London Metal Exchange (LME) nickel prices fluctuated and closed higher last week. Opening at $16,385/ton, reaching a high of $16,670/ton and a low of $16,205/ton, it closed at $16,585/ton, a week-on-week increase of 1.38%. Stainless steel prices fluctuated sharply last week, with generally spot transactions at lower prices. The main futures contract touched a low near US$2250/MT. As of Friday's night session close, the main stainless steel futures contract was reported at US$2310/MT.

Overall, nickel prices fluctuated within a range last week under the influence of inventory and macroeconomic sentiment, recovering from low levels late in the week. On the supply side, ore prices fell, nickel price weakened, and capacity continues to expand. July is the last phase of applying for RKAB, which will determine the quotation and supply of nickel ore the market will gain in the rest of 2026. In the short term, the Fed’s moves and the RKAB changes will be the two largest factors for the nickel dynamics. Generally, it is predicted that nickel price lacks increasing momentum.

Stainless Steel Spot Market: Tsingshan Opens Downward Across Cold and Hot Rolled, High Inventory Pressure Highlights Again

Stainless steel 304

Last week, spot prices for both cold-rolled and hot-rolled stainless steel 304 weakened. As of Friday, the mainstream base price for 4-foot private cold-rolled stainless steel 304 in Wuxi was reported at US$2275/MT, down US$7 from last week; hot-rolled reported at US$2240/MT, down US$22 from last week. Regarding steel mills, Tsingshan quoted cold and hot-rolled stainless steel 304 on Thursday, lowering by US$45 from previous prices; in the afternoon, prices were raised by US$14/MT, totally dropping by US$30/MT in a day. Due to rapid fluctuations, people were more cautious, resulting in weak transactions.

Overall, demand is expected to remain subdued during the seasonal slowdown, leaving limited upside for stainless steel prices. Cold-rolled prices are expected to trade in the range of US$2,260–2,305/MT, while hot-rolled prices are likely to fluctuate between US$2,245 and US$2,275/MT. Should planned maintenance at steel mills proceed as scheduled, easing inventory pressure and accelerating the drawdown of accumulated stocks, spot market activity could improve, potentially paving the way for a recovery in stainless steel prices.

Stainless steel 201

Stainless steel 201 prices showed mixed movements last week. As of Friday (July 10th), Hongwang quoted cold-rolled stainless steel 201 J2 at US$1,285/MT, with transaction prices typically negotiated around US$22/MT lower. Beigang New Materials quoted US$1,260/MT for cold-rolled material, while hot-rolled stainless steel J1 was offered at around US$1,365/MT.

Early in the week, discounted offers with concessions of approximately US$7/MT dominated trading. However, adverse weather disrupted steel mill deliveries, prompting dealers to raise their offers by around US$7/MT on Wednesday. Toward the end of the week, Tsingshan’s dealers reduced the offer by US$22/MT for prompt shipments. Meanwhile, reduced arrivals led to a slight decline in inventories.

Production costs for stainless steel 201 continued to ease. On the supply side, most steel mills that had undergone maintenance earlier resumed normal production during the month. July production of 200-series stainless steel is expected to recover, further elevated inventory levels.

In the absence of stronger downstream demand, weak market conditions are expected to persist. Cold-rolled stainless steel 201 J2/J5 prices (gross basis) are therefore expected to remain under pressure, fluctuating within a range of US$1,225–1,300/MT.

Stainless Steel 430

Stainless steel 430 prices remained stably weak. As of Friday, cold-rolled 430 stainless steel was quoted at US$1,275/MT in the Wuxi market, while hot-rolled 430 was quoted at US$1,140/MT, both unchanged from the previous week.

Futures prices fluctuated throughout the week, buyers waited. To stimulate sales, most traders offered discounts. Overall trading activity remained subdued.

Meanwhile, continuous arrivals of steel mill shipments outpaced downstream demand, resulting in further inventory accumulation for both cold-rolled and hot-rolled products.

Summary & Outlook

Overall, although stainless steel output declined slightly in June, production cuts was limited, leaving overall supply at high levels. With steel mill profitability improving, production is expected to increase again in July. However, output of the 300 series is projected to decline as steel mills continue reallocating capacity to the 200 and 400 series, further increasing supply pressure and inventory levels for both product categories.

In the near term, Tsingshan's pricing strategy should continue to provide some support to the market. Nevertheless, end-user demand remains subdued, and the broader oversupply situation is unlikely to change. As a result, any downside in prices may moderate, but a meaningful recovery is unlikely in the absence of stronger demand.

Seasonally weak demand, compounded by adverse weather conditions, continues to weigh on downstream purchasing activity. Meanwhile, social inventories of 400-series stainless steel have increased for a third consecutive week, reinforcing the imbalance between supply and demand. In the short term, prices are expected to remain under pressure, with market participants closely watching steel mill production plans and spot trading activity for clearer market direction.

Nickel: Uncertainty Remains Over Indonesian Nickel Ore Quota Outlook

Although the market generally expects Indonesia to raise its final 2026 RKAB nickel ore quota, significant uncertainty remains regarding the specific arrangements.

Indonesia's Ministry of Energy and Mineral Resources (ESDM) stated that adjustments to the 2026 nickel ore RKAB quota are not expected to be substantial, with newly approved quotas prioritized for smelters facing raw material shortages. The market generally considers this part of the Indonesian government's measures to control nickel supply, support nickel prices, and reduce market surplus. However, the potential incremental scale has not been announced, and other details remain unconfirmed.

The market still lacks clear guidance regarding the final quota level, though most market participants expect an upward adjustment. Some participants expect an increase of about 10%, which would raise the 2026 RKAB quota to roughly 290–300 million wet metric tons (wmt). Previously, Indonesia had approved a 2026 nickel ore RKAB quota of about 260–270 million tons, significantly lower than 2025's 379 million tons.

Other participants argue that given weakening nickel ore prices, any quota increase will be limited. Lower benchmark prices could dampen the motivation for significant quota expansions while reinforcing the government's cautious approach to supply management.

In the first half of July, Indonesia's Mineral Benchmark Price (HMA) for nickel fell to $17,593/ton, down from $18,642/ton in the second half of June. This is expected to lower the benchmark price (HPM) for 1.5% grade nickel ore by at least $3/wmt.

Currently, the Indonesian government is still assessing domestic ore demand, and the window for mining companies to submit RKAB revision applications will remain open until the end of July.

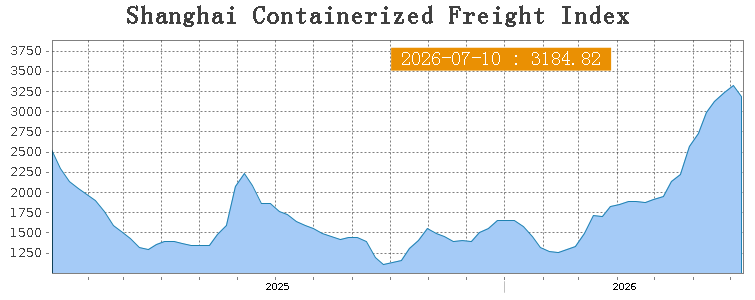

Sea Freight: Freight Rates Adjusted Downward, Strait of Hormuz Blocked Again

Last week, demand in China's export container shipping market was generally stable, with ocean route freight rates pulling back and the composite index dropping slightly. On July 10, the Shanghai Containerized Freight Index published by the Shanghai Shipping Exchange (under preparation) stood at 3,184.82 points, down 4.3% from the previous period.

·European Route: Shipping demand was relatively stable last week, and spot booking prices pulled back slightly after continuous gains. On July 10, the market freight rate (ocean freight and surcharges) from Shanghai Port to European base ports was $3,332/TEU, down 2.5% from the previous period.

·Mediterranean Route: The market trend mirrored the European route, with freight rates pulling back slightly. On July 10, the rate from Shanghai Port to Mediterranean base ports was $4,561/TEU, down 3.3% from the previous period.

·North American Route: Shipping demand was generally stable and the supply-demand balance was maintained; spot rates underwent an adjustment following earlier substantial gains. On July 10, rates from Shanghai Port to US West Coast and US East Coast base ports were $6,219/FEU and $8,134/FEU, down 6.2% and 2.0% respectively.

·Persian Gulf Route: Small-scale conflicts broke out between the US and Iran last week, leading to renewed Middle East geopolitical tensions that dragged down the recovery of Strait of Hormuz shipping; market freight rates continued to fall. On July 10, the rate from Shanghai Port to Persian Gulf base ports was $4,199/TEU, down 4.4% from the previous period.

·Australia-New Zealand Route: Growth in shipping demand lacked momentum, supply-demand fundamentals weakened, and freight rates pulled back slightly. On July 10, the rate from Shanghai Port to Australia-New Zealand base ports was $2,266/TEU, down 0.6% from the previous period.

·South American Route: Shipping demand lacked further growth momentum, and spot rates extended their adjustment trend. On July 10, the rate from Shanghai Port to South American base ports was $6,570/TEU, down 9.1% from the previous period.

Just 25 days after the signing of the US-Iran Memorandum of Understanding, the Strait of Hormuz was closed once again on July 12.

Analysts pointed out: "The Strait of Hormuz is Iran's core strategic leverage as well as its most important deterrent tool and bargaining chip; it will neither recover smoothly nor return to the past. Whenever any situation change or execution occurs that dissatisfies Tehran, closing or tightening control over the strait becomes a pressure tactic at the negotiating table. It does not need to secure $300 billion or more in benefits at once; instead, by leveraging global reliance on energy transport and supply chain security, it can continuously create leverage, gain advantages, and enhance its bargaining power across repeated crises and negotiations. In this sense, it is difficult for the Strait of Hormuz to ever return to its past state."

Although shipping costs have finally cooled down after ten consecutive weeks of increases, it does not mean the crisis has passed.

During the 108 days of conflict, global energy markets demonstrated resilience that exceeded expectations. After the war ended, international oil prices even swiftly dropped back to pre-war levels. However, the market environment has now changed. Previously, the market could withstand the conflict largely because global oil inventories were ample, alternative supplies were available, the conflict duration was limited, and shipowners and energy companies possessed significant risk buffers. Today, global inventory buffers are declining, and energy markets no longer possess the ample 'safety cushion' they had months ago. If Hormuz risks persist or enter another high-intensity conflict phase, the impact could very likely exceed that of the previous round.