Stainless Insights in China from May 26th to May 30th.

TREND || Retail Prices Weaken, Setting the Stage for a Downturn in June

Major steel mills have successively announced their high-carbon ferrochrome procurement prices for June, generally maintaining a flat trend compared to the previous month. Details are as follows:

Tsingshan Group: The long-term contract purchase price for high-carbon ferrochrome in June 2025 is set at US$1138/50 reference ton (cash, tax-included, delivered to plant), unchanged from the previous month. The receiving price at Tianjin Port is US$21 lower per 50 base tons.

TISCO : The tender purchase price for high-carbon ferrochrome in June 2025 is finalized at US$1110/50 reference ton (cash, tax-included, delivered to plant), unchanged from May.

Beigang New Materials: The long-term contract purchase price for June is also US$1138/50 reference ton (cash, tax-included, delivered to plant), flat month-on-month, with the Tianjin Port receiving price also US$21/50 reference tons.

As a result, mainstream ex-factory quotations for high-carbon ferrochrome have been running weakly in recent days, generally ranging between US$1125-US$1153/50 reference ton, slightly above the mainstream steel mill purchase prices.

According to market sources, retail quotations in northern major production regions have dropped below US$1125, with some offers as low as US$1111/50 reference ton. Industry insiders expect that with rising high-chrome output and slightly weakening downstream demand, price support will gradually erode, and there remains downside risk for high-carbon ferrochrome prices in June.

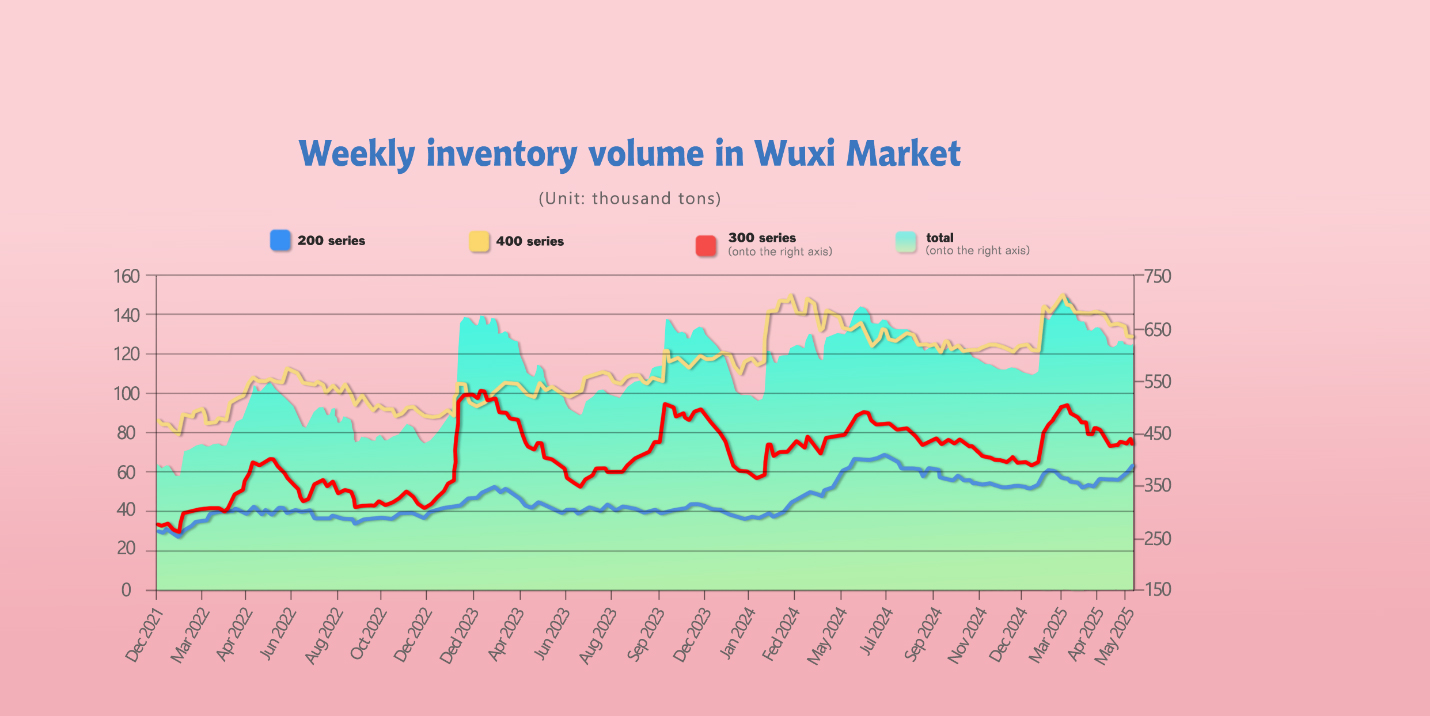

INVENTORY || Up 2.55%! With Supply Pressure Unrelieved, Where Will Prices Go Amid Weak Seasonal Demand?

As of May 29th, total inventory in Wuxi sample warehouses increased by 15,600 tons to 626,661 tons. Breakdown:

200 Series: 2,874 tons up to 62,583tons.

300 Series: 11,746 tons up to 435,868 tons.

400 Series: 980 tons up to 128,210 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| May 22nd | 59,709 | 424,122 | 127,230 | 611,061 |

| May 29th | 62,583 | 435,868 | 128,210 | 626,661 |

| Difference | 2,874 | 11,746 | 980 | 15,600 |

200 Series: Increased Resource Inflows, Price Cuts Yield No Gains

According to the spot inventory structure, last week saw continued inflows of resources from Baosteel Desheng, Zhongshan Hongwang, and others, resulting in ample circulating supply in the market. Prices for 201 cold-rolled products continued to weaken, with J2 cold-rolled transaction prices falling as low as US$970/MT, and downstream purchasing sentiment remained poor, leading to continued inventory buildup. 201 hot-rolled prices saw slight downward adjustments, with more low-priced resources available in the market, and transactions mostly driven by rigid demand.

As the market nears the holiday period, sales promotions have become prevalent. Supply pressure remains high. Attention should be paid to steel mill production trends. The 200 series inventory is expected to continue accumulating next week.

300 Series: Supply Pressure Persists; Weak Supply-Demand Balance Leads to Further Inventory Accumulation

Looking at the spot inventory structure, there was a notable increase in hot-rolled arrivals at Jiangyin Port last week, with ample hot-rolled stock in circulation and supply pressure showing no signs of easing. With a slight rise in costs, some steel mills that were planning to switch production slowed operations, and arrivals remained steady. However, due to weak market conditions, cold-rolled inventory shifted from declining to increasing on a weekly basis.

Last week, futures and spot prices both fell in tandem. The off-season and the lack of macro policy drivers have made fundamentals more dominant in price setting. The weak supply-demand pattern showed no obvious improvement. Downstream purchasing remained focused on low-priced, rigid-demand buying, with little speculative interest, leading to a noticeable inventory buildup.

At present, macro sentiment is relatively weak, and the speculative environment in the market is limited. On the supply side, with production switching and reductions slowing, supply pressure is increasing. On the demand side, the seasonal downturn and ongoing price stagnation have led downstream buyers to continue purchasing only on a needs basis. The imbalance between supply and demand remains unresolved, causing inventories to increase.

Note: Taking warehouse warrant resources into account, the total 300 series cold-rolled inventory in Wuxi (social + warrant) was 304,000 tons last week, down by 3,400 tons (1.11%) from last week, and down by 68,100 tons (18.30%) compared with the same period last year.

400 Series: High Costs Provide Support, but Market De-stocking Slows

From the current spot inventory structure, JISCO’s cold-rolled inventory saw a slight decrease last week, while both cold- and hot-rolled inventories from TISCO increased significantly, leading to a slight overall inventory accumulation.

Steel mills replenished inventories, but downstream demand has slowed, resulting in moderate sales of 400 series cold-rolled stainless steel, with destocking happening at a sluggish pace. On the raw materials side, the retail price of high-carbon ferrochrome continued to show weak and steady trends last week. Although stainless steel production costs remain high, support has started to weaken slightly.

400 series stainless steel producers continue to face losses. Wuxi’s spot market is expected to continue slow destocking next week, with a slight drop in 400 series inventory.

Last week, 430 cold-rolled prices were relatively stable, but downstream demand softened, leading to a mild increase in inventory. With June’s high-chrome procurement prices unchanged month-on-month, cost support remains. Watch closely how changes in downstream demand for 400 series stainless steel will affect 430 prices.

MACRO || Trump Accuses China of Breach, Announces Tariff Hike on Steel and Aluminum

On May 30, former U.S. President Donald Trump held a rally at a U.S. Steel plant in the suburbs of Pittsburgh, Pennsylvania, where he accused China of violating a bilateral agreement and failing to lower tariffs as promised. During the event, he also announced that import tariffs on steel and aluminum would be raised from 25% to 50%.

Trump claimed that China and the U.S. had previously agreed to mutually lift trade restrictions on critical minerals and reduce tariffs, but China broke its commitment. He issued a stern warning, hinting at taking tougher actions against Beijing. On his social media platform Truth Social, he wrote:

“Perhaps unsurprisingly to some — China has completely violated the agreement it made with us. No more being Mr. Nice Guy!”

At a rally in Pennsylvania last Friday, Trump announced a "partnership" soon to be finalized between Japan’s Nippon Steel and U.S. Steel, and declared that steel import tariffs would be raised from 25% to 50% starting next week. He said the measure would “further safeguard the security of America’s steel industry.” Shortly after, he posted on Truth Social that aluminum tariffs would also be raised to 50% starting June 4.

Although China is the world’s largest steel producer and exporter, its steel has virtually disappeared from the U.S. market since the 25% tariff was imposed in 2018. However, China remains the third-largest supplier of aluminum to the United States.

During the same May 30 rally, Trump praised the “agreement” and partnership between Nippon Steel and U.S. Steel. Nippon Steel Vice Chairman Takahiro Mori joined Trump on stage in a show of support. Reports suggest that the U.S. side is moving toward final approval of Nippon Steel’s plan to acquire 100% of U.S. Steel, making it a wholly owned subsidiary. However, Trump did not explicitly state whether he would approve the acquisition — a diplomatically sensitive move — at the rally.

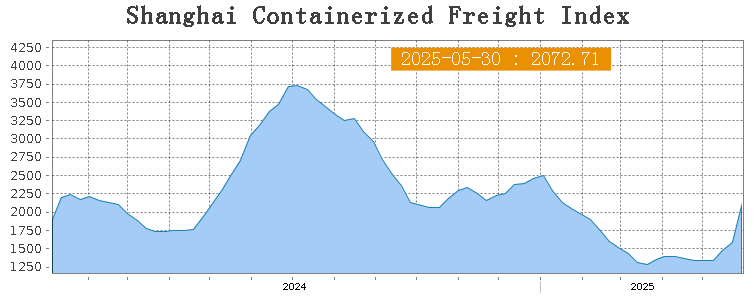

SEA FREIGHT || Market Remains Generally Stable with Slight Fluctuations on Some Routes

Last week, China’s container export shipping market continued its upward trend. Positive news surrounding the easing of the “tariff war” has continued to support the market, with freight rates on most major routes rising further, driving the composite index higher. On May 30th, the Shanghai Containerized Freight Index (SCFI) surge 30.7% to 2072.71 points.

Europe/ Mediterranean:

Europe is accelerating its tariff negotiations with the United States, but the outlook for those talks remains highly uncertain, putting the prospects for Europe's economic recovery to the test.

On May 30th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1587/TEU, which increased by 20.5%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$3061/TEU, which grew 31.5% from previous week.

North America:

Last week, shipping demand remained stable. With continued support from positive news, spot booking prices in the market increased. According to data released by the U.S. Department of Commerce, new orders for durable goods in April fell sharply by 6.3% month-on-month (preliminary data), with business equipment orders from U.S. factories seeing their biggest drop since October of last year. This suggests that uncertainty over tariffs and tax policies is dampening business investment appetite.

At the same time, the ongoing “rush to export” has helped keep transportation demand at a high level. Overall shipping capacity has basically returned to pre-trade war levels, but tight space availability remains an issue. Some ports are experiencing congestion, and market freight rates have risen sharply.

On May 30th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$5172/FEU and US$6243/FEU, reporting 57.9% and 45.7% surge accordingly.

The Persian Gulf and the Red Sea:

On May 30th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf gain 22% to US$1692/TEU.

Australia & New Zealand:

On May 30th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand lost 1.8% to US$709/TEU.

South America:

On May 30th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports rose 44.6% to US$2797/TEU.