Stainless Insights in China from July 7th to July 13th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 1,990 | 0 | 0.00% |

| Foshan | 2,035 | 0 | 0.00% | ||

| Hongwang | Wuxi | 1,900 | 4 | 0.24% | |

| Foshan | 1,905 | 3 | 0.16% | ||

| 304/NO.1 | ESS | Wuxi | 1,815 | 4 | 0.25% |

| Foshan | 1,830 | 3 | 0.16% | ||

| 316L/2B | TISCO | Wuxi | 3,495 | 39 | 1.18% |

| Foshan | 3,560 | 34 | 0.99% | ||

| 316L/NO.1 | ESS | Wuxi | 3,350 | 39 | 1.24% |

| Foshan | 3,375 | 34 | 1.05% | ||

| 201J1/2B | Hongwang | Wuxi | 1,170 | -14 | -1.32% |

| Foshan | 1,170 | -4 | -0.40% | ||

| J5/2B | Hongwang | Wuxi | 1,055 | -13 | -1.32% |

| Foshan | 1,070 | -3 | -0.29% | ||

| 430/2B | TISCO | Wuxi | 1,120 | -1 | -0.14% |

| Foshan | 1,110 | -6 | -0.56% |

TREND || Government Advocates Capacity Optimization, Supply and Demand Gradually Recover

Last week, spot prices in the Wuxi stainless steel market saw a mild rebound in line with futures. Costs trended downward due to falling raw material prices. However, production cuts by steel mills remained limited, deliveries to the market continued, and inventories increased. Anti-price-war ("anti-involution") policies continued to gain momentum, keeping sentiment strong in the bulk commodity market, while downstream demand remained focused on essential procurement.

As of Friday, the price of the stainless steel main futures contract fell by US$2.8/MT week-on-week to US$1905/MT.

300 Series: Ongoing Arrivals Lead to Inventory Rebound After Previous Drawdown

Last week, 304 prices rose slightly. By Friday, the mainstream base price for four-foot 304 private cold-rolled in Wuxi was US$1865/MT, up US$7/MT from last week. Private hot-rolled was priced at US$1820/MT, an increase of US$14/MT.

At the beginning of the week, Tsingshan lowered its price cap, prompting market agents to follow suit, resulting in an influx of low-priced resources. However, strong wait-and-see sentiment from downstream buyers led to sluggish inventory reduction. With new U.S. tariffs on Chinese goods taking effect August 1 and potential additional tariffs from BRICS countries, export uncertainty is on the rise.

Domestically, policies targeting low-price competition ("anti-involution") are intensifying, boosting sentiment in the commodities market. Stainless steel futures prices fluctuated upward last week, and some agents cautiously raised prices to sell. Still, high-priced resources were slow to move. June production cuts by steel mills fell short of expectations, leaving ample spot supply in the market. Weak demand led to renewed inventory accumulation.

200 Series: Spot Prices Return to Lows

Prices for 201 continued to decline last week:

201J2 cold-rolled: US$1025/MT, down US$7/MT

201J1 cold-rolled: US$1140/MT, down US$14/MT

201J1 hot-rolled: US$1120/MT, down US$14/MT

Early in the week, futures prices edged down, and 201J2 cold-rolled hit a low of US$1025/MT, driving a pessimistic market sentiment. As macro sentiment improved midweek, futures rebounded and traders firmed up their offers. Downstream buyers prioritized lower-priced options, leading to slight inventory accumulation in both cold-rolled and hot-rolled products.

By Friday afternoon, low-end 201 prices rose by US$7-US$14/MT, and overall transaction activity improved.

400 Series: Prices Remain Stable

The 430 market remained stable last week:

In the Wuxi spot market, state-owned 430 cold-rolled was quoted at US$1125/MT, unchanged from last week.

State-owned 430 hot-rolled held steady at US$1040/MT, also flat week-on-week.

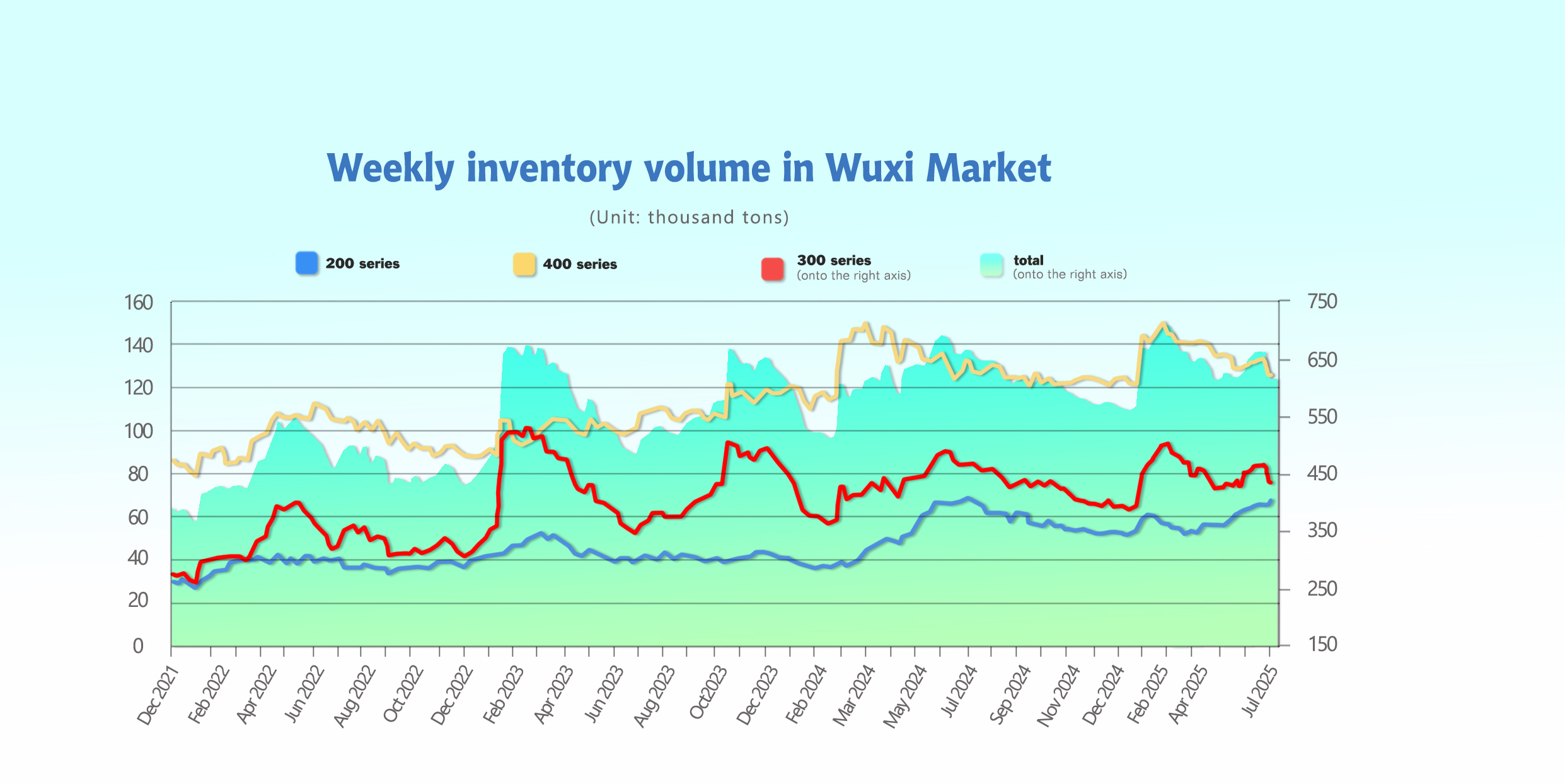

INVENTORY || The weekly inventory increased by 7,000 tons

As of July 10th, total inventory in Wuxi sample warehouses increased by 6,705 tons to 631,699 tons. Breakdown:

200 Series: 3,100 tons up to 68,560 tons.

300 Series: 2,463 tons up to 436,814 tons.

400 Series: 1,142 tons up to 126,325 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

|

Jul 3rd |

65,460 | 434,351 | 125,183 | 624,994 |

| Jul 10th | 68,560 | 436,814 | 126,325 | 631,699 |

| Difference | 3,100 | 2,463 | 1,142 | 6,705 |

300 Series: Production Cuts Fall Short of Expectations, Demand Remains Weak

Futures prices fluctuated upward during the week, prompting agents to slightly raise prices while reducing inventory. However, spot prices remain constrained by weak fundamentals.

June 300 series output totaled 1.8418 million tons, a month-on-month decrease of only 8,000 tons, indicating that steel mills' production cuts were less than expected, and supply pressure persists in the market.

On the demand side, conditions remain weak. Downstream buyers continue to purchase only on a just-in-time basis, and agents maintain low inventory operations. Overall, supply and demand dynamics remain soft.

With tepid market consumption, inventories have seen a mild increase.

While macro sentiment has warmed slightly, overseas policy remains weak, and interest rate cut expectations have once again been delayed, suppressing commodity prices.

Next week, inventories may begin to decline slightly, but attention should remain focused on steel mill production levels and market consumption trends.

200 Series: Increased Arrivals Lead to Slight Inventory Build-Up

Looking at inventory composition, steel mills such as Beigang Xincai continued to deliver shipments, increasing the volume of market-available resources.

Both cold-rolled and hot-rolled 201 prices declined this week, and traders made price concessions in actual transactions. In the short term, prices are likely to remain weak and range-bound, and inventories may continue to accumulate next week.

400 Series: Raw Material Prices Slip Slightly, Cost Support Weakens

Market activity declined compared to last week, and downstream procurement volume was limited.

Mainstream steel mill deliveries were relatively few, slightly easing supply pressure, and prices remained stable.

As of now, cost support remains relatively firm, but 400 series spot inventory is still at a high level, limiting upward price momentum.

RAW MATERIAL || Nickel Iron Purchase Prices Hit New Lows

Last week, high-grade ferronickel ex-factory prices continued to weaken, falling to US$127.9/nickel point by Friday, down US$1.4/nickel point from last Friday.

During the week, Tsingshan purchased tens of thousands of tons of high-nickel iron at US$126.6/nickel point, prompting mainstream domestic steel mills to further lower procurement prices, hitting the lowest point in nearly a year and a half.

Currently, the domestic base price for Indonesian nickel ore has slightly declined, pushing down the production cost center of Indonesian ferronickel. However, some plants continue to operate at a loss and maintain reduced production.

With stainless steel prices strengthening and profit margins recovering, the pressure from steel mills has eased. In the short term, nickel iron prices are expected to remain stable.

In June, total output of high-nickel iron from major domestic ferronickel producers and integrated steel mills was approximately 186,200 tons, down 7,100 tons from May’s 193,300 tons.

Of this, self-produced high-nickel iron by steel mills accounted for 135,500 tons, a decrease of 6,300 tons month-on-month; production by independent plants was about 50,700 tons, down 800 tons.

June saw a slight reduction in domestic ferronickel output, mainly from integrated steel mills.

Due to stubbornly high prices of Philippine nickel ore, self-produced nickel iron became less economical compared to purchasing externally, resulting in significant production cuts by mills.

Meanwhile, nickel iron prices continued to drop in June, while ore prices remained firm, worsening losses at domestic ferronickel plants. These plants maintained low production loads, and July production is expected to remain at low levels.

SUMMARY || Stronger Futures Lift Sentiment, But Seasonal Lull Caps Upside

At the end of June, planned production cuts by steel mills sparked a temporary rebound in both futures and spot stainless steel prices.

Entering early July, macro policies aimed at curbing low-price competition and promoting the orderly exit of outdated capacity (i.e., anti-involution measures) added positive momentum.

Futures prices extended gains, and market confidence in spot stainless steel improved notably, with prices rebounding as well.

However, underlying supply-demand imbalances persist, limiting the overall rally.

300 Series: Supply Pressure Remains as Output Cuts Fall Short

Steel mill production cuts were less than expected, so market supply pressure has not eased.

Demand remains sluggish; downstream buyers are only restocking as needed, and distributors are maintaining lean inventories.

Overall, supply and demand remain weak, consumption is average, and inventories continue to rise slightly.

On the macro front, sentiment is warming, but overseas policies remain weak. Rate-cut expectations have been postponed, intensifying the tug-of-war between bulls and bears.

Market sentiment is currently strong, and 304 cold and hot-rolled spot prices are expected to move with a slightly bullish bias alongside futures.

200 Series: July Production Plans Cut Again, Supply Pressure to Ease

Steel mills are expected to reduce production again in July, which may alleviate supply pressure in the following period.

However, downstream sentiment remains cautious, demand is weak, and inventories are back in accumulation.

Short-term prices for 201J2 are expected to fluctuate within a narrow range, and attention should be paid to subsequent production plans and futures price movements.

400 Series: Raw Material Prices Stable, Prices Under Pressure

Last week, retail prices of high-chromium raw materials remained steady, continuing to support the cost base of 400 series stainless steel.

Downstream demand for 400 series slowed last week. While steel mill arrivals were limited, inventory held by traders increased significantly, indicating rising supply pressure.

With upward momentum lacking, 430 prices are expected to remain stable next week.

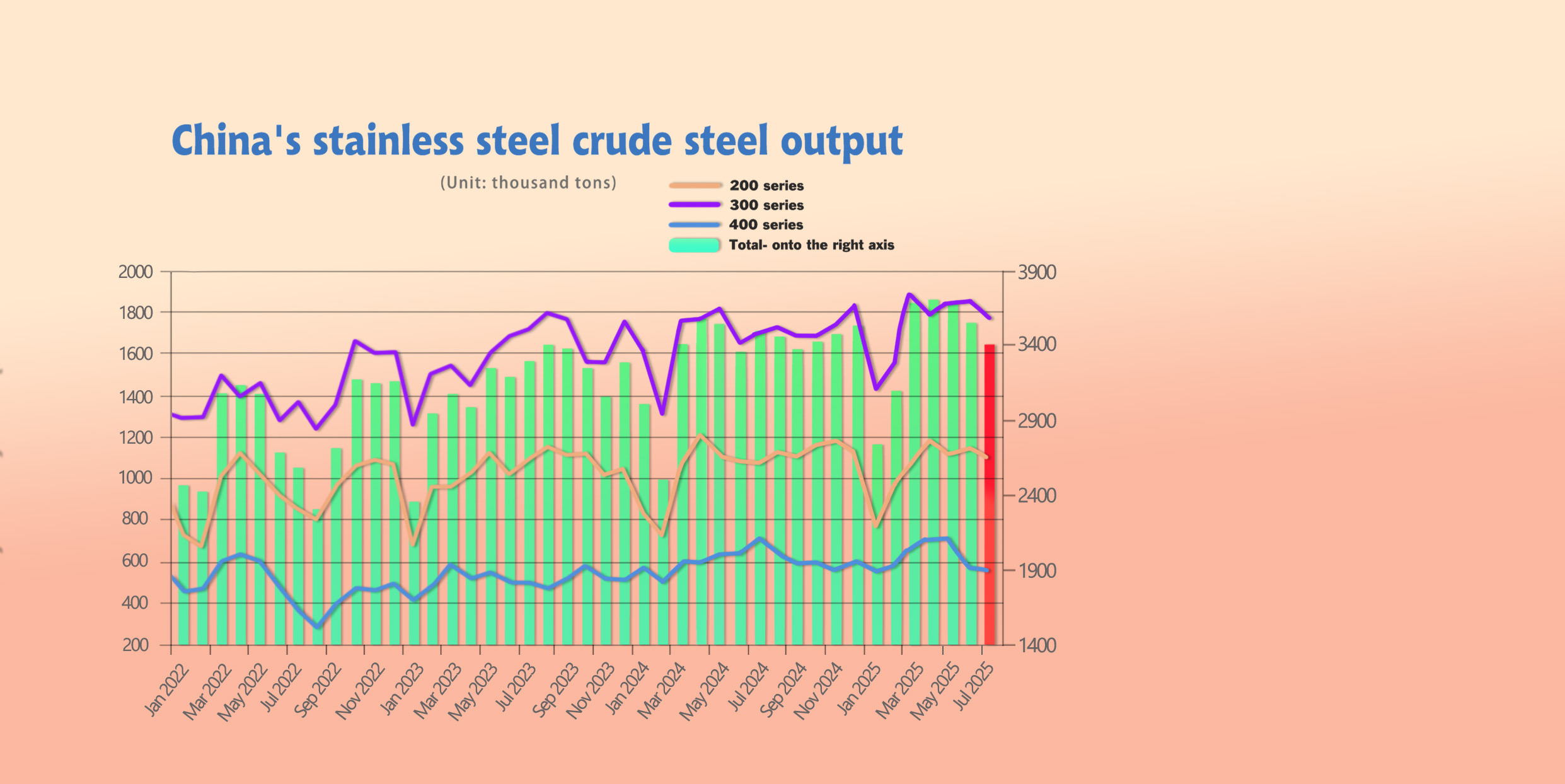

MACRO || July Output Scheduled to Drop by 112,700 Tons to 3.41 Million Tons

According to statistics, in June 2025, China's large-scale stainless steel enterprises produced approximately 3.5592 million tons of crude stainless steel, down 112,700 tons from May (a 3.05% decrease month-on-month), but up 195,900 tons year-on-year, marking a 5.53% increase.

Production by series in June showed mixed trends:

200 Series: 1.1465 million tons, up 35,800 tons MoM (+3.01%), and up 70,200 tons YoY (+6.34%)

300 Series: 1.8418 million tons, down 8,000 tons MoM (–0.45%), and up 194,900 tons YoY (+10.76%)

400 Series: 570,900 tons, down 140,500 tons MoM (–19.71%), and down 69,200 tons YoY (–11.05%)

In June, the three major steel mills aligned prices for 201J2-series spot products in the 200 series. Improved sentiment and modest price hikes spurred better transaction volumes. Mill profitability recovered, and Baosteel resumed production, leading to a notable increase of about 36,000 tons in 200 series output, up 3.01% month-on-month.

For the 400 series, prices declined slightly, mill margins were squeezed, and HuaSteel cut back production significantly, bringing overall 400 series output down to around 570,000 tons.

Short-term demand remains weak, and market supply pressure persists.

Preliminary estimates indicate that July’s crude stainless steel output is expected to fall by 112,700 tons MoM to approximately 3.41 million tons, broken down as follows:

300 Series: Down 80,000 tons to 1.762 million tons

200 Series: Down 45,000 tons to 1.10 million tons

400 Series: Down 27,000 tons to 544,000 tons

In summary, crude steel output in June declined month-on-month.

The 300 and 400 series saw eased supply pressure, while available resources in the 200 series increased.

Stainless steel prices, however, remain at low levels, and downstream buyers continue to purchase mainly on a just-in-time basis. Future trends in mill output and transaction volume remain key to watch.

First-Half 2025 Crude Stainless Steel Output Reaches 20.47 Million Tons

From January to June 2025, China’s large-scale stainless steel enterprises produced a total of 20.47 million tons of crude stainless steel, an increase of 1.04 million tons year-on-year (+5.36%).

All product series saw year-on-year growth:

200 Series: 6.30 million tons, up 284,000 tons (+4.72%)

300 Series: 10.37 million tons, up 481,000 tons (+4.86%)

400 Series: 3.79 million tons, up 276,000 tons (+7.85%)

Growth was also recorded across product forms:

Wide-width coil: 14.87 million tons, up 650,000 tons (+4.57%)

Narrow strip: 2.81 million tons, up 129,000 tons (+4.8%)

Long products: 2.78 million tons, up 261,000 tons (+10.38%)

At the beginning of the year, output was low in January–February due to the Spring Festival holiday and weak downstream demand, with many mills initiating maintenance shutdowns.

As demand gradually picked up post-holiday and raw material prices rose — providing stronger cost support for stainless steel — both spot and futures prices climbed. Mills’ profits improved, pushing April production to the highest level of H1, reaching around 3.7 million tons.

In the following months, however, continued U.S.-China tariff tensions led to obstacles in downstream exports, weakening market demand.

Stainless steel prices declined, mill profit margins shrank, and production volumes fell month by month in May and June.

July output is projected to edge down further to around 3.42 million tons.

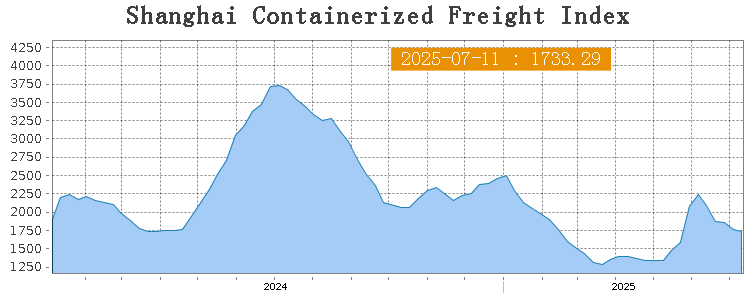

SEA FREIGHT || Overall Stability in the Shipping Market, Mixed Performance on Long-Haul Routes

Last week, China's export container shipping market remained generally stable. Due to differences in supply-demand fundamentals across routes, freight rates experienced mixed movements, and the composite index declined slightly.

On July 11th, the Shanghai Containerized Freight Index (SCFI) fell 1.7% to 1733.29 points.

Europe/ Mediterranean:

The tariff negotiations between Europe and the U.S. still have no clear outcome as the original tariff suspension deadline passed, leaving market prospects uncertain. Transport demand remained stable last week, and freight rates operated steadily.

On July 11th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$2099/TEU, which decreased by 0.1%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$2667/TEU, which dip 7% from previous week.

North America:

The ongoing volatility in tariff policies is expected to continue having a significant impact on the container shipping market. Last week, overall transport demand remained stable, and after continuous adjustments, freight rates showed a rebound.

On July 11th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$2194/FEU and US$4172/FEU, reporting 5% and 1.2% growth accordingly.

The Persian Gulf and the Red Sea:

On July 11th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf shrank 16.1% to US$16.1/TEU.

Australia & New Zealand:

On July 11th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand gained 19.7% to US$1021/TEU.

South America:

On July 11th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports decreased 2.4% to US$6221/TEU.