Stainless Insights in China from June 2nd to June 8th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,045 | -25 | -1.30% |

| Foshan | 2,090 | -25 | -1.27% | ||

| Hongwang | Wuxi | 1,950 | -10 | -0.54% | |

| Foshan | 1,960 | -20 | -1.06% | ||

| 304/NO.1 | ESS | Wuxi | 1,875 | -18 | -1.03% |

| Foshan | 1,890 | -21 | -1.18% | ||

| 316L/2B | TISCO | Wuxi | 3,535 | 0 | 0.00% |

| Foshan | 3,605 | 0 | 0.00% | ||

| 316L/NO.1 | ESS | Wuxi | 3,410 | 6 | 0.19% |

| Foshan | 3,420 | 3 | 0.09% | ||

| 201J1/2B | Hongwang | Wuxi | 1,220 | -7 | -0.63% |

| Foshan | 1,215 | -6 | -0.57% | ||

| J5/2B | Hongwang | Wuxi | 1,110 | -8 | -0.77% |

| Foshan | 1,115 | -6 | -0.63% | ||

| 430/2B | TISCO | Wuxi | 1,155 | 0 | 0.00% |

| Foshan | 1,135 | -4 | -0.34% |

TREND || Ample Supply in the Market, Weak Demand During Off-Season

Last week, spot prices for stainless steel in the Wuxi market saw a slight decline. The futures market fluctuated in line with macroeconomic sentiment. On the cost side, falling raw material prices led to some downward adjustments. As steel mill profits recovered, production increased, leading to continued market arrivals and a buildup in inventory. With prices at relatively low levels, market participants remain cautious and are not optimistic about the short-term outlook. Stainless steel has returned to a fundamental supply-demand imbalance, and there is little momentum for a turnaround in the near term. The continued weak performance of prices over the past two weeks has widened the fluctuation range in the futures market, which may remain in a low-level oscillating pattern moving forward. Last week, the main stainless steel futures contract closed at US$1905/MT, down 0.04% week-on-week, with a weekly low of US$1890/MT.

300 Series: Increase in Arrivals, Inventory Build-Up Suppresses Price Rebound

The 304 spot market declined slightly last week. As of Friday, the mainstream base price for private 304 cold-rolled four-foot coils in Wuxi was reported at US$1905/MT, down US$7/MT from previous Friday. Private hot-rolled coils were quoted at US$1875/MT, down US$14/MT from previous week. After the holiday, Tsingshan opened with lower prices, and market agents followed suit by reducing their quotations. However, due to the weak futures performance, downstream buyers showed limited interest and mostly stuck to low-price purchases to meet immediate needs. Higher-priced materials were difficult to move. On Wednesday, futures prices rose slightly, supported by positive sentiment from policy expectations, but the market remained cautious. On Thursday, prices again returned to being dictated by weak fundamentals, with futures rising briefly before falling back. Holiday trading was subdued, and increased arrivals from the Tsingshan system led to a noticeable inventory buildup, which capped the potential for a price rebound. Current prices remain in a narrow oscillating range.

200 Series: Mills Lead Price Cuts Again, Market Offers More Discounts

The 201 market remained weak last week. The base price for 201J2 cold-rolled coils dropped to US$1075/MT; 201J1 cold-rolled was quoted at US$1185/MT, and 201J1 hot-rolled at US$1160/MT. Futures showed mixed performance during the week, and market sentiment was largely wait-and-see. On Wednesday, Tsingshan opened again with across-the-board price cuts of US$14/MT for both cold-rolled and hot-rolled 201. All agents and traders followed suit with lower prices. Mainstream transaction prices gradually dropped to the US$1075/MT level. Downstream purchasing focused on low prices, leading to slight increases in both cold-rolled and hot-rolled inventories.

400 Series: Noticeable Inventory Build-Up, Weakening Cost Support, Rising Bearish Factors

Last week, the 430 market was relatively weak. As of Friday, the Wuxi spot market quoted state-owned 430 cold-rolled coils at around US$1155/MT-US$1160/MT, unchanged from previous weekend. However, the price for state-owned 430 hot-rolled coils fell by US$14/MT to US$1055/MT.

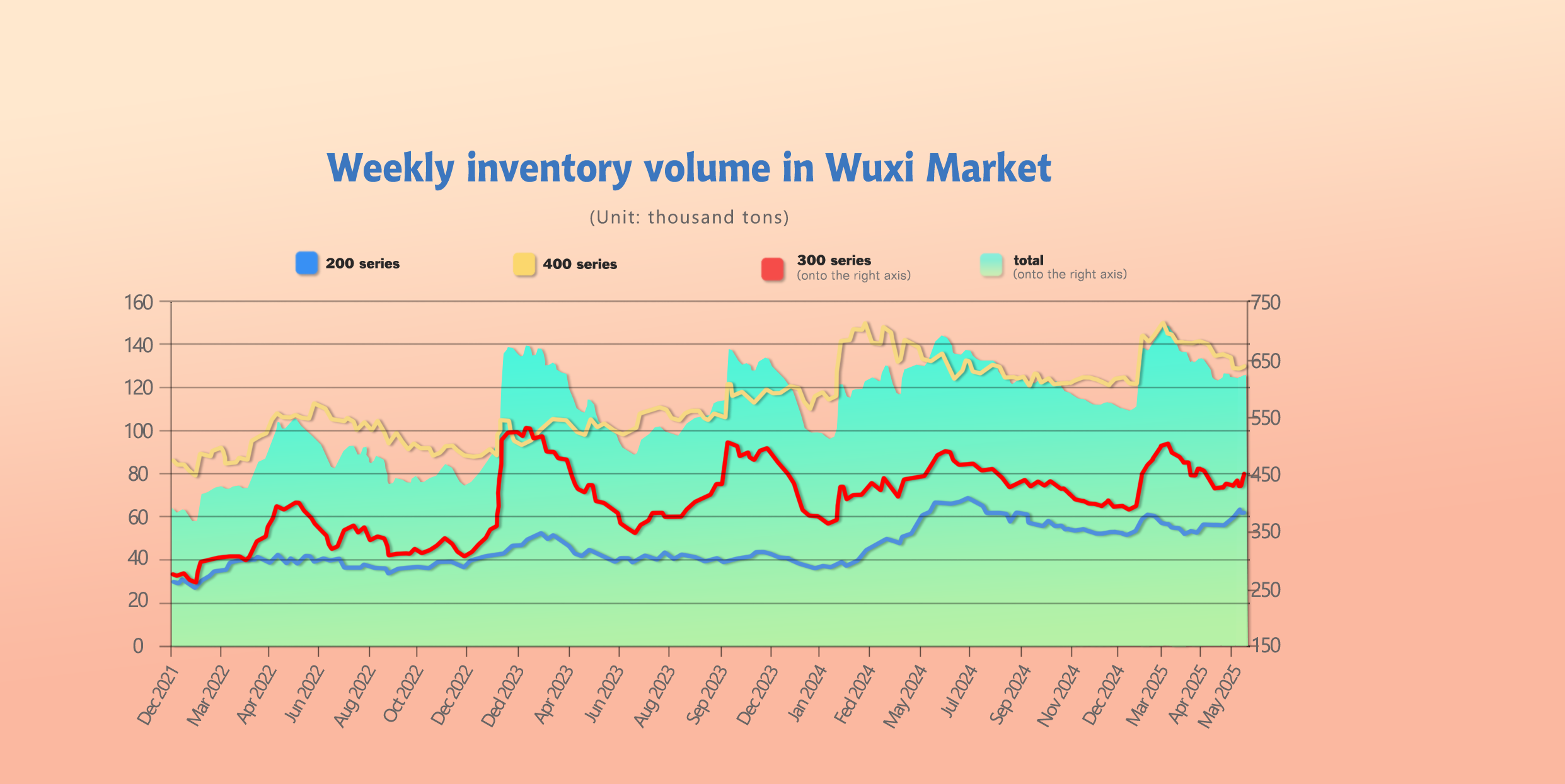

INVENTORY || A Reduction of 150,000 Tons—Enough to Offset the Off-Season Slump?

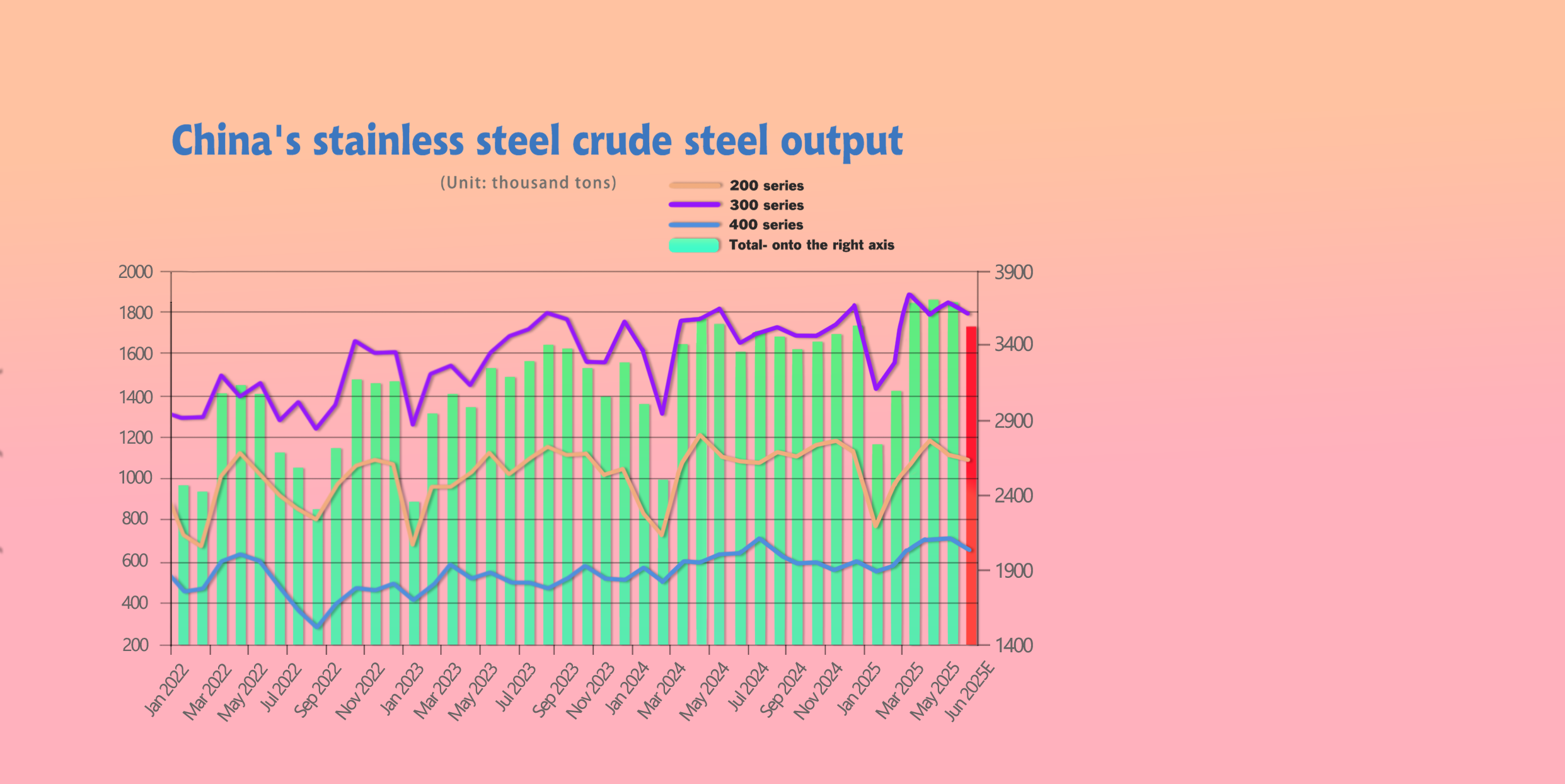

As the market enters the off-season for consumption, inventory pressure has led to a month-on-month production cut of 30,000 tons at steel mills, with a further 150,000-ton reduction scheduled for June. China's total stainless steel output continues to contract.

In May 2025, crude stainless steel output from large-scale domestic enterprises reached 3.6719 million tons, a month-on-month decrease of 26,000 tons or 0.7%, but a year-on-year increase of 127,600 tons or 3.60%.

Production varied across different series in May, as detailed below:

200 series: 1.1107 million tons, down 80,400 tons MoM (-6.75%), up 3,800 tons YoY (+0.34%).

300 series: 1.8498 million tons, up 56,000 tons MoM (+3.12%), up 38,400 tons YoY (+2.12%).

400 series: 711,400 tons, down 1,600 tons MoM (-0.22%), up 85,400 tons YoY (+13.64%).

Currently, both mill and market inventories remain above historical averages, and destocking is progressing slowly. With demand in its seasonal lull, many steel mills have announced plans for maintenance and output cuts. Preliminary statistics show that in June 2025, domestic crude stainless steel output is expected to fall by approximately 150,000 tons month-on-month to around 3.52 million tons. Specifically:

300 series: Decrease by 55,000 tons MoM to 1.795 million tons.

200 series: Decrease by 25,000 tons MoM to 1.086 million tons.

400 series: Decrease by 69,000 tons MoM to 643,000 tons.

Overall, in the short term, downstream demand is unlikely to improve significantly during the off-season. Market absorption capacity is slowing, and inventory reduction remains difficult. With subdued demand expectations, many mills are voluntarily cutting production due to limited orders and cost pressures. As crude steel output in May and scheduled production in June both continue to shrink, short-term cost support is weakening. Attention should be paid to how production cuts at mills may push raw material prices down. Stainless steel prices in June are likely to continue a trend of fluctuating downward.

As of June 5th, total inventory in Wuxi sample warehouses increased by 20,833 tons to 647,494 tons. Breakdown:

200 Series: 909 tons up to 63,492 tons.

300 Series: 18,074 tons up to 453,942 tons.

400 Series: 1,850 tons up to 130,060 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| May 29th | 62,583 | 435,868 | 128,210 | 626,661 |

| Jun 5th | 63,492 | 453,942 | 130,060 | 647,494 |

| Difference | 909 | 18,074 | 1,850 | 20,833 |

200 Series: Continued Arrivals

Last week, the 200 series inventory in the Wuxi market increased by 900 tons to 63,500 tons. (Cold-rolled stock increased by 600 tons, hot-rolled stock increased by 300 tons.)

In terms of inventory structure, Baosteel Desheng has continued to deliver 201 cold-rolled and hot-rolled materials after the holiday, increasing the volume of available circulating resources in the market.

In the short term, 201 prices are expected to remain weak. Attention should be paid to the upcoming production trends at steel mills. Inventory is projected to see a slight buildup next week.

300 Series: Weak Off-Season Demand, Significant Inventory Accumulation

Last week, the 300 series inventory in the Wuxi market increased by 18,100 tons to 453,900 tons (cold-rolled stock rose by 5,900 tons; hot-rolled stock rose by 12,200 tons). After the holiday, prices from TISCO dropped, and market agents followed suit by lowering quotations, resulting in weakened market confidence.

Downstream buyers continued to procure only for immediate low-cost needs, while speculative demand remained limited. With weak off-season demand expectations, inventory continues to stay at high levels.

400 Series: Slower Inventory Depletion

In terms of supply, the 400 series inventory in the Wuxi market increased by 1,900 tons to 130,100 tons, with cold-rolled stock rising by 1,200 tons and hot-rolled stock rising by 700 tons.

The main contributing factors include concentrated arrivals of spot goods from mills and slower transaction activity due to the Dragon Boat Festival holiday.

Additionally, falling raw material costs have weakened the cost support for stainless steel, though overall cost levels remain relatively high.

400 series stainless steel producers continue to face profitability challenges. The Wuxi spot market is expected to accelerate inventory depletion next week.

SUMMARY || Weak Confidence in the Stainless Steel Market

Stainless steel prices declined last week.

Demand remains primarily driven by essential procurement, while steel mill production plans have decreased slightly but still remain at high levels, making it difficult to reverse the oversupply situation.

Inventory at social warehouses is being digested slowly, and spot resources remain abundant.

Attention should be given to downstream demand's capacity to absorb supply, as well as changes in mill production and inventory drawdown.

The stainless steel market is expected to continue fluctuating at low levels in the near term.

300 Series: The seasonal demand downturn is gradually setting in, and with prices remaining undervalued, downstream buyers mostly stick to low-cost essential purchases, showing limited interest in higher-priced materials.

On the supply side, arrivals remain stable and inventories are high, which suppresses any potential price rebound.

From a macro perspective, domestic economic data has been relatively strong, while U.S. core PCE has risen, intensifying the tug-of-war between bullish and bearish sentiment.

In the short term, 304 cold- and hot-rolled spot prices are expected to fluctuate along with the futures market. Monitor trading activity and inventory depletion closely.

200 Series: With raw material costs for copper and manganese staying elevated, steel mill margins have been compressed.

Production plans for 200 series crude stainless steel are set to decline in June, easing supply pressure in the market.

However, as the industry enters a seasonal lull, downstream demand remains sluggish and purchasing sentiment is poor.

Prices for 201 cold- and hot-rolled products are expected to continue weak performance in the short term.

400 Series: Last week, retail prices for high-carbon ferrochrome weakened, gradually approaching June's mainstream mill tender prices.

This has slightly undermined cost support for 400 series stainless steel.

Given weak downstream demand and continued inventory buildup in the spot market last week, 430 prices are expected to trend steadily to slightly weaker levels next week.

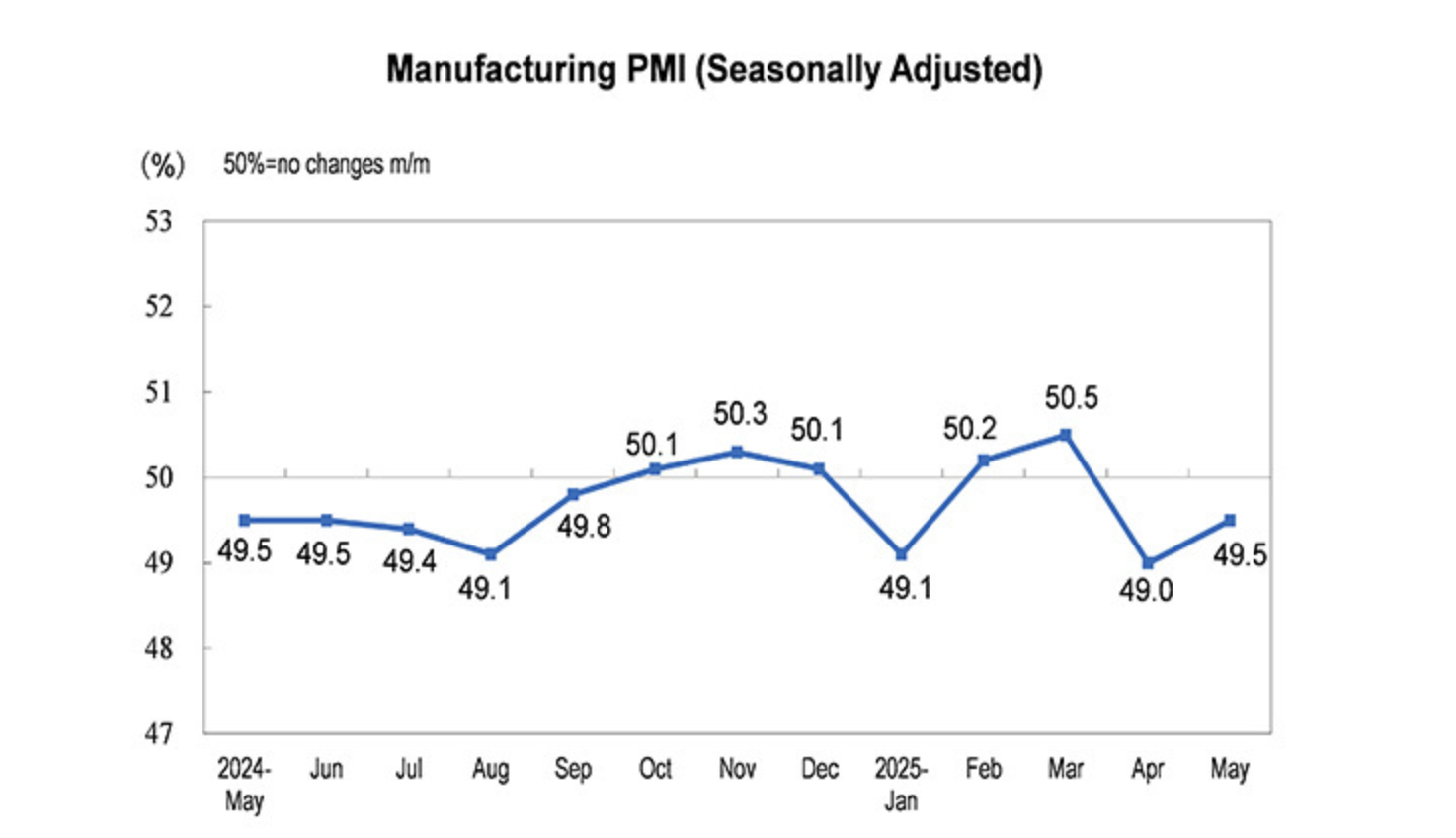

MACRO || PMI Rebounds, China’s Exports to the U.S. Plunge by 34.5%

On June 9, China’s General Administration of Customs announced that the total value of China's goods trade imports and exports for the first five months of 2025 reached 2.52 trillion USD, a year-on-year increase of 2.5%, continuing the growth trend.Of this, exports were US$1.5 trillion, up 7.2%, while imports were US$1.02 trillion, down 3.8%.

In May alone, total trade amounted to US$3.81 trillion, an increase of 2.7%. Exports in May reached USD 535.8 billion, up 6.3%. Notably, exports to ASEAN, the EU, Africa, and the five Central Asian countries increased by 16.9%, 13.7%, 35.3%, and 8.8%, respectively.

Additionally, according to data released by the General Administration of Customs and measured in U.S. dollars, China’s exports to the United States in May totaled USD 28.819 billion, a sharp year-on-year decline of 34.5% (compared to a 21% drop in April). Imports from the U.S. in May amounted to USD 10.807 billion, down 18.1% year-on-year (compared to a 13.8% drop in April).

In terms of macroeconomic indicators, the manufacturing Production Index for May rose to 50.7% (previous value: 49.8%). The New Orders Index was 49.8%, and the New Export Orders Index reached 47.5%, both up by 0.6 and 2.8 percentage points, respectively.

Amid a phase of stabilizing demand and expectations, the return of production to expansion territory reflects the strong resilience and risk resistance of China’s economy. On the external demand front, following former U.S. President Trump’s suspension of retaliatory tariffs against other countries and the achievement of a phase-one result in U.S.-China negotiations in Geneva—where both sides reduced tariffs—exports have been buoyed by a combination of domestic "rush-to-export" momentum and international "rush-to-order" behavior.

In May, China–U.S. West Coast container freight rates stabilized and rebounded. The China-to-U.S. West Coast Export Container Freight Index rose 8.7% month-on-month to 908.14, recovering from the price shock caused by retaliatory tariffs.

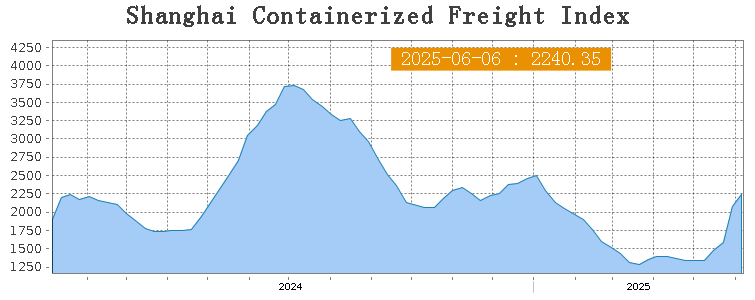

SEA FREIGHT || Market Remains Generally Stable with Slight Fluctuations on Some Routes

Last week, China's container export shipping market maintained an overall positive trend. Freight rates on most major ocean routes continued to rise, pushing the composite index further upward. On June 6th, the Shanghai Containerized Freight Index (SCFI) rose 8.1% to 2240.35 points.

Europe/ Mediterranean:

Data from S&P Global shows that the final Eurozone Composite PMI was revised up to 50.2, surpassing the initial contraction-level reading of 49.5. This suggests that the European economy is showing more resilience than previously expected. Manufacturing PMI continued to exhibit modest growth, though the services PMI dropped to a six-month low. Europe is still navigating challenging tariff negotiations, and the region’s economic outlook remains uncertain. Last week, transport demand grew steadily, and market freight rates continued to rise.

On June 6th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1667/TEU, which increased by 5%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$3302/TEU, which inflated 7.9% from previous week.

North America:

According to research firm ADP, the U.S. added just 37,000 private-sector jobs in May—well below market expectations and the lowest figure since March 2023—indicating a significant cooling in the job market. The “tariff war” is beginning to show a tangible impact on the U.S. economy. Furthermore, last week, President Trump announced another increase in import tariffs on steel and aluminum to 50%. The ongoing changes in tariff policy are casting a shadow over the economic outlook.

Despite this, the shipping market continues to benefit from a wave of “rush exports.” Cargo volumes remain high, supply and demand fundamentals remain tight, and spot booking prices continued to rise.

On June 6th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$5606/FEU and US$6939/FEU, reporting 8.4% and 11.1% growth accordingly.

The Persian Gulf and the Red Sea:

On June 6th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf surged 14% to US$1929/TEU.

Australia & New Zealand:

On June 6th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand lost 3.2% to US$686/TEU.

South America:

On June 6th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports exploded 41.5% to US$3959/TEU.