Stainless Insights in China from July 14th to July 18th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,000 | 11 | 0.60% |

| Foshan | 2,045 | 11 | 0.59% | ||

| Hongwang | Wuxi | 1,905 | 4 | 0.24% | |

| Foshan | 1,915 | 13 | 0.71% | ||

| 304/NO.1 | ESS | Wuxi | 1,825 | 10 | 0.58% |

| Foshan | 1,840 | 13 | 0.74% | ||

| 316L/2B | TISCO | Wuxi | 3,530 | 37 | 1.09% |

| Foshan | 3,605 | 42 | 1.23% | ||

| 316L/NO.1 | ESS | Wuxi | 3,375 | 28 | 0.87% |

| Foshan | 3,400 | 24 | 0.74% | ||

| 201J1/2B | Hongwang | Wuxi | 1,175 | 8 | 0.80% |

| Foshan | 1,195 | 24 | 2.26% | ||

| J5/2B | Hongwang | Wuxi | 1,075 | 18 | 1.94% |

| Foshan | 1,095 | 24 | 2.50% | ||

| 430/2B | TISCO | Wuxi | 1,120 | 0 | 0.00% |

| Foshan | 1,110 | 0 | 0.00% |

TREND || Policy Support from MIIT & Improved Supply-Demand Dynamics Fuel Ongoing Uptrend

At a press conference held by the State Council Information Office on July 18, the Ministry of Industry and Information Technology (MIIT) announced that action plans aimed at stabilizing growth in ten key industries—including steel, nonferrous metals, petrochemicals, and building materials—are soon to be released. MIIT will promote structural adjustments, improve supply quality, and eliminate outdated production capacity in these sectors.

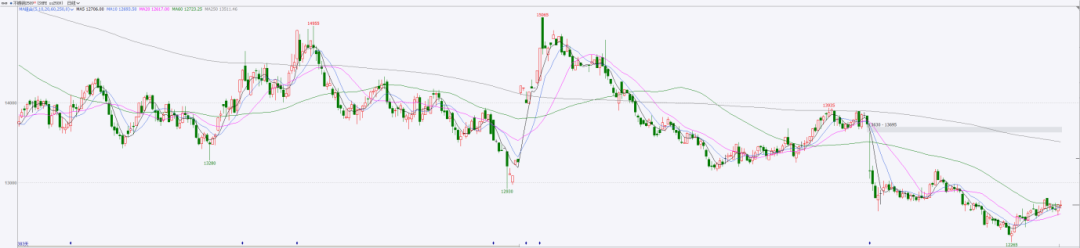

Last week, stainless steel spot prices in the Wuxi market saw a mild rebound, mirroring the futures market. Prices fluctuated within a narrow range, while raw material prices stabilized and steel mill profits showed signs of recovery. July production schedules declined, reducing the volume of arriving goods and easing supply-side pressure. Inventories recorded a slight dip. As of Friday, the main stainless steel futures contract rose by US$1.4/MT week-on-week to US$1910/MT, a 0.08% increase. The night trading session gained further momentum from the MIIT policy boost, with futures prices rising to US$1925/MT amid increased positions.

300 Series: Supply Pressure Eases, Inventory Sees Modest Drawdown

Prices for 304 stainless steel rose slightly last week. By Friday, the mainstream base price for private cold-rolled 304 four-foot coils in Wuxi reached US$1865/MT, while hot-rolled coils were quoted at US$1825/MT—both up by US$14/MT from last week.

The Central Financial and Economic Affairs Commission recently emphasized the need to curb disorderly low-price competition and promote the exit of obsolete capacities, raising market expectations for policy enforcement. This macro-level optimism is supporting a price floor, though an oversupplied market continues to limit the room for a rebound. Futures trading reflects intensified long-short competition.

The positive signal from MIIT has lifted market sentiment, boosting futures with increased open interest. With steel mills reducing production schedules in July, supply-side pressure has eased. On the demand side, the price rebound has sparked speculative buying, improving transaction levels during certain periods and contributing to a modest inventory drawdown.

200 Series: Prices Continue Rising, Market Activity Improves

Prices for 201 stainless steel were raised across the board during the week:

201J2 cold-rolled: up US$21/MT to US$1050/MT (base price)

201J1 cold-rolled: up US$14/MT to US$1155/MT (base price)

201J1 hot-rolled: up US$7/MT to US$1120/MT

Early in the week, futures prices fluctuated while traders held firm on their offers. 201J2 cold-rolled prices hovered around US$1040/MT, with some attempting a further increase to US$1050/MT. However, downstream acceptance of higher prices was limited, and buying slowed as a result.

In the latter half of the week, futures turned bullish and boosted market sentiment. Traders began holding back inventory in anticipation of further price increases, making low-priced stock harder to find. Cold- and hot-rolled inventory levels saw a slight reduction.

400 Series: Inventories Continue to Accumulate, 430 Prices Remain Stable

Prices for 430 stainless steel remained stable last week. In Wuxi's spot market:

State-owned 430 cold-rolled products were quoted around US$1125/MT

State-owned 430 hot-rolled products held steady at US$1040/MT

Both were unchanged from the previous week. However, overall inventories continued to rise.

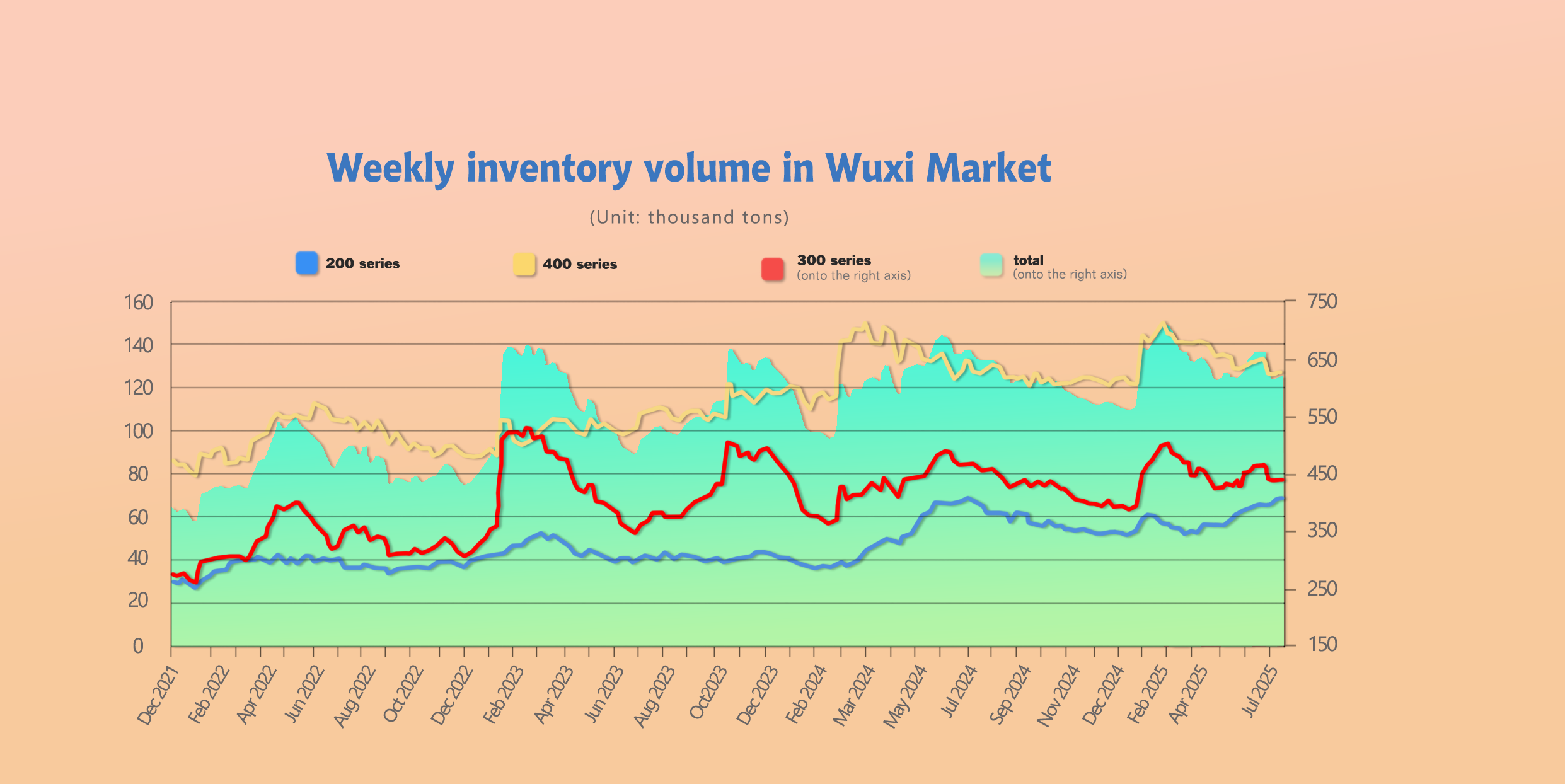

INVENTORY || 2,000 Tons Drawn Down! Supply-Demand Dynamics Improve, Just Waiting for a Final Push

As of July 17th, total inventory in Wuxi sample warehouses decreased by 2,113 tons to 629,486 tons. Breakdown:

200 Series: 1,099 tons down to 67,461 tons.

300 Series: 2,244 tons down to 434,570 tons.

400 Series: 1,130 tons up to 127,455 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

|

Jul 10th |

68,560 | 436,814 | 126,325 | 631,699 |

| Jul 17th | 67,461 | 434,570 | 127,455 | 629,486 |

| Difference | -1,099 | -2,244 | 1,130 | -2,213 |

200 Series: Fewer Arrivals, Accelerated Inventory Drawdown

Looking at spot inventory structure, the arrival of resources from Hongwang decreased last week, slightly easing supply pressure. During the week, cold-rolled 201 prices were raised by US$21/MT. Traders held firm on their quotes, and improved sentiment among downstream buyers helped accelerate the destocking of cold-rolled products.

Hot-rolled 201 prices remained mostly stable, but overall transaction volumes increased week-on-week due to favorable market conditions, accelerating the drawdown of hot-rolled inventories.

With the rebound in cold-rolled 201 prices last week, traders raised their previous low quotes, and the market outlook remains optimistic. Short-term prices for 201 are expected to continue fluctuating with a strong bias. Inventories are likely to keep declining next week.

300 Series: Mills Raise Prices, Market Demand Picking Up

From the spot inventory perspective, hot-rolled arrivals in Jiangyin remained steady last week, while cold-rolled supply to the market declined, easing some supply pressure. After agents of TISCO made concentrated end-of-month pickups, most are now operating on low inventory levels and maintaining a cautious stance, leading to some accumulation in upstream warehouses.

Following contract rollovers in the futures market, prices fluctuated. TSINGAHSAN opened with price increases, prompting agents to slightly raise their selling prices. Combined with stabilized raw material costs, this led to some improvement in downstream procurement, and inventories saw a minor reduction.

Production cuts by steel mills may continue, reducing market arrivals and easing supply-side pressure. With both futures and spot prices stabilizing, market confidence has started to recover, and demand is gradually improving.

On the macro front, supportive domestic policies remain in place, and overseas interest rate cuts are expected soon. However, the market remains in a tug-of-war between bulls and bears. Inventory is expected to continue a slight decline next week, with ongoing attention on mill production and transaction performance in the market.

400 Series: Raw Material Prices Stabilize, Downstream Maintains Just-in-Time Buying

From the current spot inventory structure, cold-rolled inventories from JISCO continued to decline last week, though the reduction was smaller than the previous week. In contrast, both cold- and hot-rolled spot inventories from TISCO increased significantly, leading to an overall noticeable rise in stock levels.

Last week saw a substantial increase in deliveries from steel mills, while downstream demand for 400 series stainless remains mostly limited to just-in-time procurement, with no major improvement—resulting in ongoing inventory accumulation.

Prices for 430 cold-rolled remained stable. Market activity was generally moderate, with downstream purchases focused on immediate needs. Deliveries from major mills increased, raising overall supply and keeping prices steady for now.

On the cost side, raw material support remains solid. However, given the evident inventory buildup in 400 series stainless steel, upward price momentum is weak. Moving forward, attention will focus on the procurement policies for high-chromium raw materials from major mills in August and downstream demand trends, which will influence the price outlook for 430 stainless steel.

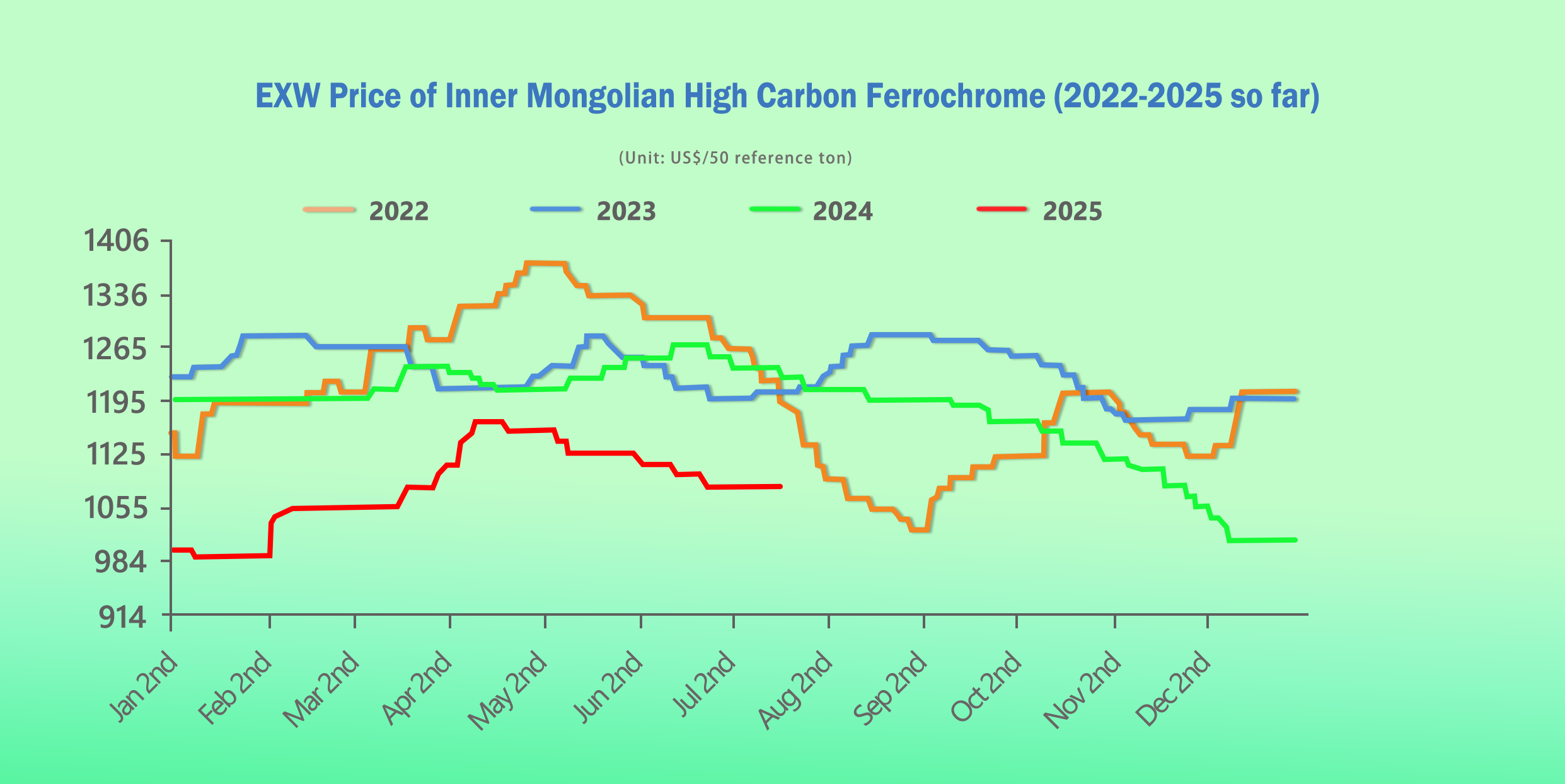

RAW MATERIALS || July Stability Holds — Will the Market Replay the Scenario from Three Years Ago?

As major steel mills approach their procurement bidding period in late July, a wait-and-see sentiment has grown in the high-carbon ferrochrome market, with prices continuing to hold steady.

In terms of costs, last week’s mainstream ex-factory price for high-nickel pig iron remained steady at US$126/nickel point, and ferrochrome prices held firm at US$1083/50 reference ton. The theoretical production cost for stainless steel 304 cold-rolled stood at US$1875/MT, while hot-rolled 304 was at US$1805/MT.

Mainstream ex-factory prices for high-carbon ferrochrome stayed within the US$1082-US$1111/50 reference ton range. With the August procurement bidding period approaching for major mills, market participants are taking a cautious stance. Transaction volumes have not seen significant growth, but cost support for 400 series stainless steel remains relatively solid.

In the first half of 2025, high-carbon ferrochrome prices showed a pattern of rising first and then falling. Overall, price levels stayed below the five-year moving average, though the trend within the year has been relatively strong.

Throughout the first half of the year, high-carbon ferrochrome prices moved through one phase of increases followed by a decline. From January to April, mainstream ex-factory quotes for high-carbon ferrochrome rose steadily. By mid-April, prices had increased by a total of US$169/50 reference ton—up 16.9%.

This upward movement was primarily driven by the impact of the Spring Festival travel rush and holiday period in January–February, followed by a surge in post-holiday demand in March–April. Downstream buying intensified, pushing mainstream ferrochrome prices up to the first-half peak range of US$1167-US$1195.5/50 reference ton.

However, this price rally encouraged an increase in production. Entering the second quarter, market supply of high-carbon ferrochrome expanded significantly, shifting the price trend from bullish to bearish. Prices began to decline, further pressured by falling costs of ore and coke. By late April, ferrochrome prices dropped sharply from the high of US$1195 to US$1111/50 reference ton—a drop of 7.23%.

Overall, high-carbon ferrochrome prices in the first half of 2025 followed a pattern of strength followed by weakness. This was primarily driven by noticeable shifts in supply and demand, as well as significant changes in production costs. When compared with historical data, the price trend in 2025 closely resembles that of 2022.

SUMMARY || Market Prices Remain Stable, with Some Improvement in Transactions

300 Series: Current prices are fluctuating within a narrow range. During the off-season, downstream purchases are primarily driven by just-in-time demand for low-priced goods, with limited acceptance of higher-priced resources. On the supply side, production cuts by steel mills have yet to be confirmed, and current market supply pressure remains high, with ample inventory in circulation. Expectations of U.S. Federal Reserve rate cuts have cooled, while domestic economic data remains relatively strong—intensifying the tug-of-war between bullish and bearish market sentiment. In the short term, 304 cold-rolled and hot-rolled spot prices are expected to follow futures market movements.

200 Series: Raw material prices for copper and manganese remain at elevated levels, providing cost support for 201 stainless steel. Steel mill output has decreased, leading to a potential reduction in available market supply in the coming period. Boosted by macro sentiment and futures performance during the week, market confidence is leaning optimistic. In the short term, 201 prices are expected to remain firm and stable.

400 Series: Last week, retail prices for high-carbon ferrochrome remained stable, continuing to support the production costs of 400 series stainless steel. However, downstream demand showed no significant growth, while mill and trader inventories increased, leading to a slight build-up. As a result, 430 prices are expected to mostly hold steady next week.

MACRO || A Brief Analysis of China’s Stainless Steel Coil Import and Export Data for June 2025

I. Import and Export Volumes of Stainless Steel Coils (Including Coils and Strips)

1. Stainless Steel Coil and Strip Imports – June 2025

In June 2025, China imported approximately 67,400 tons of stainless steel coils (width ≥ 600mm), down 27,700 tons month-on-month (-29.1%) and down 15,800 tons year-on-year (-19.0%).

From January to June 2025, cumulative imports of stainless steel coils (width ≥ 600mm) reached approximately 617,100 tons, down 21,900 tons year-on-year (-3.4%).

In June 2025, imports of stainless steel strips (width < 600mm) totaled approximately 2,260 tons, down 291 tons month-on-month (-11.4%) and down 644 tons year-on-year (-22.2%).

From January to June 2025, cumulative imports of stainless steel strips (width < 600mm) amounted to approximately 13,600 tons, a decrease of 2,165 tons from the same period last year (-13.7%).

In total, June 2025 saw stainless steel coil (coils + strips) imports of approximately 69,600 tons, a 28.66% decline month-on-month and a 19.11% drop year-on-year.

For the first half of 2025, total stainless steel coil (coils + strips) imports were approximately 630,700 tons, down 3.68% from the same period last year.

2. Stainless Steel Coil and Strip Exports – June 2025

In June 2025, China exported approximately 269,700 tons of stainless steel coils (width ≥ 600mm), a 29,700-ton decrease month-on-month (-9.9%) and down 47,600 tons year-on-year (-15.0%).

From January to June 2025, cumulative exports of stainless steel coils (width ≥ 600mm) reached 1,731,700 tons, up 39,000 tons year-on-year (+2.3%).

In June 2025, stainless steel strip (width < 600mm) exports were approximately 27,200 tons, down 5,499 tons month-on-month (-16.8%) and down 4,566 tons year-on-year (-14.4%).

From January to June 2025, cumulative stainless steel strip exports reached 189,200 tons, up 28,200 tons year-on-year (+17.5%).

Overall, June 2025 exports of stainless steel coils (coils + strips) totaled approximately 296,900 tons, a 10.60% decrease month-on-month and a 15.21% decline year-on-year.

For January to June 2025, total stainless steel coil (coils + strips) exports were approximately 1,921,000 tons, up 3.45% year-on-year.

3. Net Stainless Steel Coil Exports – June 2025

In June 2025, China’s net export volume of stainless steel coils (coils + strips) was approximately 227,300 tons, down 3.09% month-on-month and down 13.93% year-on-year.

From January to June 2025, cumulative net exports reached 1,290,200 tons, an increase of 88,200 tons, or +7.34% compared to the same period last year.

II. Top Five Import Source Regions

China’s stainless steel coil imports remained highly concentrated among a few countries. In June 2025, imports from Indonesia, Japan, and South Korea totaled 65,500 tons, accounting for 94.1% of the nation’s total imports. The top five source regions accounted for 67,100 tons, or 96.5% of the total.

From January to June 2025, imports from these three countries totaled 604,700 tons, representing 95.87% of China’s total imports, while the top five regions combined accounted for 611,800 tons, or 97%.

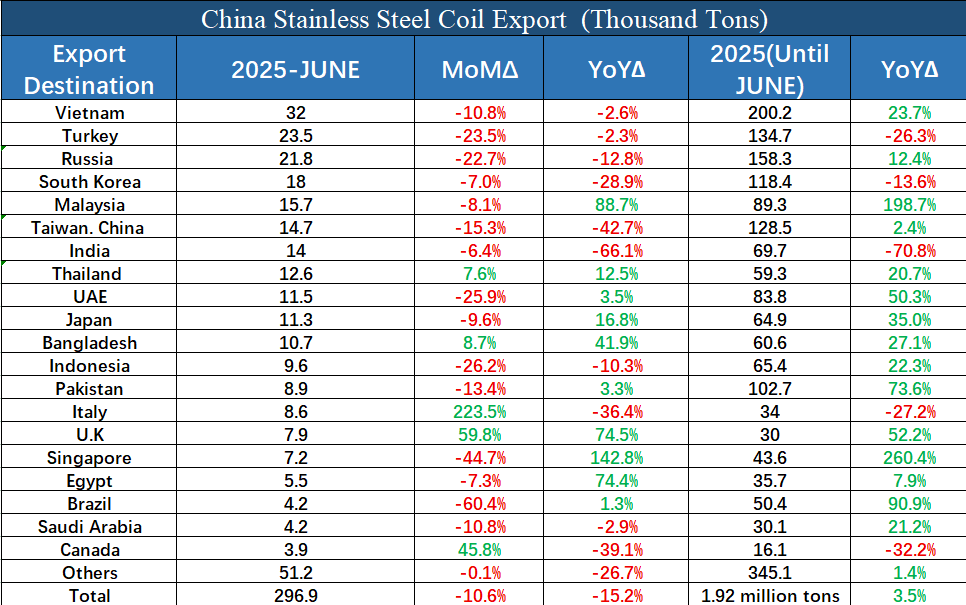

III. Top Ten Export Destinations

In June 2025, China exported 175,100 tons of stainless steel coils to its top ten destination markets, accounting for approximately 58.97% of total exports for the month.

From January to June 2025, cumulative exports to these top ten regions reached 1,107,100 tons, representing about 57.64% of total stainless steel coil exports during the first half of the year.

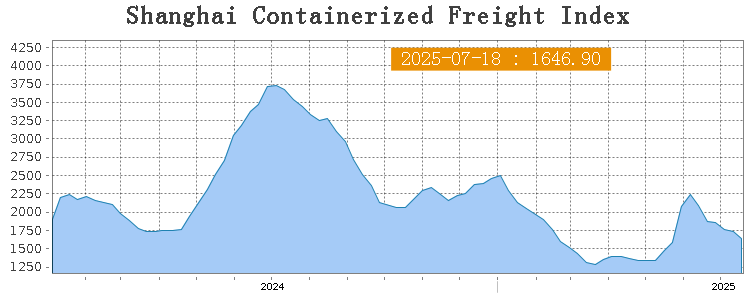

SEA FREIGHT || Market Remains Generally Stable, Freight Rates Fall on Most Routes

Last week, China’s container export shipping market remained generally stable, though freight rates declined on most routes, dragging down the overall composite index.

According to the latest data released by China’s General Administration of Customs, China’s goods trade imports and exports grew by 2.9% year-on-year in the first half of 2025, reaching a record high for the same period. Exports alone rose by 7.2% year-on-year. Despite challenges from unilateralism and protectionism, China’s foreign trade has withstood the pressure—maintaining steady growth in scale and achieving improvements in quality. This continued resilience will provide long-term support for China’s containerized export shipping market.

On July 18th, the Shanghai Containerized Freight Index (SCFI) fell 5% to 1646.9 points.

Europe/ Mediterranean:

According to data released by the Centre for European Economic Research (ZEW), the Eurozone ZEW Economic Sentiment Index for July rose to 36.1, while Germany's index climbed to 52.7, marking the highest level since February 2022. The European economy continues to show signs of recovery.

Meanwhile, U.S. President Trump recently announced a 30% tariff on imports from the European Union starting August 1. In response, the EU has drafted a countermeasure involving a tariff list on U.S. service sectors. The transatlantic trade relationship remains highly uncertain.

On July 18th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$2079/TEU, which decreased by 1%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$2528/TEU, which dip 5.2% from previous week.

North America:

Last week, overall transportation demand remained steady, but freight rates declined slightly.

According to the U.S. Bureau of Labor Statistics, the Consumer Price Index (CPI) in June rose 0.3% month-on-month and 2.7% year-on-year, the highest in four months. Import prices are showing clear upward pressure, and the pass-through effect of tariffs on consumer goods is intensifying, posing a future inflationary risk.

Last week, the shipping market lacked further momentum for demand growth. On the U.S. East Coast route, due to uncertainty over upcoming tariff policies, shippers were cautious about placing new orders, which put downward pressure on freight rates.

On July 18th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$2142/FEU and US$3612/FEU, reporting 2.4% and 13.4% slide accordingly.

The Persian Gulf and the Red Sea:

On July 18th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf shrank 17.8% to US$1321/TEU.

Australia & New Zealand:

On July 18th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand gained 2.1% to US$1042/TEU.

South America:

On July 18th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports decreased 9.5% to US$5628/TEU.