Stainless Insights in China from June 30th to July 6th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 1,990 | 3 | 0.15% |

| Foshan | 2,035 | 3 | 0.15% | ||

| Hongwang | Wuxi | 1,895 | 6 | 0.32% | |

| Foshan | 1,900 | -3 | -0.16% | ||

| 304/NO.1 | ESS | Wuxi | 1,810 | 1 | 0.08% |

| Foshan | 1,825 | -4 | -0.25% | ||

| 316L/2B | TISCO | Wuxi | 3,455 | -14 | -0.42% |

| Foshan | 3,525 | -3 | -0.08% | ||

| 316L/NO.1 | ESS | Wuxi | 3,310 | -8 | -0.26% |

| Foshan | 3,345 | -14 | -0.44% | ||

| 201J1/2B | Hongwang | Wuxi | 1,185 | 6 | 0.53% |

| Foshan | 1,175 | 1 | 0.13% | ||

| J5/2B | Hongwang | Wuxi | 1,070 | 3 | 0.29% |

| Foshan | 1,075 | 0 | 0.00% | ||

| 430/2B | TISCO | Wuxi | 1,120 | -17 | -1.65% |

| Foshan | 1,115 | -8 | -0.83% |

TREND || Macroeconomic Policies Boost Market Sentiment

Last week, stainless steel spot prices in the Wuxi market remained volatile. Positive macroeconomic developments in China lifted market sentiment—The sixth meeting of the Central Financial and Economic Affairs Commission emphasized the need to regulate disorderly and low-price competition in accordance with laws and regulations, guide enterprises to improve product quality, and promote the orderly exit of outdated production capacity.

Stainless steel futures rebounded from their lows, and the cost side stabilized with limited downside potential. Supply-side pressures have eased somewhat, but demand remains weak, offering insufficient support for significant price increases. As of Friday, the main stainless steel futures contract price rose by US$15.4/MT week-on-week to US$1910/MT, with an intraday high of US$1920/MT. LME nickel closed down US$95 to US$15,260/ton, while LME nickel inventory decreased by 1,158 tons to 202,470 tons.

300 Series: Macroeconomic boost stimulates downstream purchases

Prices for 304-grade stainless steel remained stable last week. As of Friday, the mainstream base price for privately produced 304 cold-rolled (four-foot width) in Wuxi was quoted at US$1855/MT, while hot-rolled was at US$1815/MT—both unchanged from the previous week.

Early in the week, Tsingshan opened with lower prices, prompting market agents to slash quotes and move inventory, resulting in an influx of low-priced products. However, downstream buyers remained cautious, and inventory destocking was slow. On Wednesday, the government issued a favorable policy statement on eliminating outdated capacity, triggering a rebound across commodity markets. Stainless steel futures gained on increased open interest, improving market sentiment. Agents began slightly raising offers for spot goods, and with the earlier price cuts from mills taking effect, speculative demand increased, leading to a noticeable reduction in inventory.

200 Series: Macroeconomic tailwinds support transactions

Prices for 201-grade stainless steel were generally stable with some declines. Cold-rolled 201J2 was quoted at US$1035/MT (tax-included, base gauge), down US$14/MT from the previous week. Cold-rolled 201J1 held steady at US$1155/MT, and hot-rolled 201J1 was quoted at US$1135/MT, both unchanged week-on-week.

At the beginning of the week, futures prices came under pressure, and some spot traders offered discounts, with the lowest quotes hitting US$1035/MT. As macroeconomic news on eliminating outdated capacity spread, low-priced resources in the market decreased, and traders firmed up their quotes to around US$1040/MT. However, downstream buyers were hesitant to accept higher prices, and by Friday, market prices had returned to around US$1035/MT.

400 Series: Market transactions improve

Last week, 430-grade stainless steel prices showed a slight downward trend. In the Wuxi spot market, the price for state-owned 430 cold-rolled fell to US$1120-US$1135/MT, down US$14 from last weekend. The price for 430 hot-rolled dropped to US$1040/MT, down US$7/MT from the previous week.

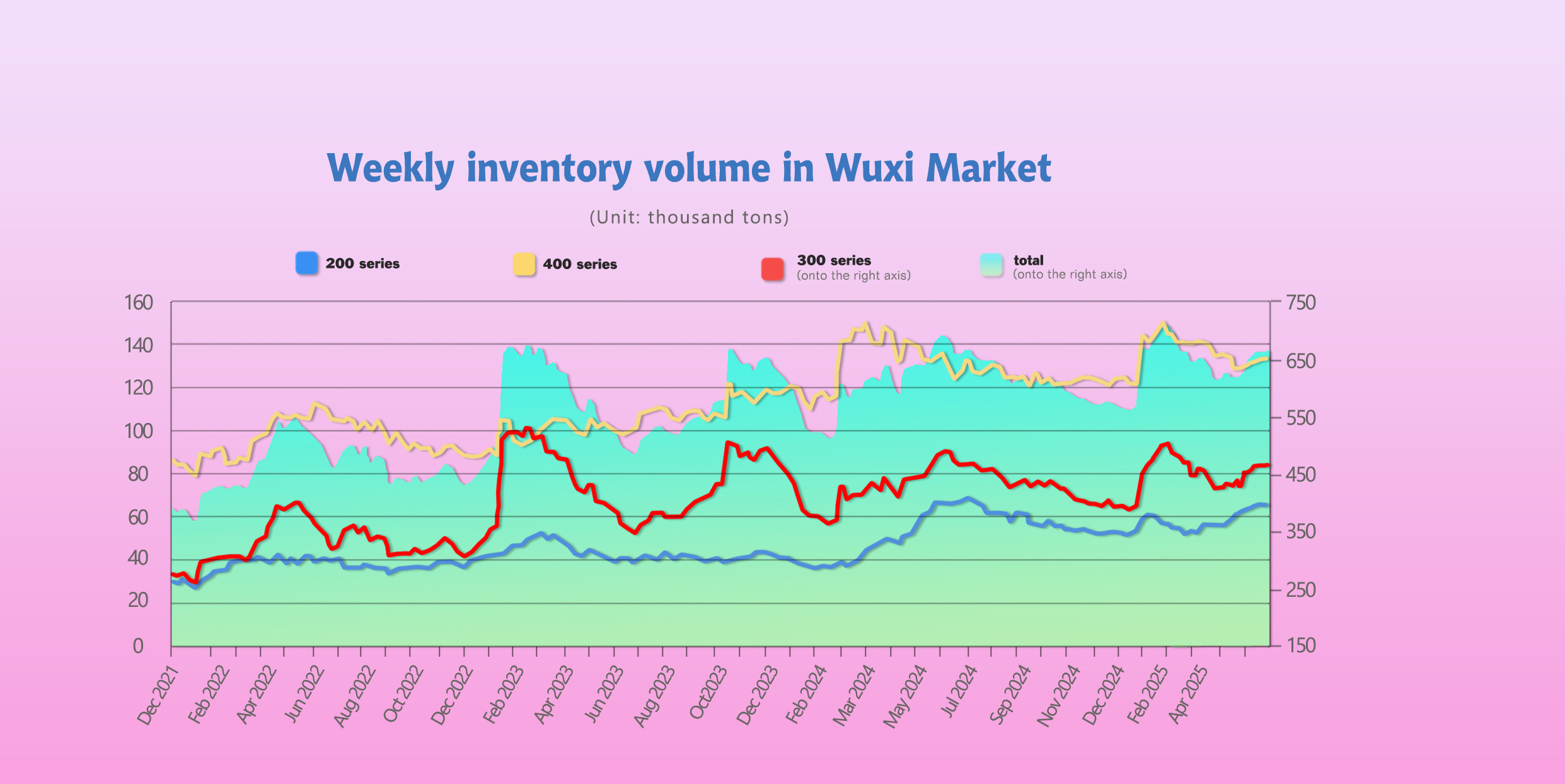

INVENTORY || Nearly 40,000 Tons De-stocked Last week

As of July 3rd total inventory in Wuxi sample warehouses decreased by 38,711 tons to 624,994 tons. Breakdown:

200 Series: 248 tons down to 65,460 tons.

300 Series: 30,184 tons down to 434,351 tons.

400 Series: 8,279 tons down to 125,183 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Jun 26th | 65,708 | 464,535 | 133,462 | 663,705 |

| Jul 3rd | 65,460 | 434,351 | 125,183 | 624,994 |

| Difference | -248 | -30,184 | -8,279 | -38,711 |

300 Series: Mills Cut Prices to Stimulate Sales, Market Consumption Improves

Stainless steel futures rebounded from lows, and mill price cuts to stimulate orders were well received. Overall market sentiment improved, and downstream buyers showed increased willingness to restock at low prices, leading to a clear reduction in inventory.

200 Series: Fewer Arrivals Ease Supply Pressure

Prices for 201-grade stainless steel mostly held steady, and macro policies helped lift downstream sentiment. Mill production and agent contract volumes for July have both been reduced, leading to a drop in available supply.

A slight inventory drawdown is expected next week, depending on actual market transactions.

400 Series: Cost Support Stabilizes, Downstream Procurement Increases

From a structural standpoint, there was an increase in cold-rolled stock from Jiugang, but significant reductions in both cold-rolled and hot-rolled stock from Taigang led to an overall sharp drop in inventory.

Despite some new arrivals from mills, improving downstream procurement led to a strong rebound in 400 series stainless steel transactions. Spot inventories were quickly digested, and the turnover of spot resources accelerated.

SUMMARY || Oversupply Persists

Stainless steel prices rose last week.

Anti–“cutthroat competition” policies lifted sentiment in bulk commodity markets, though downstream demand still mainly came from just-in-time purchasing.

Mill output has declined slightly but remains at high levels, so the oversupply situation remains unresolved.

There’s still pressure from high social inventory and ample spot availability.

The market will continue to watch downstream demand, mill production schedules, and social inventory reduction.

Stainless steel prices are expected to remain volatile going forward.

300 Series: Domestic and international macro sentiment is gradually improving, with the possibility of another round of reserve requirement ratio (RRR) or interest rate cuts.

On the supply side, as production costs stabilize and mill output reduction plans take effect, incoming supply to the market has declined.

On the demand side, a price rebound from the bottom has strengthened downstream buying interest.

The supply-demand balance is improving, inventory is being digested faster, and the momentum for stainless steel price increases is strengthening.

Prices for 304 cold-rolled and hot-rolled are expected to follow futures and trend upward in a slightly bullish consolidation.

200 Series: Macro policies have buoyed market sentiment, and the nonferrous metals sector remains strong, pushing copper prices to remain in a high range.

Mills plan to reduce output further in July, alleviating supply-side pressure and allowing inventory to begin depleting.

However, downstream demand needs close monitoring.

Prices for 201J2 are expected to remain mostly stable in the short term.

400 Series: Last week, retail prices for high-chromium raw materials were stable, continuing to support 400 series stainless steel costs.

Procurement demand from downstream buyers continues to improve.

Overall, mill deliveries were lower than sales volumes, significantly easing supply-side pressure.

Support for prices has improved from a previously weak position.

Prices for 430 stainless steel are expected to remain stable next week.

MACRO || Mid-Year Review of the Stainless Steel Market in 2025

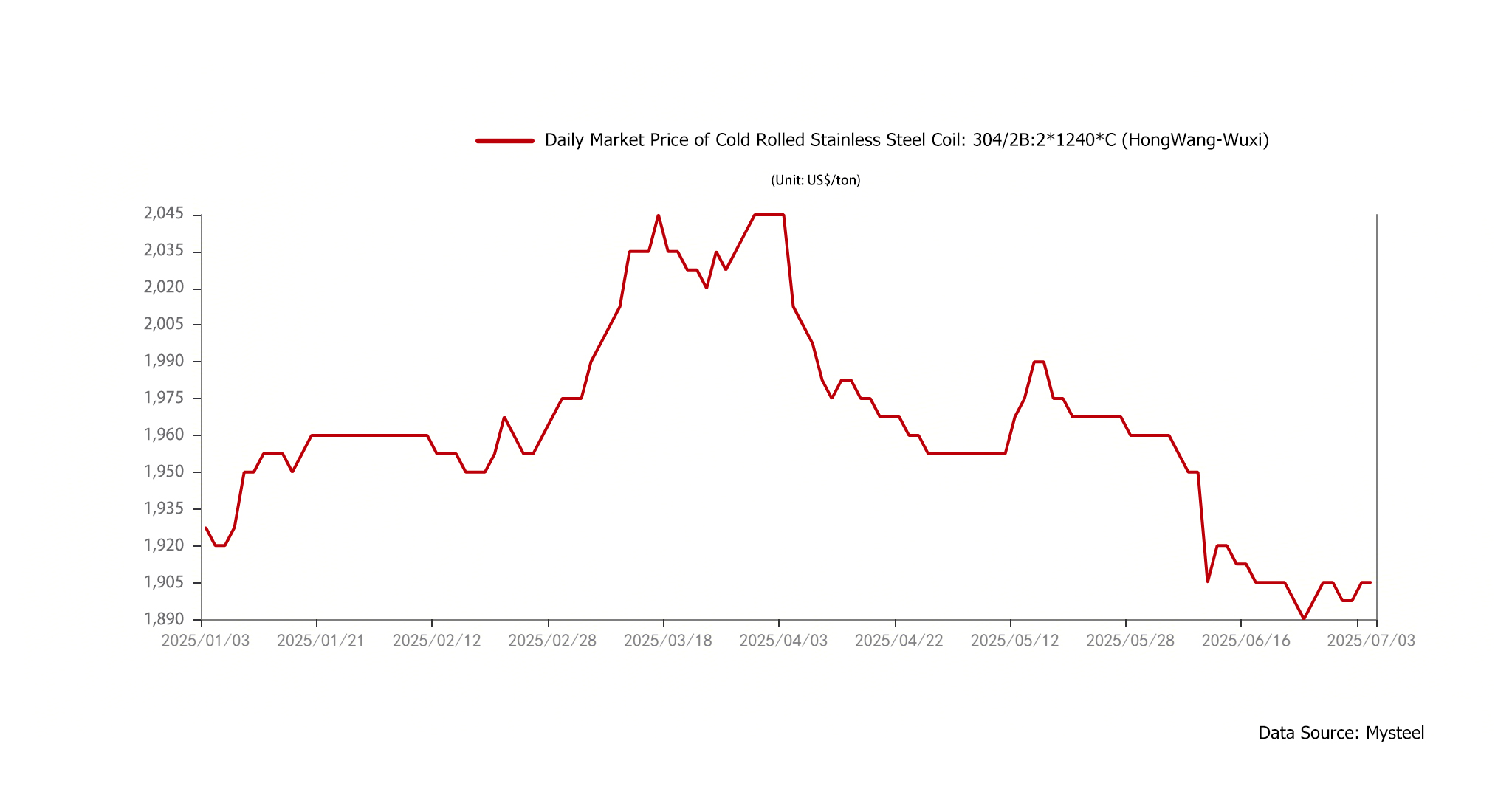

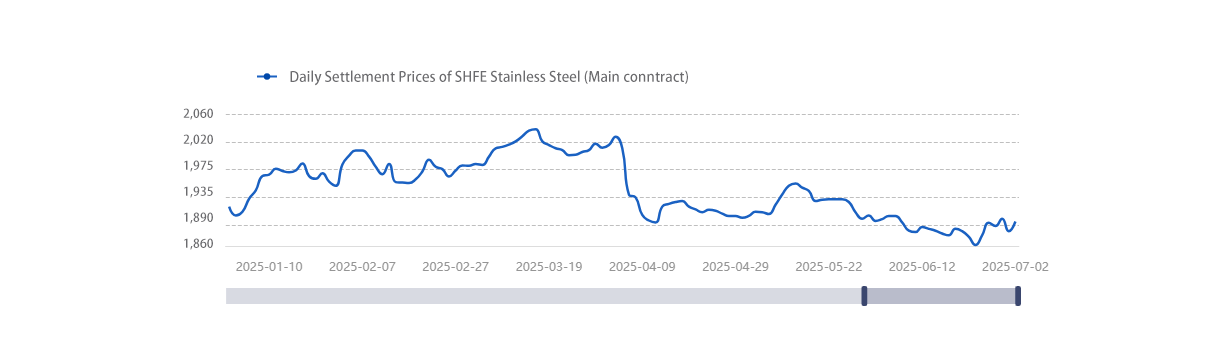

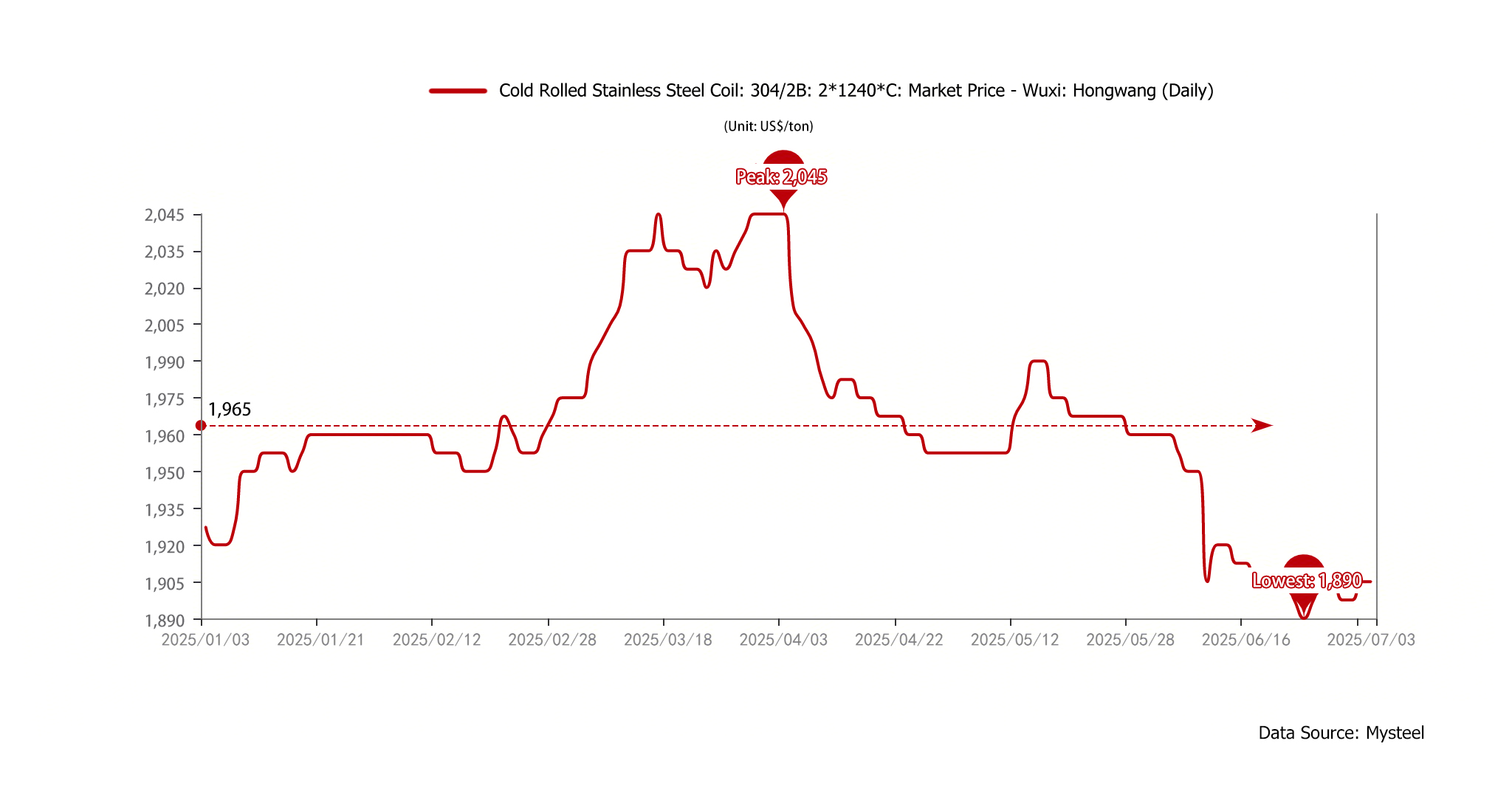

In the first half of 2025, the stainless steel market followed a trajectory of rising first and then falling (using Wuxi market 304 cold-rolled Hongwang as an example). Prices initially trended upward, supported by macro policies and cost factors, peaking in March. However, in Q2, prices declined continuously due to weak demand, high inventory levels, and falling raw material costs.

Price Trends: Futures and Spot Prices Under Pressure

1.Futures Market:

The settlement price of the stainless steel main contract on the Shanghai Futures Exchange rose from US$1800/MT in early January to US$1917/MT in mid-March (the year’s peak). However, starting in April, prices plunged under pressure from U.S. tariff policies, falling to US$1741/MT on June 24 (the year’s low), a decline of 9.2%.

2.Spot Market:

As a mainstream product, the average price of 304 cold-rolled stainless steel in the first half was US$1965/MT. The highest price reached US$2045/MT (April 3rd), while the lowest dropped to US$1890/MT (June 24th).

From January to March, prices rose temporarily due to favorable macro policies and mills supporting prices. But beginning in April, weak demand and increasing inventory led to continuous price declines.

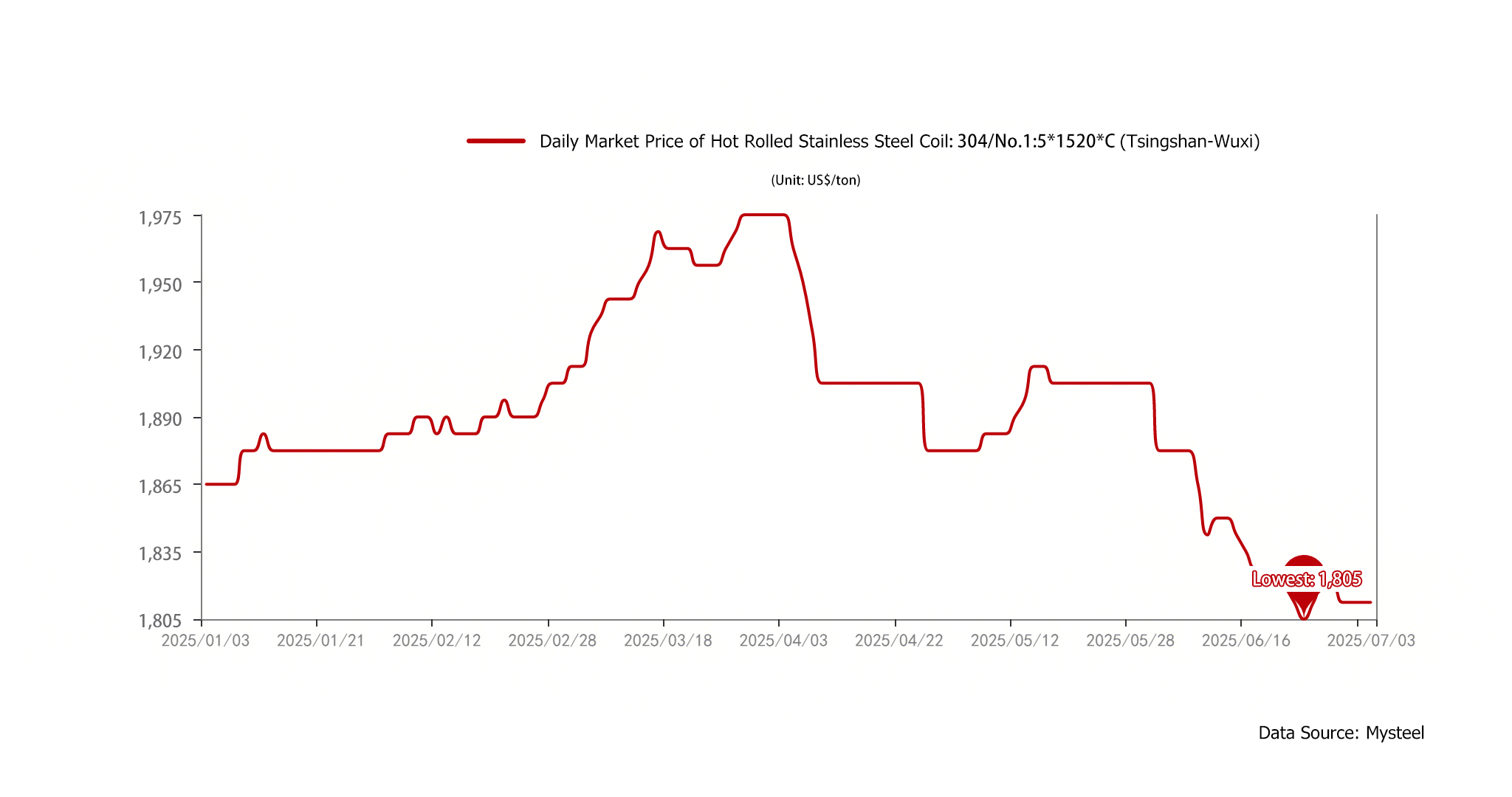

By June, with falling futures and sluggish end-user procurement, prices hit multi-year lows; 304 hot-rolled from private mills in Wuxi even fell below US$275.

Supply and Demand: Supply Contracts but Weak Demand Prevails

Supply Fundamentals:

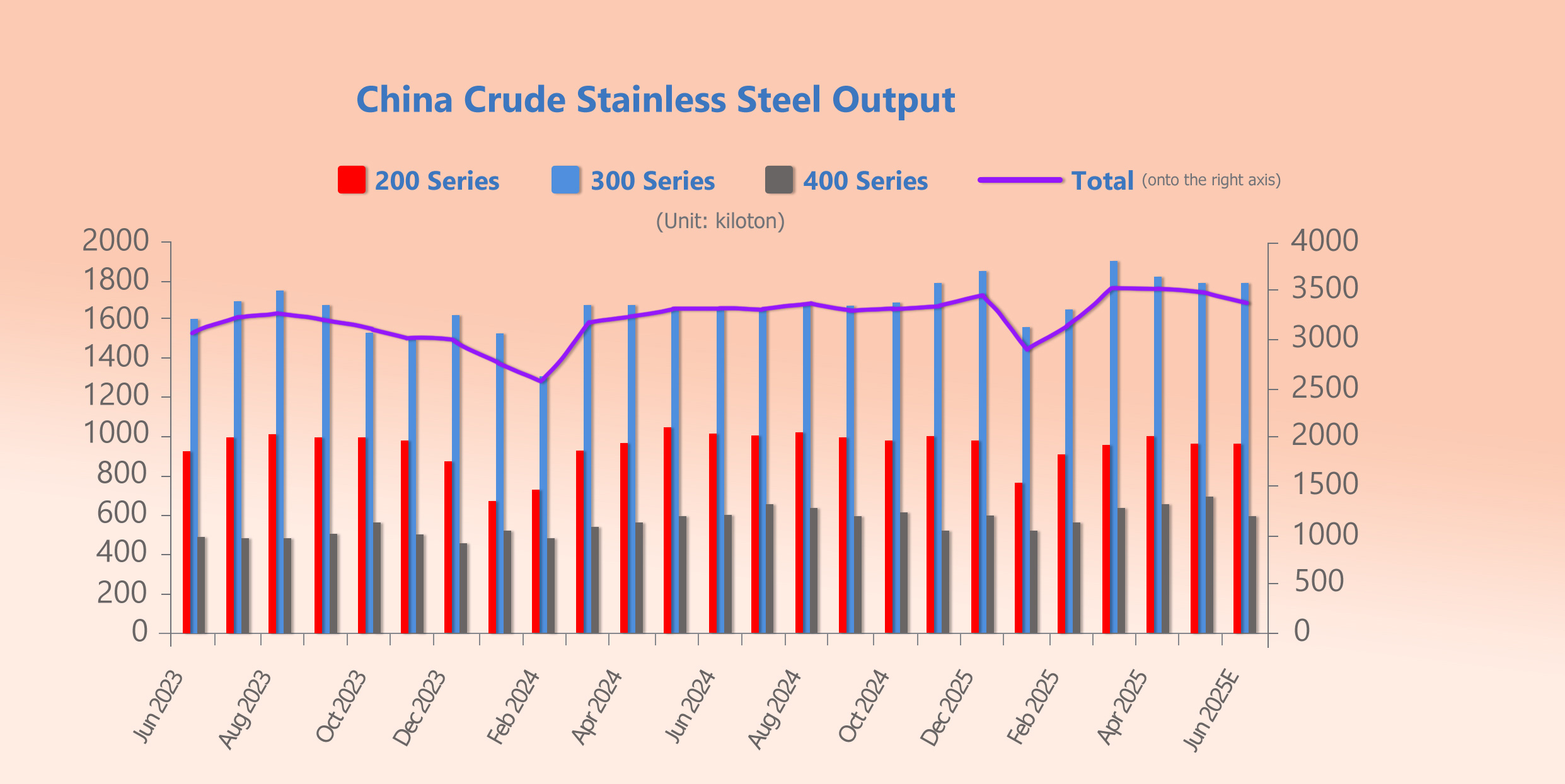

In May, China’s stainless steel crude steel output was 3.4644 million tons, down 1.46% month-on-month.

Within that, 300-series output stood at 1.7841 million tons (down 2.17% MoM), as some mills reduced production due to losses.

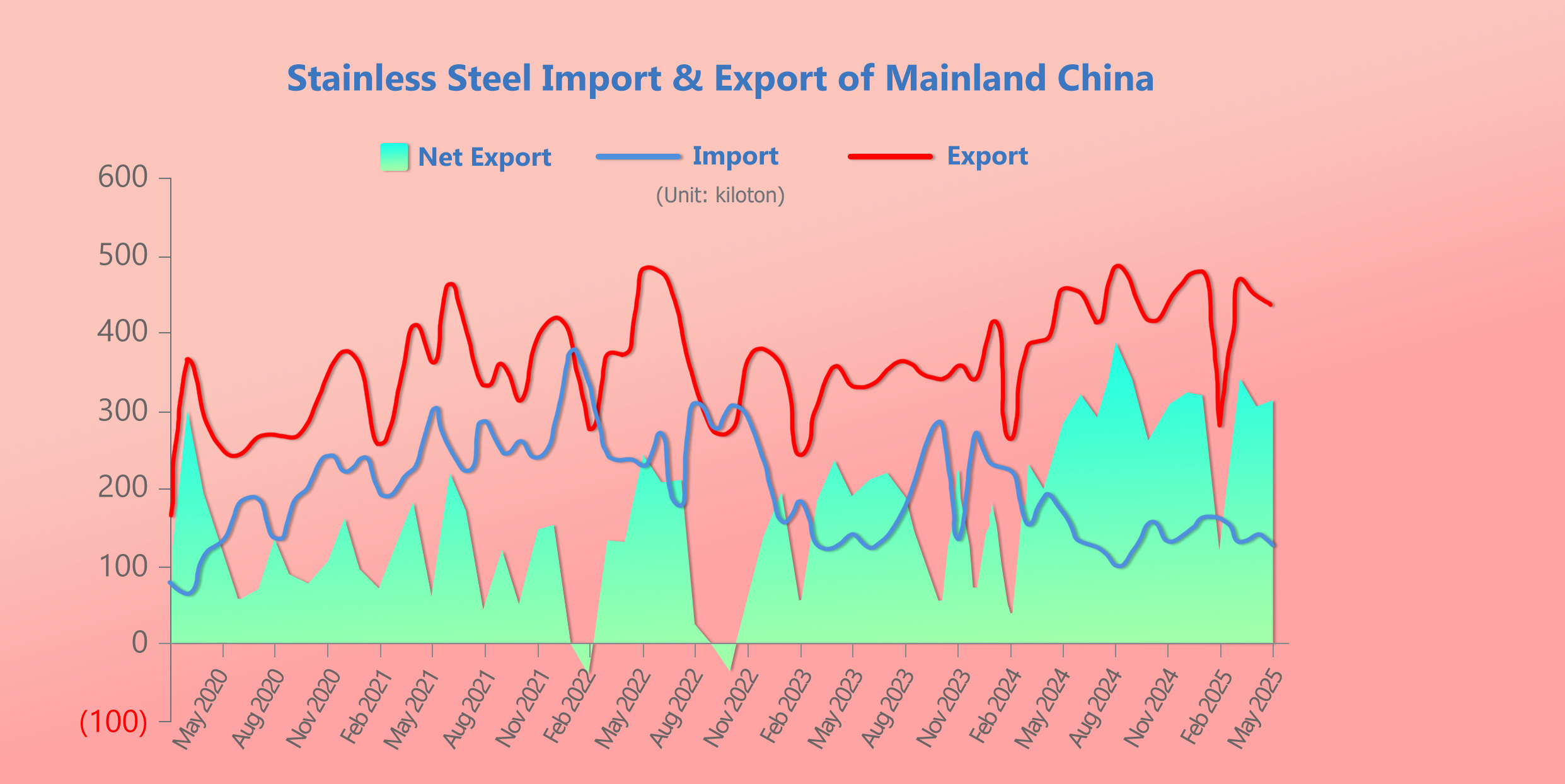

Imports Continue to Shrink:

May imports were 125,100 tons, down 28.3% YoY.

Total imports from January to May reached 718,000 tons, down 26.5% YoY.

Costs, Demand, and Inventory

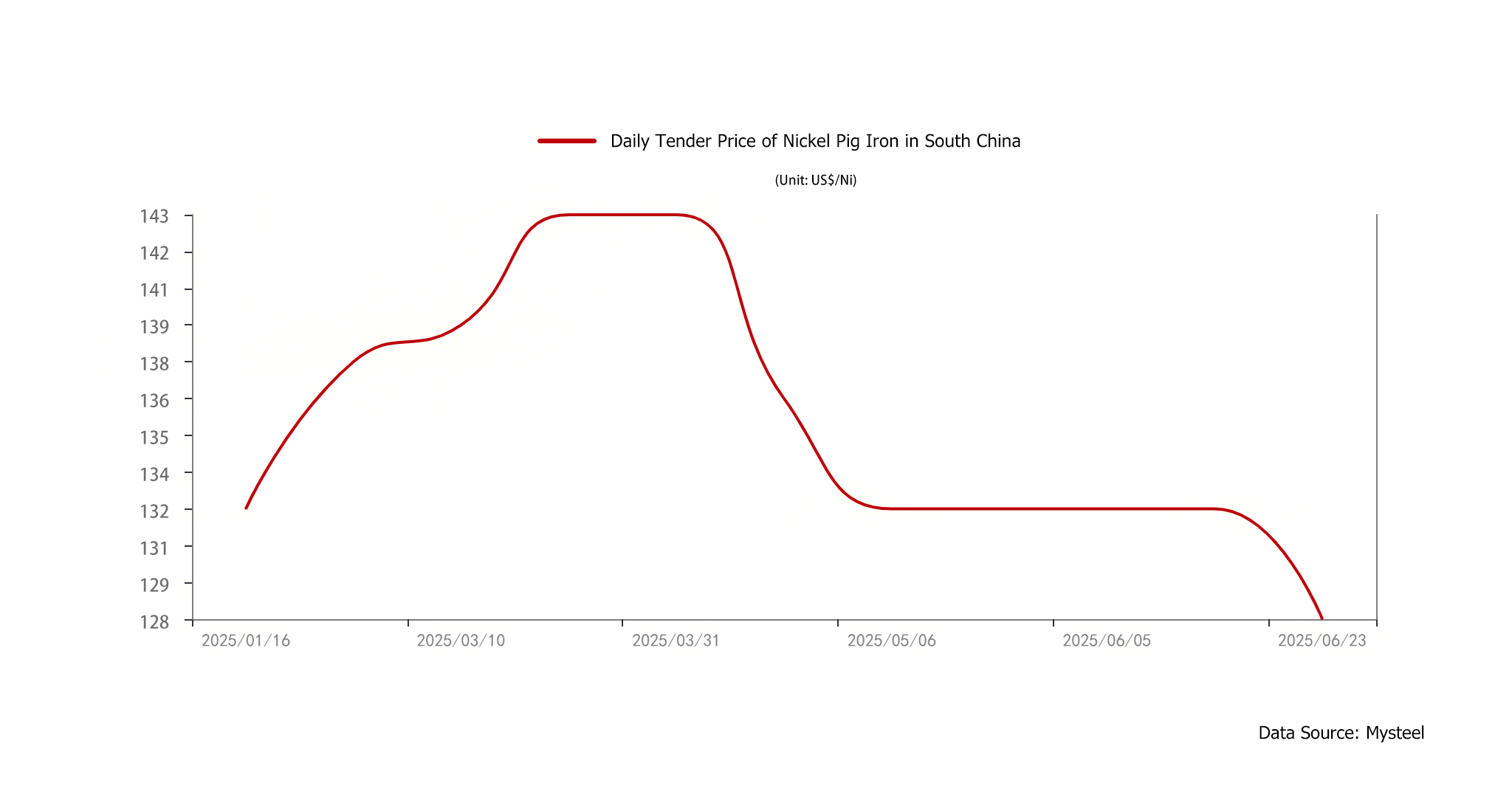

Raw material costs fell, eroding cost support. Nickel pig iron (NPI) transaction prices dropped, ferrochrome tender prices held steady in June, but retail prices fell, weakening stainless steel’s cost support.

Export Resilience:

Cumulative exports from January to May were 2.11 million tons, up 10.4% YoY.

However, May’s single-month export volume dropped to 436,300 tons, down 2.6% MoM.

High Social Inventory:

By the end of June, nationwide stainless steel social inventory stood at 1.1544 million tons (with 300-series accounting for 685,000 tons).

Though this was down slightly by 3,000 tons from the previous month, it remains at a historically high level.

Outlook

Currently, the market is in a seasonal demand lull — end-users are mainly purchasing based on actual needs, and there’s no significant recovery in manufacturing orders.

In June, 300-series production rose by 10,000 tons month-on-month while inventory was slow to clear, so the oversupply situation persists.

400-series production declined by 100,000 tons in June, and if losses widen, further production cuts may be triggered.

The industry urgently needs self-discipline and innovation to break out of the current dilemma.

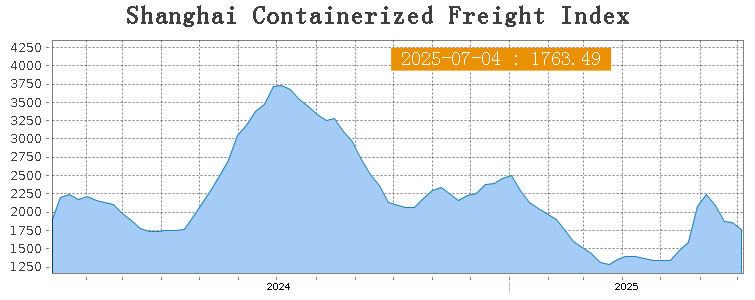

SEA FREIGHT || Shipping Market Remains Stable

Last week, China's export container shipping market remained stable, with continued divergence across long-haul routes. The composite index continued to adjust downward.

On July 4th, the Shanghai Containerized Freight Index (SCFI) fell 0.4% to 1763.49 points.

Europe/ Mediterranean:

On July 4th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$2101/TEU, which increased by 3.5%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$2869/TEU, which dip 3.9% from previous week.

North America:

Transport demand lacked further growth momentum, supply-demand balance remained weak, and spot market booking prices continued to fall.

On July 4th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$2089/FEU and US$4724/FEU, reporting 19% and 12.6% slide accordingly.

The Persian Gulf and the Red Sea:

On July 4th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf shrank 7% to US$1916/TEU.

Australia & New Zealand:

On July 4th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand gained 2% to US$853/TEU.

South America:

On July 4th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports increased 2.5% to US$6220/TEU.