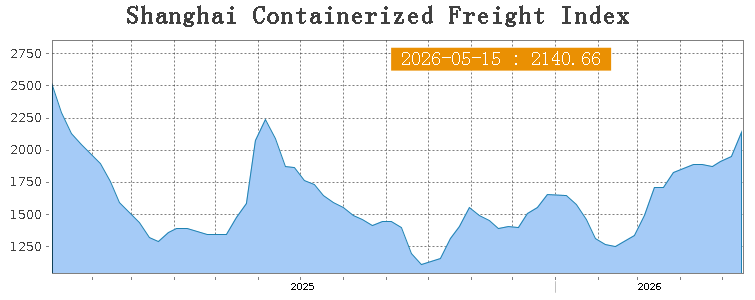

SEA FREIGHT: Freight rates on the Shanghai–South America route surged 28.9% within the week

China's export container shipping market remained generally stable, with freight rates on ocean-going routes showing an upward trend and the composite index continuing to rise. On May 15th, the Shanghai Containerized Freight Index (SCFI) rose 9.5% at 2140.66 points.

Europe/ Mediterranean:

On May 15th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1816/TEU, which increased by 13.8%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$3145/TEU, which was a surge by 27.7% from the previous week.

North America:

On May 15th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$3118/FEU and US$4224/FEU, reporting a 10.3% and 10.8% gain, respectively.

The Persian Gulf and the Red Sea:

On May 15th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf increased 5.2% to US$4131/TEU.

Australia & New Zealand:

On May 15th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand increased by 9.2% to US$1317/TEU.

South America:

On May 15th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports surged by 28.9% to US$4256/TEU.