Stainless Insights in China from May 19th to May 25th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,075 | 11 | 0.58% |

| Foshan | 2,120 | 11 | 0.57% | ||

| Hongwang | Wuxi | 1,965 | 1 | 0.08% | |

| Foshan | 1,985 | 0 | 0.00% | ||

| 304/NO.1 | ESS | Wuxi | 1,900 | -4 | -0.24% |

| Foshan | 1,920 | 7 | 0.39% | ||

| 316L/2B | TISCO | Wuxi | 3,500 | 23 | 0.67% |

| Foshan | 3,580 | 17 | 0.49% | ||

| 316L/NO.1 | ESS | Wuxi | 3,365 | 13 | 0.39% |

| Foshan | 3,390 | 14 | 0.43% | ||

| 201J1/2B | Hongwang | Wuxi | 1,260 | 0 | 0.00% |

| Foshan | 1,235 | -4 | -0.37% | ||

| J5/2B | Hongwang | Wuxi | 1,140 | -4 | -0.41% |

| Foshan | 1,135 | -4 | -0.41% | ||

| 430/2B | TISCO | Wuxi | 1,160 | -3 | -0.27% |

| Foshan | 1,145 | -7 | -0.68% |

TREND || China–U.S. Joint Statement Indirectly Supports Demand for 400 Series Stainless Steel

Stainless steel futures prices showed weak and volatile performance last week. At the beginning of the week, futures extended their downward trend from last week’s close, but later stabilized. However, the overall technical pattern has deteriorated, with prices retreating to the upper edge of a previous minor consolidation range. After a failed attempt to break higher, the fluctuation range widened, suggesting a lack of momentum for any short-term rallies. Trading activity was lighter compared to last week, and open interest declined slightly as the market largely adopted a wait-and-see attitude. The main stainless steel futures contract closed at US$1945/MT, up 1.93% for the week, with a weekly high of US$1965/MT.

In the spot market, stainless steel prices fell by US$4.2-US$14/MT last week.

300 Series: Production Shift Shows Results, Inventory Slightly Reduced

The 304 spot market declined slightly last week. As of Friday, mainstream base prices for private cold-rolled four-foot coils in Wuxi were quoted at US$1920/MT, while private hot-rolled prices were at US$1900/MT—both down by US$14/MT compared to last Friday.

The central bank’s interest rate cut at the start of the week briefly lifted market sentiment, and spot transactions were acceptable in the early week as downstream buyers increased purchases, leading to inventory reduction. However, after the initial emotional lift wore off, commodity prices pulled back slightly in the latter half of the week. End-user sentiment turned cautious again, purchases returned to a "just-in-time" basis, market arrivals decreased, and inventory reduction slowed.

200 Series: Mills Continue to Cut Prices, Spot Transactions Remain Limited

Prices for 201 fell last week. cold-rolled 201J2 was quoted atSU$1105/MT, cold-rolled 201J1 at US$1225/MT, and hot-rolled 201J1 at US$1195/MT.

The futures market fluctuated throughout the week, and market sentiment turned increasingly cautious. On Thursday and Friday, Tsingshan opened with two rounds of price cuts—dropping both cold and hot-rolled 201 by US$14/MT each time. Spot prices closely followed futures trends, and low-priced resources appeared in the market. Downstream buyers showed limited interest, and both cold-rolled and hot-rolled inventories saw slight increases.

400 Series: Improved Sales, Accelerated Inventory Reduction

The 430 market saw weaker prices last week. In Wuxi’s spot market, prices for state-owned 430 cold-rolled dropped by US$7/MT to around US$1160/MT, while hot-rolled remained stable at US$1085/MT—unchanged from last weekend.

Following the release of the joint statement from the China–U.S. trade talks in Geneva, expectations grew for adjustments to stainless steel export tariffs, boosting futures prices and lifting spot prices in tandem. This helped ease overly pessimistic views on exports. While the direct impact on stainless steel exports is limited, improved export expectations for downstream products made in China—such as home appliances and kitchenware—are indirectly supporting demand for 400 series stainless steel.

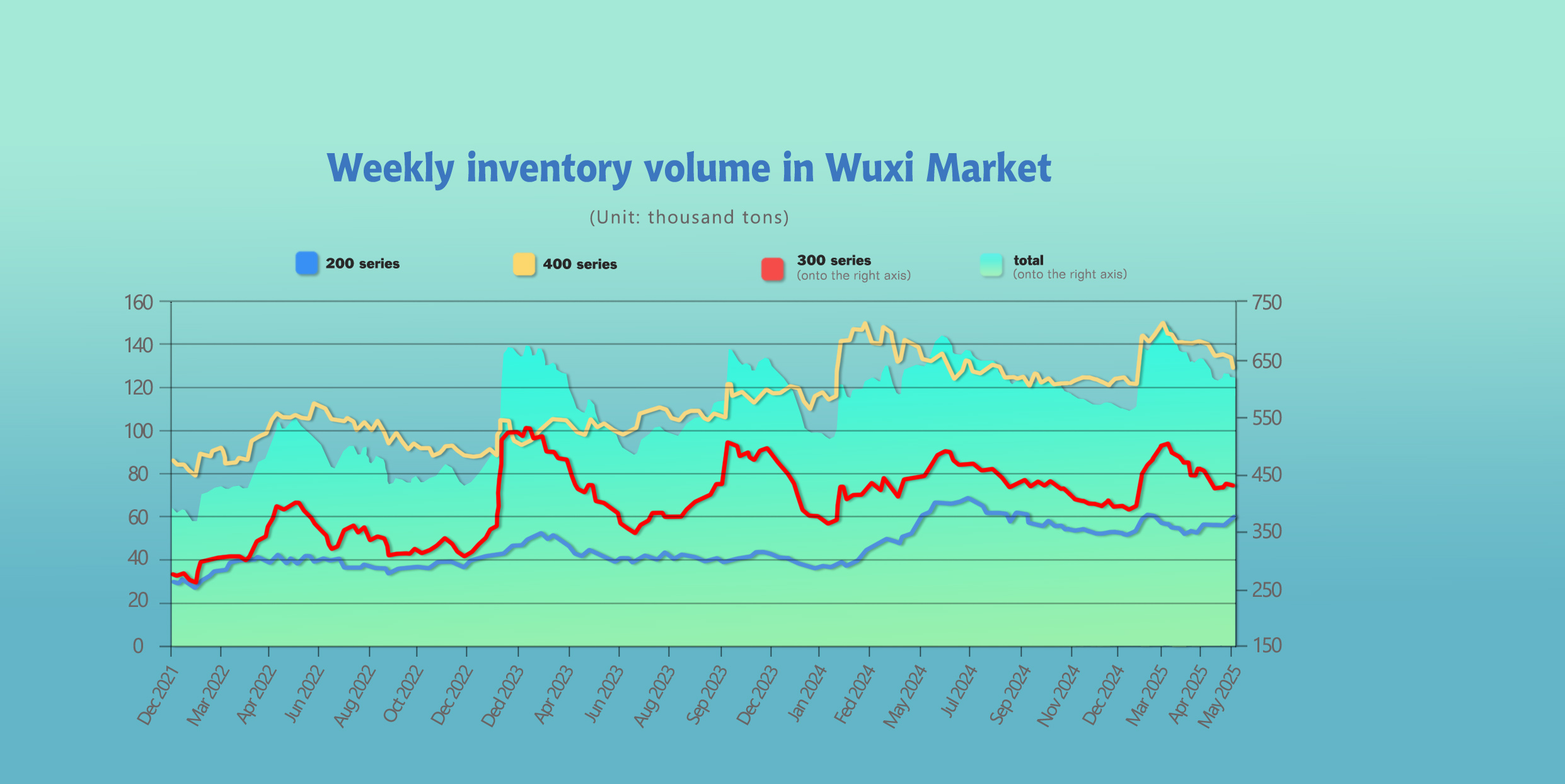

INVENTORY || Continuous Inventory Decline Has Limited Market Impact

As of May 22nnd, total inventory in Wuxi sample warehouses decreased by 8,804 tons to 611,061 tons. Breakdown:

200 Series: 1,595 tons up to 59,709 tons.

300 Series: 5,169 tons down to 424,122 tons.

400 Series: 5,230 tons down to 127,230 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| May 15th | 58,114 | 429,291 | 132,460 | 619,865 |

| May 22nd | 59,709 | 424,122 | 127,230 | 611,061 |

| Difference | 1,595 | -5,169 | -5,230 | -8,804 |

300 Series: Production Shift Takes Effect, Inventory Slightly Reduced

Futures and spot prices fluctuated downward during last week, and downstream buyers remained cautious. Steel mills continue to operate at a loss, while costs remain high. As production shifts out of the 300 series, available market supply has decreased.

The recent domestic reserve requirement ratio and interest rate cuts have slightly boosted market sentiment. However, given the weak fundamentals, prices remain range-bound. As steel mill production declines, the supply-demand balance is gradually improving. Inventory may continue to decrease slightly in the coming period. Continued attention should be paid to transaction volumes and production trends at the mills.

200 Series: Ongoing Deliveries Drive Continued Inventory Growth

From the structure of spot inventory, resources from mills like Hongwang continued to flow into the market, keeping supply at high levels. During the week, Tsingshan lowered its opening price for 201 cold-rolled, and traders followed with downward price adjustments. Downstream buyers turned more cautious, leading to a slight buildup in cold-rolled inventory. With mill openings leading to falling spot prices, the market has adopted a pessimistic outlook for future price trends. Supply pressure is mounting, and 200 series inventory is expected to continue increasing next week.

400 Series: Terminal Demand Rises, Inventory Continues to Decline

The primary factor was the easing of China-U.S. tariffs, which led to a rebound in stainless steel demand and accelerated inventory reduction. Last week, 430 cold-rolled prices remained stable, while downstream demand saw a clear increase, accelerating the depletion of spot inventory. Raw material prices remained stable, providing moderate cost support. Attention should be given to June’s procurement policies for high-carbon ferrochrome, which may impact 430 prices.

SUMMARY || Steel Mill Output Declines, but Stainless Steel Supply-Demand Imbalance Persists

Stainless steel prices declined last week. On the demand side, purchases remain largely driven by essential needs. Although steel mills have slightly reduced production schedules, the oversupply situation remains difficult to reverse. Social inventory has decreased somewhat but still remains at a high level, with sufficient spot availability. Market attention remains on downstream consumption capacity, mill production plans, and the pace of inventory depletion. In the short term, stainless steel prices are expected to fluctuate within a range.

300 Series: Supply Pressure Eases, but High Inventory Caps Price Rebound

The current market sees some relief in supply, as high costs have prompted steel mills to shift production away from the 300 series, reducing available market resources. On the demand side, as prices remain low and fluctuate within a narrow range, low-priced resources are gradually being absorbed, leading to a slight inventory reduction. However, the pace of destocking has slowed, and high inventory levels continue to suppress the extent of any price rebound. On the macro level, the tug-of-war between bullish and bearish forces at home and abroad has intensified, and expectations remain for more domestic policy measures. As fundamentals play a stronger role in pricing, stainless steel prices are likely to fluctuate along with the futures market in the short term.

200 Series: Macro Supportive Policies in Place, but Demand Remains Weak

Recent macro policy support and strength in the non-ferrous sector have driven copper and manganese prices to remain elevated, continuing to support 201 production costs. However, the market is gradually entering a seasonal off-peak period, and there has been no significant improvement in downstream demand. With mills continuing to deliver material, supply pressure in the market persists. Under the current supply-demand dynamics, 201 prices are expected to remain stable with a slight downward bias.

400 Series: Cost Support Holds, Inventory Declines Ease Pressure

High-carbon ferrochrome retail prices have remained weak and stable, aligning closely with prices set in the latest round of steel mill tenders. This provides moderate cost support for 400 series stainless steel. Coupled with accelerated inventory reduction in the spot market, supply-side pressure has eased. As a result, 430 prices are expected to remain stable next week.

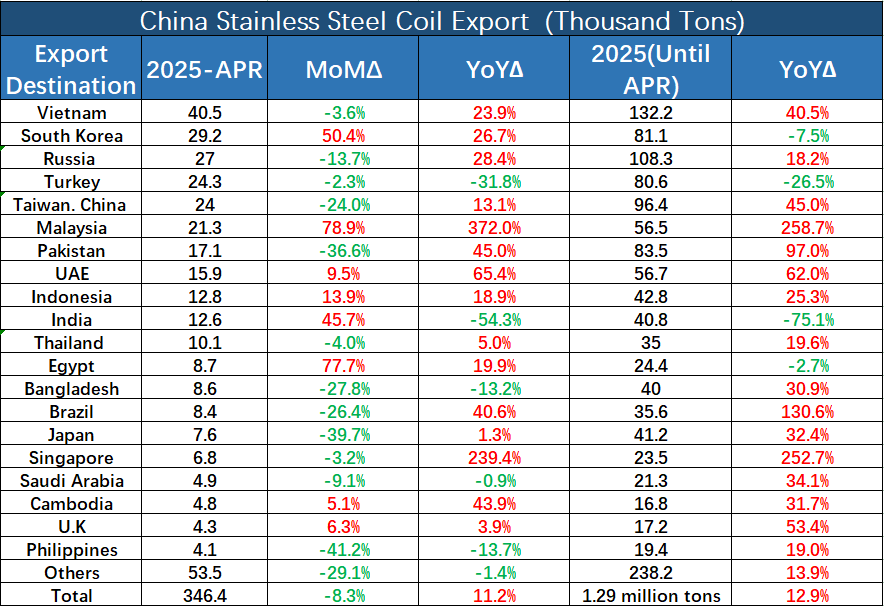

MACRO || Malaysia Imported 21,300 Tons of Coil from China in April, Up 372% Year-on-Year

In April 2025, China exported approximately 307,300 tons of stainless steel plate and coil (with a width ≥600mm), representing a month-on-month decrease of 36,200 tons, or 10.5%, but a year-on-year increase of 23,700 tons, or 8.4%.

In April 2025, the top 10 destination regions for China’s stainless steel coil exports accounted for around 224,700 tons, which is about 64.85% of the total.

From January to April 2025, the cumulative export volume to these top 10 regions was approximately 778,800 tons, accounting for 60.28% of total exports during the period.

South Korea Imposes Anti-Dumping Duties on Stainless Steel Plate and Coil from China

On May 16, 2025, South Korea's Ministry of Economy and Finance issued Decree No. 1126, announcing the continuation of five-year anti-dumping duties on stainless steel plate and coil (Flat-rolled Products of Stainless Steel) with thickness not exceeding 8 mm, originating from mainland China, Indonesia, and Taiwan.

For mainland China, the anti-dumping duty ranges from 23.69% to 25.82%.

For Taiwan, from 7.17% to 9.47%

For Indonesia, the rate is 25.82%

At the same time, the Ministry has reached price undertakings with certain suppliers (see Annex 2 for the supplier list). These suppliers will not be subject to anti-dumping duties as long as they comply with the agreed price terms.

The products with Korean tax numbers involved in this case are as follows, but some of them are not subject to the above anti-dumping measures:

7219.12.1010、7219.12.1090、7219.12.9000、7219.13.1010、7219.13.1090、7219.13.9000、7219.14.1010、7219.14.1090、7219.14.9000、7219.22.1010、7219.22.1090、7219.22.9000、7219.23.1010、7219.23.1090、7219.23.9000、7219.24.1010、7219.24.1090、7219.24.9000、7219.31.1010、7219.31.1090、7219.31.9000、7219.32.1010、7219.32.1090、7219.32.9000、7219.33.1010、7219.33.1090、7219.33.9000、7219.34.1010、7219.34.1090、7219.34.9000、7219.35.1010、7219.35.1090、7219.35.9000、7219.90.1010、7219.90.1090、7219.90.9000、7220.11.1010、7220.11.1090、7220.11.9000、7220.12.1010、7220.12.1090、7220.12.9000、7220.20.1010、7220.20.1090、7220.20.9000、7220.90.1010、7220.90.1090 and 7220.90.9000

The following products are not subject to the above anti-dumping measures:

1.Steel products conforming to ASTM (American Society for Testing and Materials) standards S31254 and N08367.

2.200-series nickel-based steel products with nickel content less than 6% and manganese content greater than or equal to 3%. (Tax number involved: 7219.12.1010、7219.13.1010、7219.14.1010、7219.22.1010、7219.23.1010、7219.24.1010、7219.31.1010、7219.32.1010、7219.33.1010、7219.34.1010、7219.35.1010、7219.90.1010、7220.11.1010、7220.12.1010、7220.20.1010 and 7220.90.1010 )

3.Hot-rolled steel products with a width ≥ 2000 mm.

4.Hot-rolled 316 or 316L stainless steel coil/plate with a thickness between 3.0 mm and 4.0 mm (inclusive) and a width ≥ 1524 mm.

5.Steel products that conform to China’s national standards (GB) for 2Cr13, 3Cr13, 4Cr13, or 6Cr13, with a thickness < 3.0 mm, width < 400 mm, and hardness between HV250 and HV350 (inclusive).

6.Steel products in which the proportions of carbon, silicon, manganese, phosphorus, sulfur, nickel, chromium, molybdenum, copper, and nitrogen all meet the specified compositional requirements.

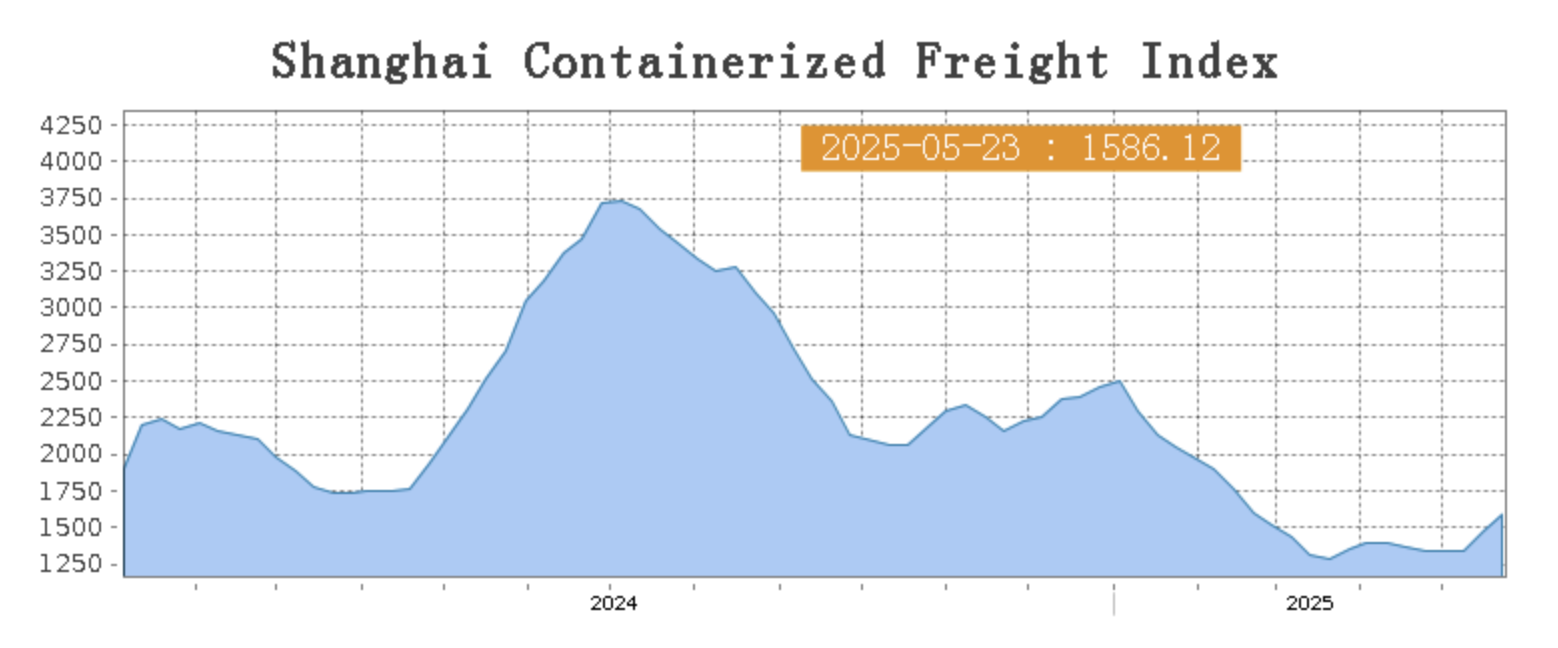

SEA FREIGHT || Market Remains Generally Stable with Slight Fluctuations on Some Routes

China's export container shipping market continued to show positive momentum, with freight rates on most long-haul routes maintaining an upward trend, driving the composite index higher.

Last week, China’s container export shipping market remained generally stable, with slight fluctuations observed on some routes. On May 23rd, the Shanghai Containerized Freight Index (SCFI) rose 11.8% to 1586.12 points.

Europe/ Mediterranean:

On May 23rd, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1317/TEU, which increased by 14.1%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$2328/TEU, which spiked 11.8% from previous week.

North America:

On May 23rd, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$3275/FEU and US$4284/FEU, reporting 6% and 5.3% growth accordingly.

The Persian Gulf and the Red Sea:

On May 23rd, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf gain 16.5% to US$1387/TEU.

Australia&New Zealand:

On May 23rd, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand lost 2% to US$722/TEU.

South America:

On May 23rd, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports rose 12.1% to US$1934/TEU.