Stainless Insights in China from June 16th to June 20th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,005 | -17 | -0.89% |

| Foshan | 2,050 | -17 | -0.87% | ||

| Hongwang | Wuxi | 1,905 | -18 | -1.01% | |

| Foshan | 1,920 | -20 | -1.08% | ||

| 304/NO.1 | ESS | Wuxi | 1,825 | -30 | -1.70% |

| Foshan | 1,840 | -25 | -1.45% | ||

| 316L/2B | TISCO | Wuxi | 3,505 | -14 | -0.42% |

| Foshan | 3,560 | -25 | -0.73% | ||

| 316L/NO.1 | ESS | Wuxi | 3,375 | -17 | -0.52% |

| Foshan | 3,390 | -11 | -0.34% | ||

| 201J1/2B | Hongwang | Wuxi | 1,185 | -20 | -1.81% |

| Foshan | 1,180 | -17 | -1.56% | ||

| J5/2B | Hongwang | Wuxi | 1,075 | -14 | -1.44% |

| Foshan | 1,080 | -17 | -1.71% | ||

| 430/2B | TISCO | Wuxi | 1,145 | -4 | -0.41% |

| Foshan | 1,130 | -1 | -0.14% |

TREND || 201 Spot Prices Hit Five-Year Low

Last week, stainless steel spot prices in the Wuxi market saw a slight decline. Tsingshan’s price control measures loosened, prompting agents to follow suit with price cuts to reduce inventory. On the cost side, raw material prices fell, leading to weaker cost support. Deliveries to the market became more mixed. Although 300-series inventory decreased slightly, overall stock levels continued to rise, with high inventory levels limiting any price rebound. As of Friday, the main stainless steel futures contract price fell by US$6.3/MT from previous week to US$1880/MT, with a weekly low of US$1870/MT. In the spot market, end-user demand remained sluggish, and stainless steel spot prices dropped by US$14-US$28/MT last week.

300 Series: Macro Headwinds, Weak Supply and Demand Recovery

304 prices edged down last week. By Friday, the mainstream base price for 304 private cold-rolled (four-foot) in Wuxi was quoted at US$1855/MT, down US$21/MT from previous Friday; private hot-rolled was at US$1815/MT, down US$35/MT week-on-week. Overseas political uncertainty, especially escalating tensions between Israel and Iran, drove a surge in chemical-related commodities, leading to a rebound in the non-ferrous sector.

At the start of the week, Tsingshan again lowered its opening price, cutting cold and hot-rolled prices by US$14/MT for incoming orders. Spot traders quickly followed Tsingshan's price cuts to reduce inventory. Delong increased discounts to seize market share. While pre-locked pricing resources sold well, intra-day transactions were weak. Inventory rose for a fourth consecutive week, and high inventory levels continued to cap price rebound potential.

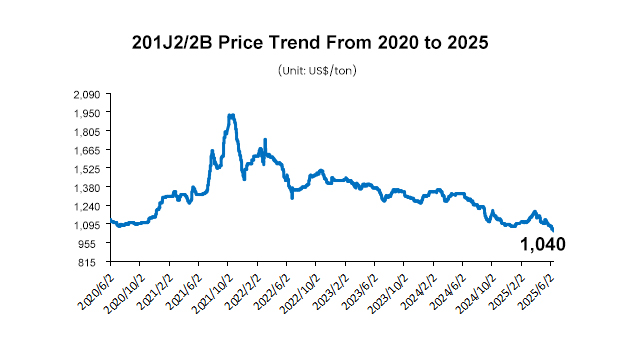

200 Series: 201 Spot Prices Reach Five-Year Low

Prices for 201 continued to weaken last week. 201J2 cold-rolled was quoted at US$1040/MT down US$14/MT week-on-week; 201J1 cold-rolled at US$1140/MT, down US$28/MT; and 201J1 hot-rolled at US$1140/MT, down US$14/MT. Currently, 201 prices have fallen to their lowest point in nearly five years.

The futures market fluctuated throughout the week. Early in the week, 201J2 cold-rolled quotes by traders centered around US$1055/MT base, with bulk deals discounted to US$1055/MT, but overall transaction volumes remained low. In the second half of the week, Tsingshan lowered its prices again, and traders slashed prices in exchange for volume. The lowest transaction price for J2 cold-rolled dropped to US$1035/MT.

400 Series: Increased Supply, Slight Price Drop

Prices for 430 remained weak last week. As of Friday, Wuxi’s spot market price for state-owned 430 cold-rolled dropped to around US$1145/MT, down US$7/MT from previous weekend. The state-owned 430 hot-rolled price remained stable at US$1055/MT, remained unchanged.

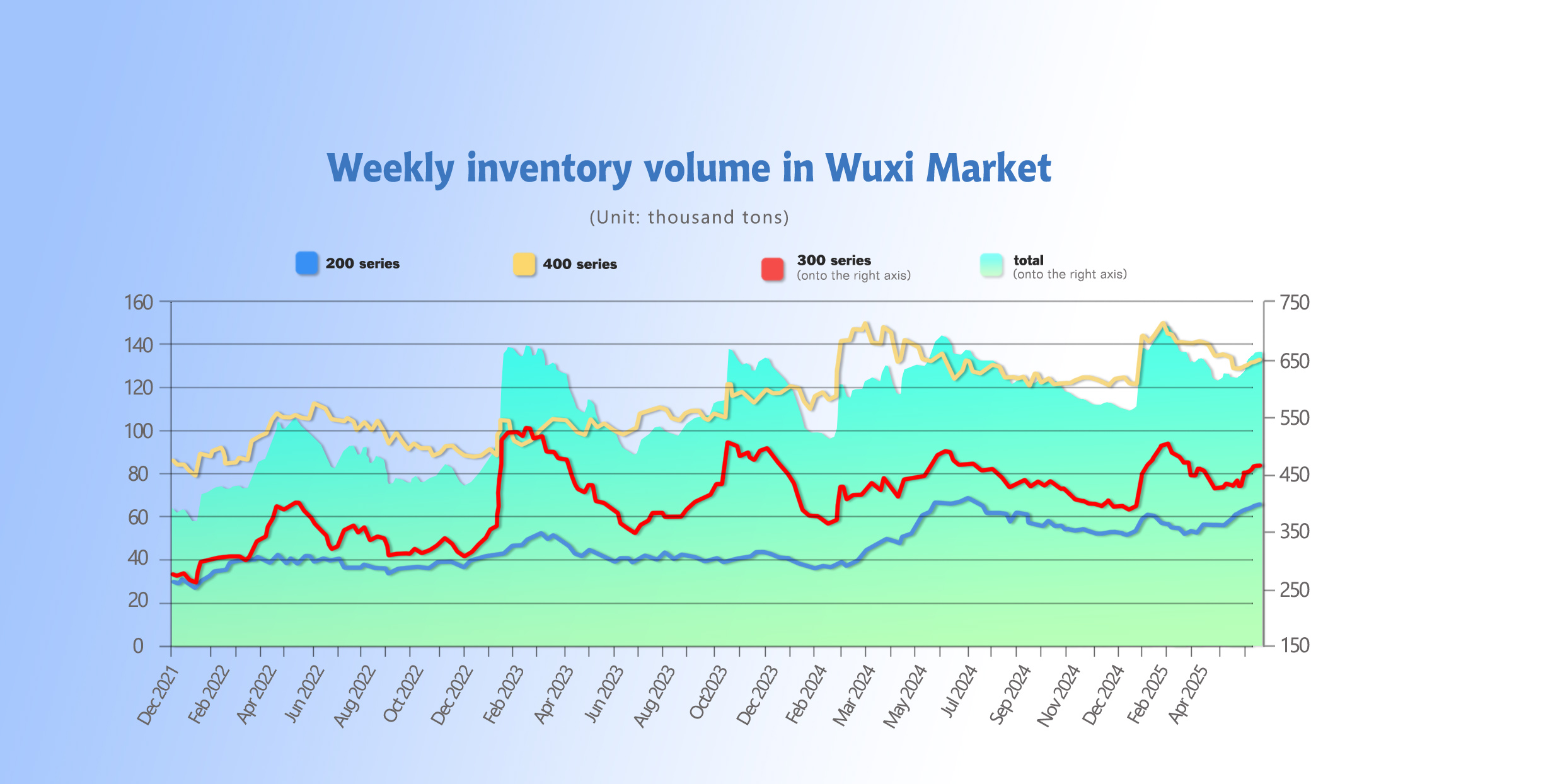

INVENTORY || Weekly Inventory Increases for Four Consecutive Years, Oversupply Situation Remains Hard to Reverse

As of June 19th, total inventory in Wuxi sample warehouses increased by 984 tons to 661,058 tons. Breakdown:

200 Series: 357 tons up to 65,125 tons.

300 Series: 487 tons down to 462,871 tons.

400 Series: 1,114 tons up to 133,062 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Jun 12th | 64,768 | 463,358 | 131,948 | 660,074 |

| Jun 19th | 65,125 | 462,871 | 133,062 | 661,058 |

| Difference | 357 | -487 | 1,114 | 984 |

300 Series: Tsingshan Cuts Prices Again, Agents Offer Discounts to Clear Inventory

At the beginning of last week, Tsingshan again lowered its cold and hot-rolled prices by US$14/MT for outbound sales, resulting in a surge of low-priced resources in the market. Other agents followed with price reductions, expanding transaction discounts. Combined with signs of stabilization in the futures market, downstream buyers entered the market for bargain purchases, speculative demand picked up, and inventory depletion accelerated.

200 Series: Incoming Supply Increases, Pressure Remains High

On the consumption side, buyers remained cautious while supply remained high. With seasonal demand in a downturn, inventory is expected to keep increasing next week. Continued attention should be paid to actual transaction activity.

As of June 19, due to persistently weak stainless steel prices — with 201 cold-rolled hitting a five-year low — a major East China mill plans to shut down one tandem rolling line for maintenance. The outage is expected to last about one week, impacting roughly 20,000 tons of cold-rolled production, mainly 201 products.

Since May, Tsingshan has repeatedly cut both cold- and hot-rolled 201 prices, and spot prices have remained weak. However, with high raw material costs, losses at steel mills have widened. As a result, many mills have begun to implement production cuts or shutdown plans throughout June. Crude steel production and scheduled output of the 200 series have both declined for two consecutive months.

400 Series: Weak Supply-Demand Pattern Persists, Inventory Continues Rising

The primary driver of this accumulation is the continued arrival of mill-supplied goods, while downstream procurement demand remains weaker than expected.

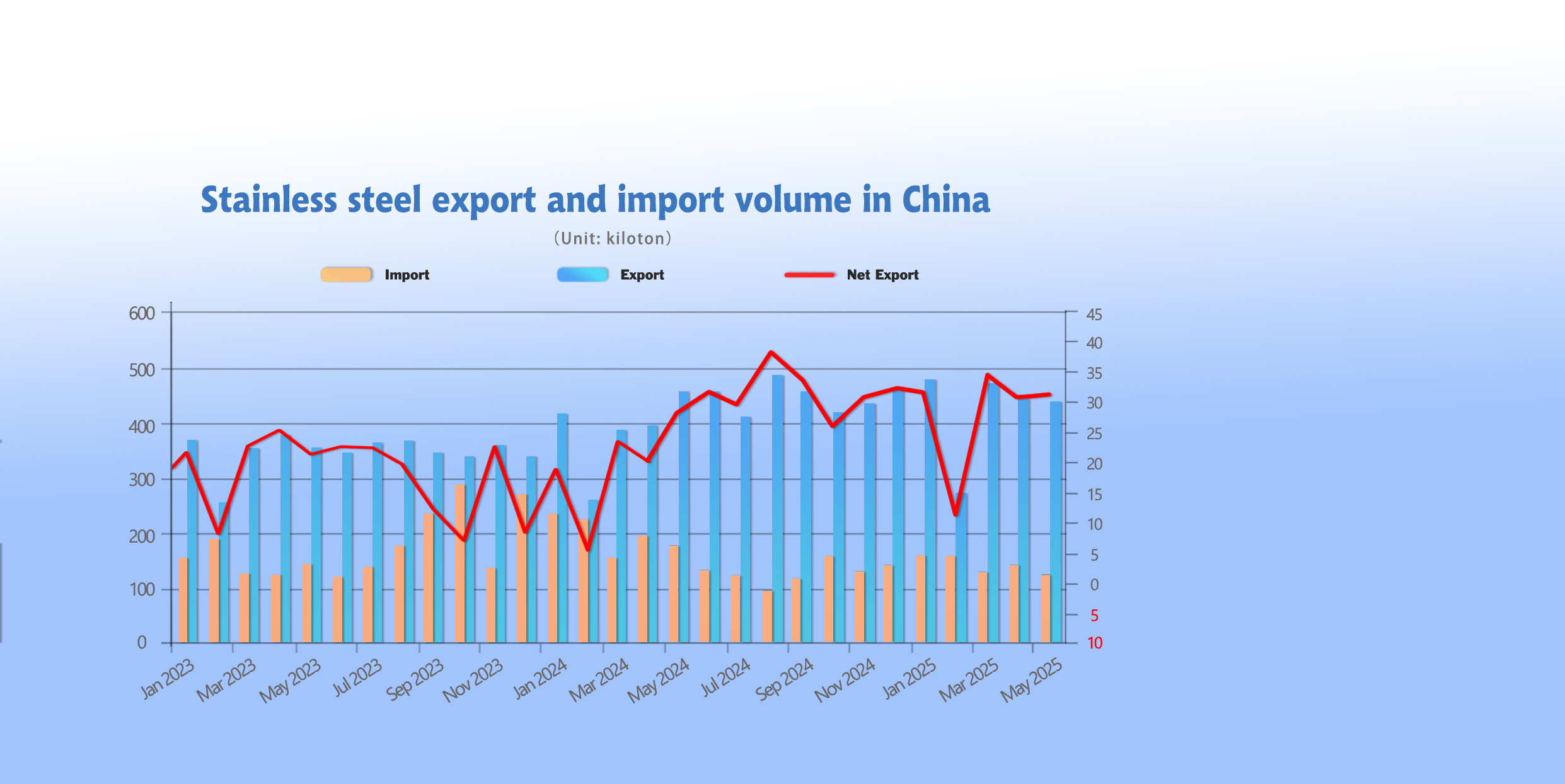

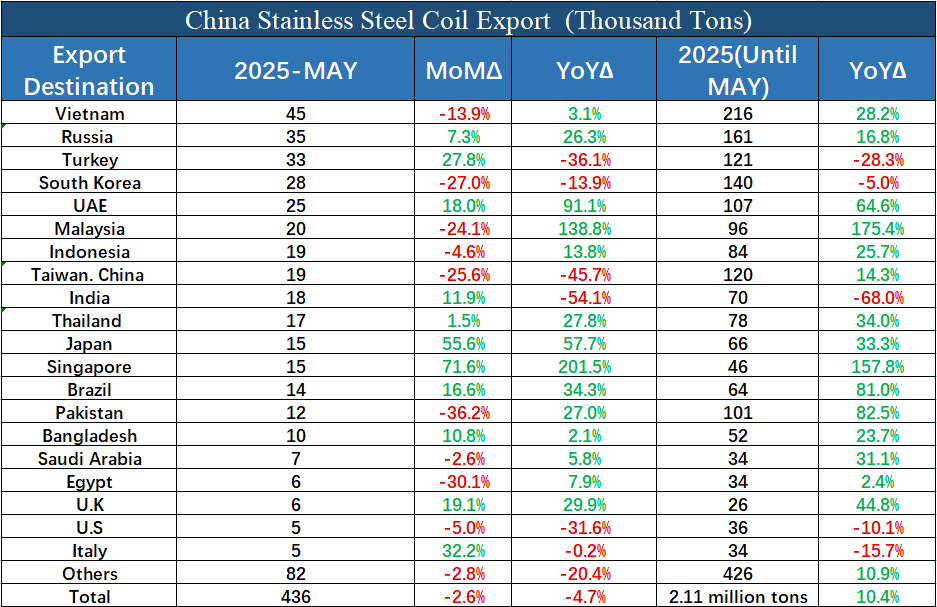

China's Stainless Steel Imports and Exports Both Declined in May

In May 2025, China imported 125,100 tons of stainless steel, down 12.00% month-on-month and 28.28% year-on-year. From January to May, total imports were 718,000 tons, down 26.47% compared to the same period last year.

Exports of stainless steel in May stood at 436,300 tons, a decrease of 2.56% month-on-month and 4.66% year-on-year. From January to May, cumulative exports reached 2.11 million tons, representing a 10.36% increase over the same period last year.

Net exports in May were 311,300 tons, up 1.82% month-on-month and 9.88% year-on-year. Cumulatively from January to May, net exports totaled 1.3921 million tons, an increase of 48.81% compared to the same period last year.

Since November 2024, when Vietnam lifted anti-dumping duties on Chinese cold-rolled stainless steel, China’s exports to Vietnam have risen significantly, making it the top export destination for Chinese stainless steel.

Meanwhile, Indonesia’s Yongwang Steel suspended production in mid-to-late May for maintenance, a shutdown expected to last until August. This will reduce cold-rolled stainless steel supply by more than 150,000 tons, with 304 cold-rolled being the most affected. Between May and June, around 50,000 tons of Indonesian cold-rolled stainless steel are expected to be re-imported into China, after which import volumes may decline significantly.

RAW MATERIALS || Stainless Steel Prices Remain Weak, Ferro-nickel Under Pressure

Last week, high-grade ferro-nickel ex-works prices continued to decline. As of Thursday, prices were quoted at US$131/nickel point, down US$2.1/MT from last Thursday. SHFE nickel futures remained weak; by Thursday’s close, the main contract settled at US$16,721/MT, down US$156/MT, a 0.93% decrease from previous week.

Recently, ferro-nickel prices have been persistently declining, hitting a new low for the year. On the supply side, nickel ore prices remain firm, leading to intensified losses for domestic ferro-nickel producers and keeping output at low levels. The premium on Indonesian nickel ore remains elevated, providing strong cost support. Some local plants in Indonesia have already started reducing production due to mounting losses.

On the demand side, stainless steel prices continue to perform weakly, resulting in negative margins for steel mills. Some mills have started production cuts. It is understood that a leading steel producer plans to reduce both long-term contracts and spot purchases of ferro-nickel in July. The ferro-nickel market is now experiencing oversupply, and prices are expected to remain under pressure in the short term.

SUMMARY || Stainless Steel Demand and Prices Remain Weak

Stainless steel prices declined again last week. On the demand side, purchasing remains mainly demand-driven. Although steel mill output has slightly declined, it still remains at a high level, making it difficult to reverse the oversupply situation. Social inventories are being digested slowly, and spot availability remains ample. Market focus should remain on downstream demand recovery, mill production schedules, and inventory drawdowns. The outlook is for continued weak and volatile performance in stainless steel prices.

300 Series: Steel mill production has slightly declined, easing market supply pressure somewhat. However, demand remains sluggish, with purchases primarily meeting just immediate needs due to seasonal weakness. Tsingshan has repeatedly reduced prices to stimulate sales, prompting agents to lower their offers as well. However, the issue of high inventory levels remains unresolved, with stocks continuing to build up, limiting the potential for any significant price rebound.

On the macro side, domestic sentiment remains cautiously optimistic, while strong overseas economic data and delayed Fed rate cut expectations have intensified global market volatility. Under weak supply-demand conditions, both cold and hot-rolled 304 spot prices continue to follow a weak and fluctuating trend.

200 Series: Despite high raw material costs, many steel mills have begun suspending or scaling back production. Output of 200-series crude steel has declined in June. However, downstream demand remains lackluster, and low-priced resources have continued to appear in the market. Inventory has been rising steadily since May. In the short term, attention should be paid to mill price policies and transaction performance. In a dual-weak supply-demand environment, 201 prices are expected to remain weak but stable.

400 Series: Last week, high-chrome raw material retail prices remained weak but stable, offering some cost support for 400-series stainless steel. However, downstream demand in the 400-series spot market showed no significant improvement, and inventory continued to build. Price support is weak, and 430 prices are expected to maintain a slightly weak and stable trend next week.

MACRO || Trade Barriers Further Suppress Demand

On June 19, the Canadian government issued a statement announcing that it will adjust its existing countermeasures on steel and aluminum tariffs starting July 21, aligning them with the progress made by the United States in broader trade arrangements.

At the same time, Canada introduced several measures to protect its domestic steel and aluminum industries. For instance, starting June 30, Canadian federal projects will only be permitted to use steel and aluminum from Canadian suppliers or from “trusted trading partners” — those with reciprocal market access under trade agreements with Canada.

Additionally, the Canadian government will establish a working group to monitor market developments under the new tariff regime.

On the same day, Canada also announced new tariff quotas for steel imports from non-free trade agreement partners, capping them at 100% of 2024 levels. Finance Minister Chrystia Freeland stated that this move aims to protect Canada’s steel industry, stabilize the domestic market, and prevent harmful trade diversion caused by destabilizing actions from the U.S.

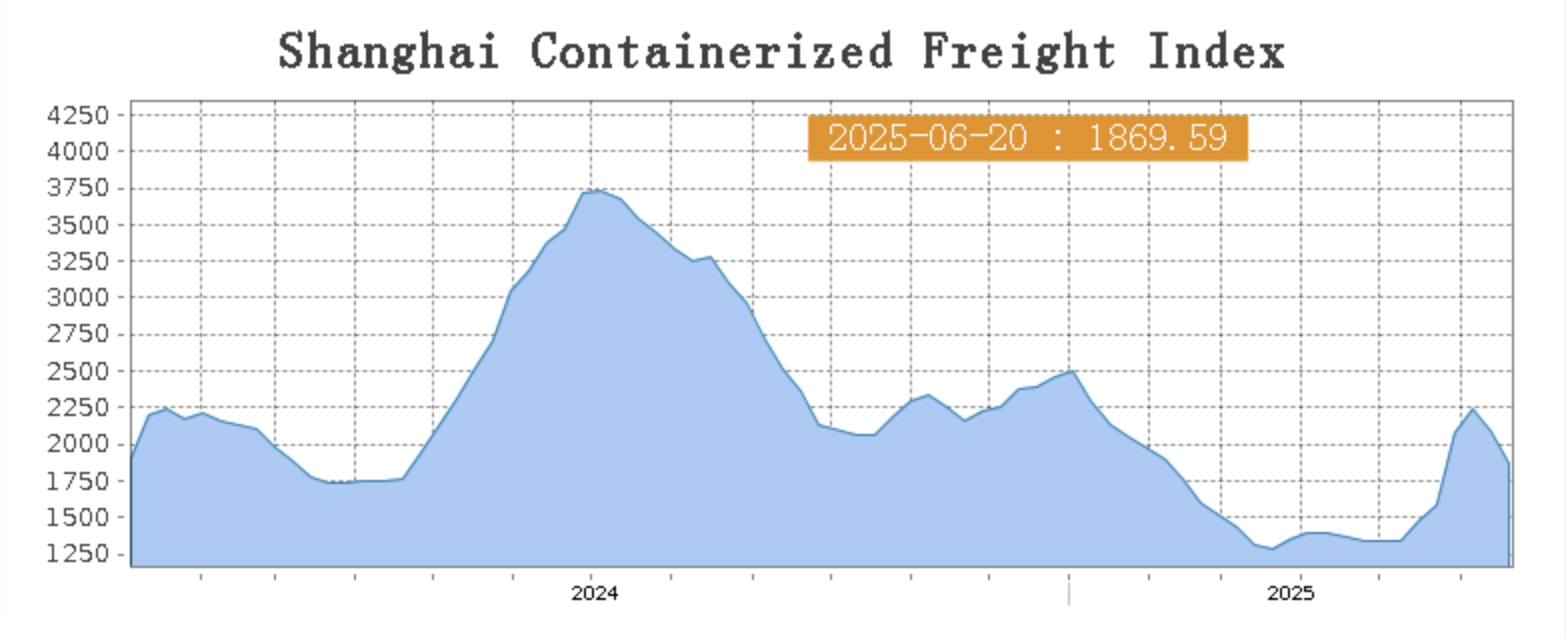

SEA FREIGHT || North America Rates Collapse 32.7%; South America Rates Surge 15.6%

As the Iran-Israel conflict escalates, the cost of maritime transport from the Middle East has soared in recent days. Not only have tanker freight rates for oil shipments jumped, but insurance premiums for vessels navigating the Red Sea and Persian Gulf have also spiked — reflecting the sharply increased shipping risks in the region.

The continued escalation of the Iran-Israel conflict has caused turbulence in global shipping markets. According to the Baltic Dirty Tanker Index, average international freight rates rose 12% over the past week. Some high-risk routes, such as Persian Gulf to Europe and Asia to Europe via the Red Sea, have seen freight rates surge by up to 2.5 times. Daily charter rates for VLCCs (Very Large Crude Carriers) soared from around $20,000 to $55,000 within a week.

Last week, China's containerized export shipping market continued to undergo adjustments. Rates varied across different trade lanes, but overall, declines outnumbered gains, leading to a drop in the composite index.

The buying frenzy driven by anticipated tariff hikes has largely subsided.

On June 20th, the Shanghai Containerized Freight Index (SCFI) fell 10.5% to 1869.59 points.

Europe/ Mediterranean:

On June 20th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1835/TEU, which decreased by 0.5%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$3063/TEU, which dip 4.0% from previous week.

North America:

Last week, shipping demand remained generally stable. However, as transport capacity increased, the supply-demand balance weakened, leading to sharp rate declines in many routes.

On June 20th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$2772/FEU and US$5352/FEU, reporting 32.7% and 20.7% slide accordingly.

The Persian Gulf and the Red Sea:

On June 20th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf grew 1.9% to US$2122/TEU.

Australia & New Zealand:

On June 20th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand gained 2.4% to US$763/TEU.

South America:

On June 20th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports surged 15.6% to US$5459/TEU.