Weekly Review: Off-Peak Purchasing Season, Stainless Steel Transactions Weaken (Jun 15-18)

Stainless steel futures prices fluctuated within a wide range this week. From June 15 to 17, stainless steel futures prices fell first before rising, accompanied by a release of heavy trading volumes, but open interest decreased significantly on Friday. Amid the currently fast-changing news environment, the long-short tug-of-war has intensified, and uncertainty regarding the future market remains high, causing the market overall to trend toward caution.

Prices still perform weakly, the downward trend has not stopped, and future market volatility will remain at a relatively high level. The main contract for stainless steel futures closed at US$2320/MT this week, with a weekly price increase of 0.51% and a weekly low of US$2260/MT.

June 19 was the Dragon Boat Festival holiday. In the week prior to the holiday, the stainless steel market showed a pattern of falling first and then rising, dominated by macroeconomic sentiment. Boosted by signals of easing US-Iran relations, the main stainless steel futures contract experienced a phased rebound, but the spot market showed limited willingness to follow the increase. For example, the spot basis price of private cold-rolled stainless steel coils 304/2B in the Wuxi market was around US$2345/MT, pulling back from the high point of US$2425/MT seen in early May. Taking a longer view, the cold-rolled stainless steel 304 series has achieved a cumulative increase of over 15% from the beginning of 2026 to date, starting from a basis price of only US$2045/MT at the beginning of the year; after surging to the year's high in early May, the price center of gravity gradually shifted downward, correcting back to over US$2365/MT by the pre-holiday period.

On Monday, June 22, the first working day after the Dragon Boat Festival, overall fluctuations in stainless steel spot prices were limited, and both stainless steel and Shanghai nickel futures showed range-bound performance, exerting a weak driving force on spot prices.

Steel mills currently express a clear intent to support prices, keeping cost support solid. Tsingshan Group continued to issue flat June futures plate prices with an allocation cycle of about three days, and the execution progress of June orders is nearing its end. Liyang Steel Mill raised its hot-rolled stainless steel 304 quotation by US$7 to US$2290/MT while steel mills such as Liyang and Xiangshui simultaneously raised the pre-settlement price of cold-rolled stainless steel 304 by US$14/MT, adjusting it to US$2380/MT.

How Macro Risk Reduction, Stainless Steel Output Cuts, and the Off-Peak Purchasing Season Will Affect the Global Market

China's Stainless Steel Mills Cut Production by 200,000 Tons in June

From the supply side, domestic crude stainless steel production scheduling plans showed a clear contraction in June. According to Mysteel statistics, estimated crude steel production scheduling for June is 3.6043 million tons, a month-on-month decrease of 5.56% and a year-on-year increase of 9.5%, among which:

Stainless steel 200 Series: 937,800 tons, down 13.21% month-on-month and down 5.21% year-on-year.

Stainless steel 300 Series: 2.0037 million tons, down 2.62% month-on-month and up 14.89% year-on-year.

Stainless steel 400 Series: 662,800 tons, down 2.27% month-on-month and up 18.72% year-on-year.

Based on these calculations, the monthly reduction exceeds 200,000 tons, constituting the core industrial bullish factor in the current market. However, this expectation of production cuts failed to effectively boost prices, primarily because the year-on-year growth on the supply side remains relatively large, causing market sensitivity to "production cut" signals to drop significantly. After the announcement of production cuts, open interest on the stainless steel board increased instead, but finished steel prices failed to move higher accordingly.

1. Global Non-Ferrous Metal Asset Valuations Are Generally Under Pressure:

US non-farm payroll data for May significantly exceeded expectations, and sticky inflation pushed the timing of Federal Reserve interest rate cuts further back. The 10-year US Treasury yield rose to 4.55%, and the US Dollar Index stood firm above the 100 mark, putting general pressure on global non-ferrous metal asset valuations. Against this backdrop, risk appetite for industrial products cooled down significantly, directly suppressing the upside potential for valuation repairs in Shanghai nickel and stainless steel futures.

2. The Chinese Construction Industry Enters Its Off-Season, and Domestic Stainless Steel Faces Export Barriers:

Data on the demand side is not optimistic: after running at relatively high levels from January to March 2026, apparent consumption retraced to around 3.3955 million tons in April, and the latest published production scheduling and inventory data both point to weakening demand during the off-season. Although export volumes have seen some repair, domestic stainless steel still faces exceptionally high barriers regarding exports.

3. Lowering Stainless Steel Production Remains Difficult to Offset Existing High Inventories:

Looking at Chinese domestic demand, May CPI rose mildly by 1.2%, while PPI increased by 3.9% year-on-year, hitting a 46-month high (since August 2022), with inflationary pressures limiting the scope for policy easing. However, the multi-trillion investment under the "15th Five-Year" Urban Renewal Plan continues to move forward, keeping the steady growth undertone unchanged. It is worth noting that the newly promulgated steel capacity replacement rules by the Ministry of Industry and Information Technology included stainless steel under a unified assessment for the first time, raising the nationwide replacement ratio to no less than 1.5:1. This will accelerate the elimination of backward capacity, alleviate low-price internal competition, and benefit the industry's supply structure over the medium-to-long term. The landing pace and scale of domestic steady-growth policies, especially the multi-trillion urban renewal investments, will determine the recovery elasticity of domestic demand.

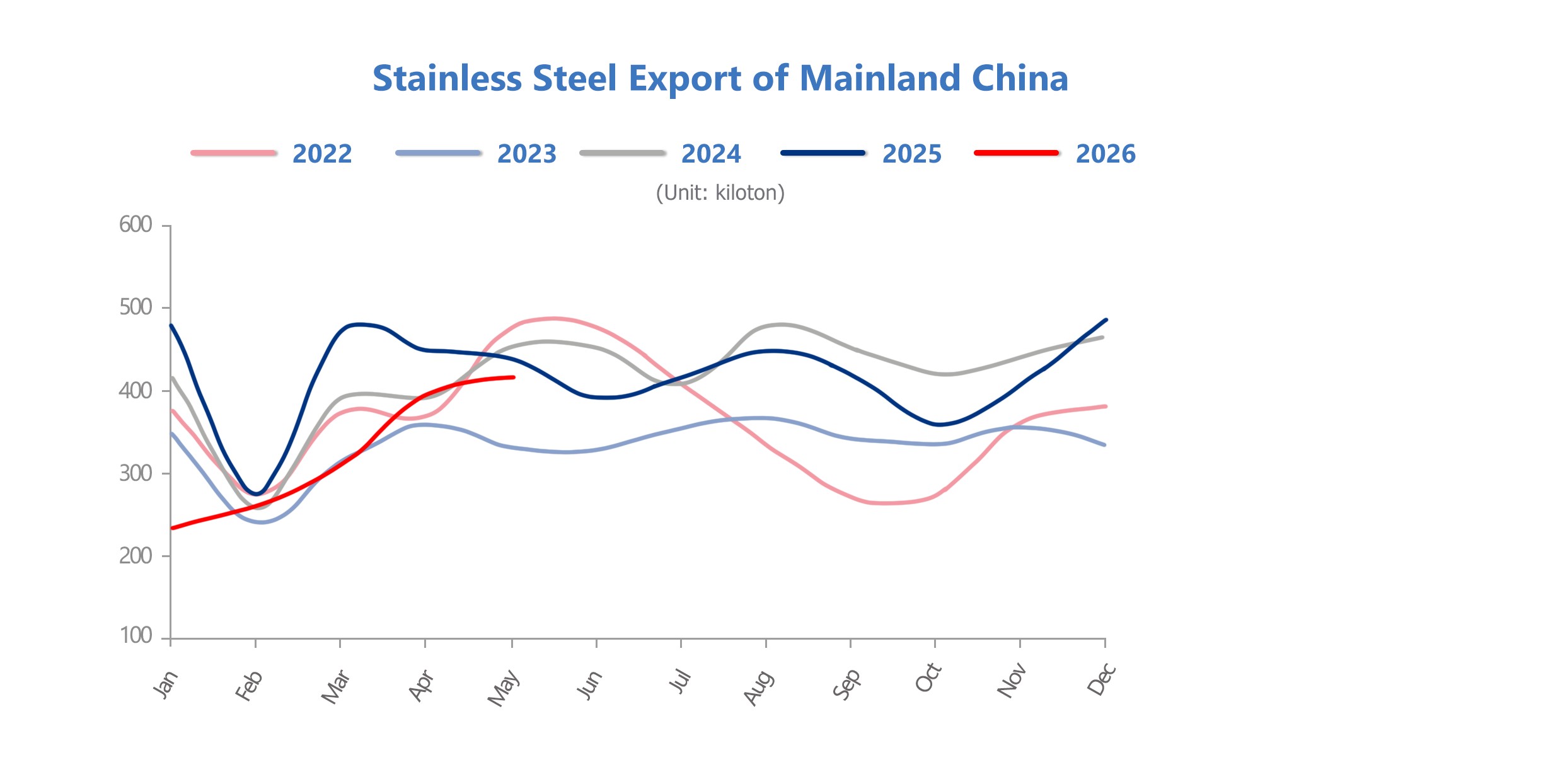

China's Stainless Steel Exports: May 2026 Domestic Stainless Steel Export Volume Increased by 5.4% Month-on-Month

According to China Customs statistics: in May 2026, domestic stainless steel export volume was about 415,700 tons, up 21,300 tons or 5.4% month-on-month; down 20,700 tons or 4.7% year-on-year. From January to May 2026, the cumulative domestic stainless steel export volume was about 1.6129 million tons, down 497,300 tons or 23.6% year-on-year.

Imports by India Increase by 75.8% Year-on-Year

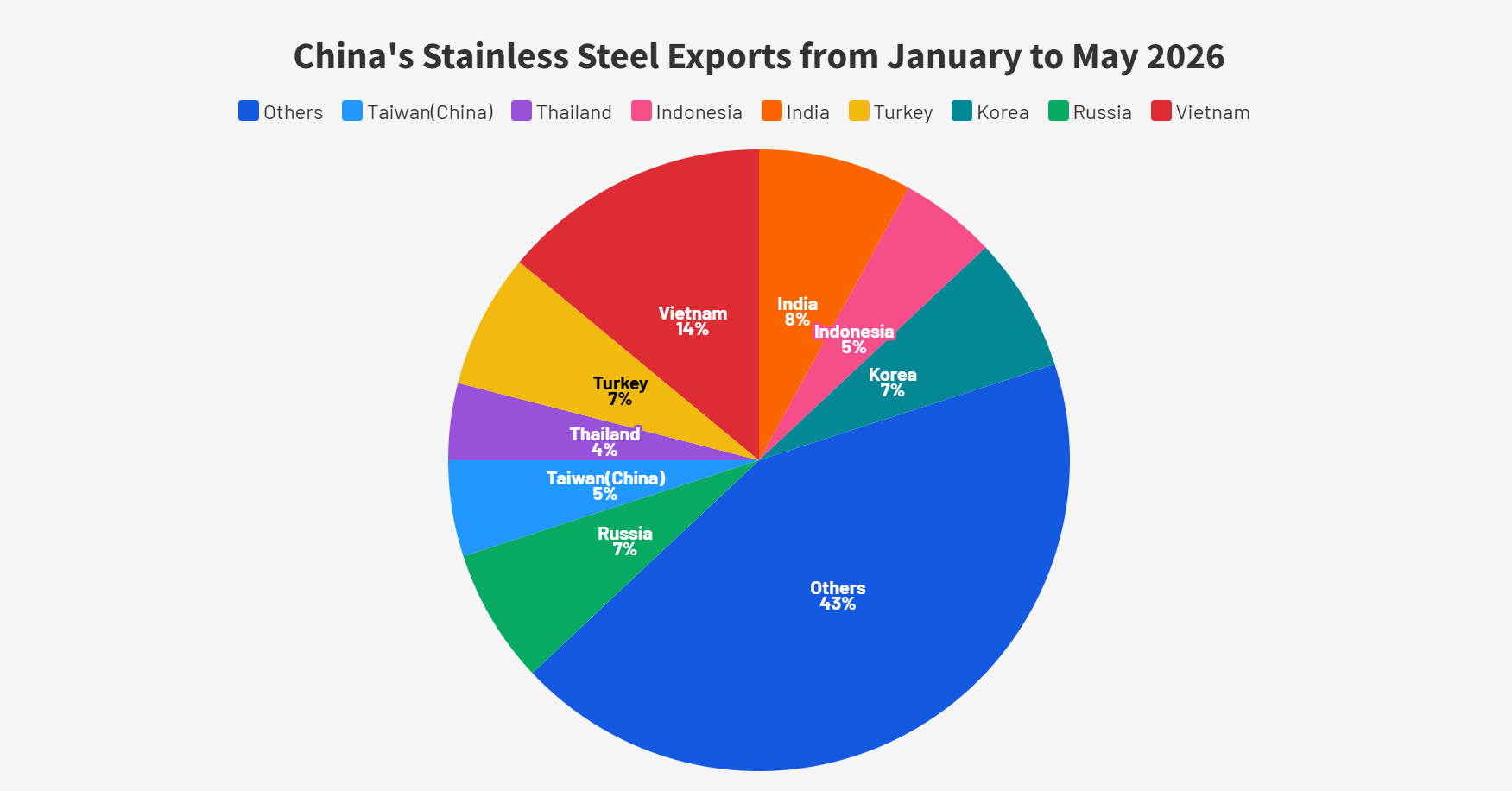

In May 2026, export volumes to mainland China's top ten regions were approximately 274,000 tons, accounting for about 66% of the total. From January to May 2026, the cumulative volume to these regions was about 1.034 million tons, accounting for roughly 64.1%.

In May 2026, export volumes to mainland China's top twenty regions were approximately 342,000 tons, representing about 82.4%. From January to May 2026, the cumulative volume reached around 1.297 million tons, accounting for about 80.4%.

A supply gap emerged in India's domestic market. To meet its domestic downstream demand, the exemption period for India's BIS certification has been repeatedly extended. Since March 2026, domestic stainless steel exports to India have shown an increasing trend, reaching 46,000 tons in May, hitting a 20-month high (since October 2024), representing a month-on-month increase of 10,000 tons and a year-on-year increase of 29,000 tons. The cumulative volume from January to May was around 123,000 tons, up 53,000 tons or 75.8% year-on-year.

In May, the European Union slashed its steel import quotas, sharply raising tariffs on over-quota imports. Consequently, European domestic stainless steel delivery cycles elongated, and prices climbed rapidly, widening the price gap between Chinese and European stainless steel and giving Chinese supply a high cost-performance advantage. As a member of the EU Customs Union, Turkey prioritized its domestic capacity for supply to Europe, which contracted its capacity for domestic sales, causing it to increase external procurement and imports to fill the gap.

Sea Freight: Freight Rates Remain High

Although freight forwarders have disclosed that there will be opportunities for freight rates to fall in two weeks, many viewpoints still hold that freight rates will maintain an upward trajectory or stay at high prices.

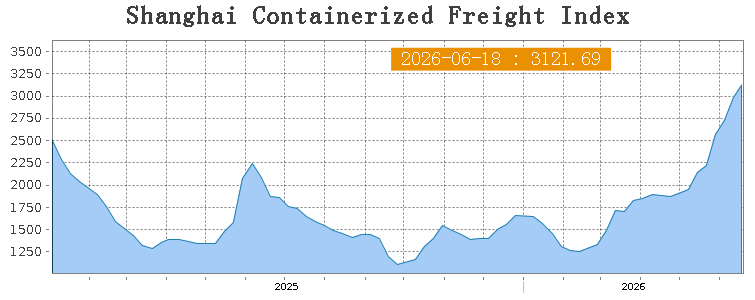

The Chinese export container shipping market continued to maintain strong momentum, with freight rates on most routes rising further, driving the composite index upward. As of June 18, the Shanghai Containerized Freight Index (SCFI) stood at 3121.69 points, up 4.6% from the previous period.

European Route: Shipping demand was generally stable, and the supply-demand relationship was favorable, pushing spot market freight rates up further. On June 18, the market freight rate (ocean freight and ocean surcharges) from Shanghai Port to European base ports was $3,158/TEU, up 3.1% from the previous period. The freight rate from Shanghai Port to Mediterranean base ports was $4,260/TEU, up 2.1%.

North American Route: Shipping demand maintained a positive trend, and space supply was relatively tight, driving market freight rates up further. On June 18, the Shanghai-US West Coast freight rate rose by 11.4% to $5,683/FEU; the Shanghai-US East Coast route rate rose by 8.7% to $6,873/FEU, leaving a price gap of $1,190 between the two.

Persian Gulf Route: Significant progress was made in Middle East geopolitical conditions, as the US and Iran reached a memorandum of understanding. Spot market booking prices fell slightly this week. On June 18, the market freight rate from Shanghai Port to Persian Gulf base ports was $4,753/TEU, down 1.3% from the previous period.

As of June 18, the Drewry World Container Index (WCI) jumped 12% to $3,969/FEU.

Spot rates for the Shanghai-Los Angeles route rose 10% to $5,142/FEU; Shanghai-New York spot rates rose 15% to $6,769/FEU.

Shanghai-Rotterdam rates rose 15% to $4,342/FEU, and Shanghai-Genoa rates rose 12% to $5,756/FEU.

Drewry pointed out that strong peak season demand enabled shipping lines to successfully implement PSS surcharges and FAK, and Drewry expects freight rates to maintain an upward trend in the coming weeks.

The signing of the memorandum of understanding between Iran and the United States improved sentiment in the global shipping market. However, uncertainty remains regarding its implementation and its impact on global shipping. The easing of geopolitical tensions is expected to stabilize oil and bunker fuel prices, potentially mitigating cost pressures for shipping companies.

Kuehne+Nagel: Freight Rates Continue to Climb, Peak Season Market Strengthens Further

In its Global Ocean Market Dynamics report (mid-to-late June), Kuehne+Nagel pointed out that driven by high peak-season demand, the temporary mitigation of US tariffs, and growth in AI and green energy-related cargo flows, high freight rates are expected to extend until the end of July.

Currently, container ship resources remain scarce and charter rates stay high; some shipping lines may consider gradually resuming operations on the Red Sea route.

The US line market maintained its strong upward trend, entering the peak season rhythm ahead of schedule. The concentrated release of cargo volumes in the short term serves as the core driver, and this wave of concentrated shipments is expected to persist until at least early July; the growth rate of cargo volumes may see a phased slowdown only after policies are officially implemented. Comprehensively judging, July is highly likely to serve as a phased peak window for this round of freight rate increases, with a freight rate turning point appearing in late July at the earliest. However, if traditional peak season demand continues to materialize, the timing for freight rates to peak remains uncertain.