Stainless Insights in China from May 12th to May 18th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,065 | 17 | 0.88% |

| Foshan | 2,105 | 17 | 0.86% | ||

| Hongwang | Wuxi | 1,960 | 21 | 1.16% | |

| Foshan | 1,985 | 23 | 1.12% | ||

| 304/NO.1 | ESS | Wuxi | 1,905 | 14 | 0.79% |

| Foshan | 1,915 | 24 | 1.37% | ||

| 316L/2B | TISCO | Wuxi | 3,480 | 21 | 0.63% |

| Foshan | 3,565 | 21 | 0.62% | ||

| 316L/NO.1 | ESS | Wuxi | 3,350 | 21 | 0.66% |

| Foshan | 3,375 | 22 | 0.68% | ||

| 201J1/2B | Hongwang | Wuxi | 1,260 | 23 | 2.00% |

| Foshan | 1,240 | 15 | 1.39% | ||

| J5/2B | Hongwang | Wuxi | 1,145 | 15 | 1.49% |

| Foshan | 1,140 | 15 | 1.53% | ||

| 430/2B | TISCO | Wuxi | 1,160 | 0 | 0.00% |

| Foshan | 1,150 | -3 | -0.27% |

TREND || Policy Support Leads, Followed by Gradual Supply-Demand Recovery — Price Gains Slow but Steady

Boosted by substantial progress in high-level China–U.S. trade talks, the stainless steel market saw a strong upward trend last week. In Wuxi, spot stainless steel prices followed the futures market in a mild rebound. On the cost side, falling raw material prices led to slight reductions in production costs. However, due to ongoing losses, steel mills reduced output or shifted production, easing supply-side pressure. As a result, the supply-demand balance improved and inventory declined slightly.

As of Friday, the main stainless steel futures contract rose by US$28.83/MT from the previous week to US$1945/MT, marking a weekly gain of 2.16%. This move successfully broke through the price high set since reciprocal tariffs were imposed, gradually filling the previous price gap. In the spot market, stainless steel prices rose by US$14-US$42/MT last week.

300 Series: Macro Optimism Boosts Confidence, Supply-Demand Recovery in Progress

304 spot prices saw a moderate rise last week. As of Friday, the mainstream base price for private cold-rolled four-foot 304 in Wuxi was quoted at US$1925/MT, up US$28/MT from last Friday. Private hot-rolled 304 was quoted at US$1910/MT, an increase of US$21/MT.

Early in the week, the joint statement from China and the U.S. on tariff-related cooperation sparked a rebound in both futures and spot prices. Downstream sentiment improved, prompting distributors to raise their quotations. Market activity picked up, end-users stepped in to purchase, and overall transactions were active. Inventory levels declined as a result.

200 Series: Mill Price Guidance Spurs Gains, But High Prices Meet Resistance

201 prices generally strengthened last week. J2 cold-rolled was quoted around US$1125/MT, J1 cold-rolled at US$1240/MT, and J1 hot-rolled at US$1195/MT.

The futures market showed a strong-to-weak pattern during the week. Following the China–U.S. joint statement on the 12th, prices rebounded. On Thursday, Tsingshan Group raised both cold and hot-rolled 201 prices by US$14/MT, fueling optimism in the market and prompting traders to chase higher offers. However, downstream buyers showed limited acceptance of higher prices, and market sentiment turned more cautious, leading to a slowdown in transaction activity.

400 Series: Improved Transactions, Prices Stabilize

430 prices remained stable last week. In the Wuxi spot market, state-owned cold-rolled 430 was quoted steadily at US$1160-US$1170/MT, and hot-rolled 430 at US$1085/MT — unchanged from last week’s close.

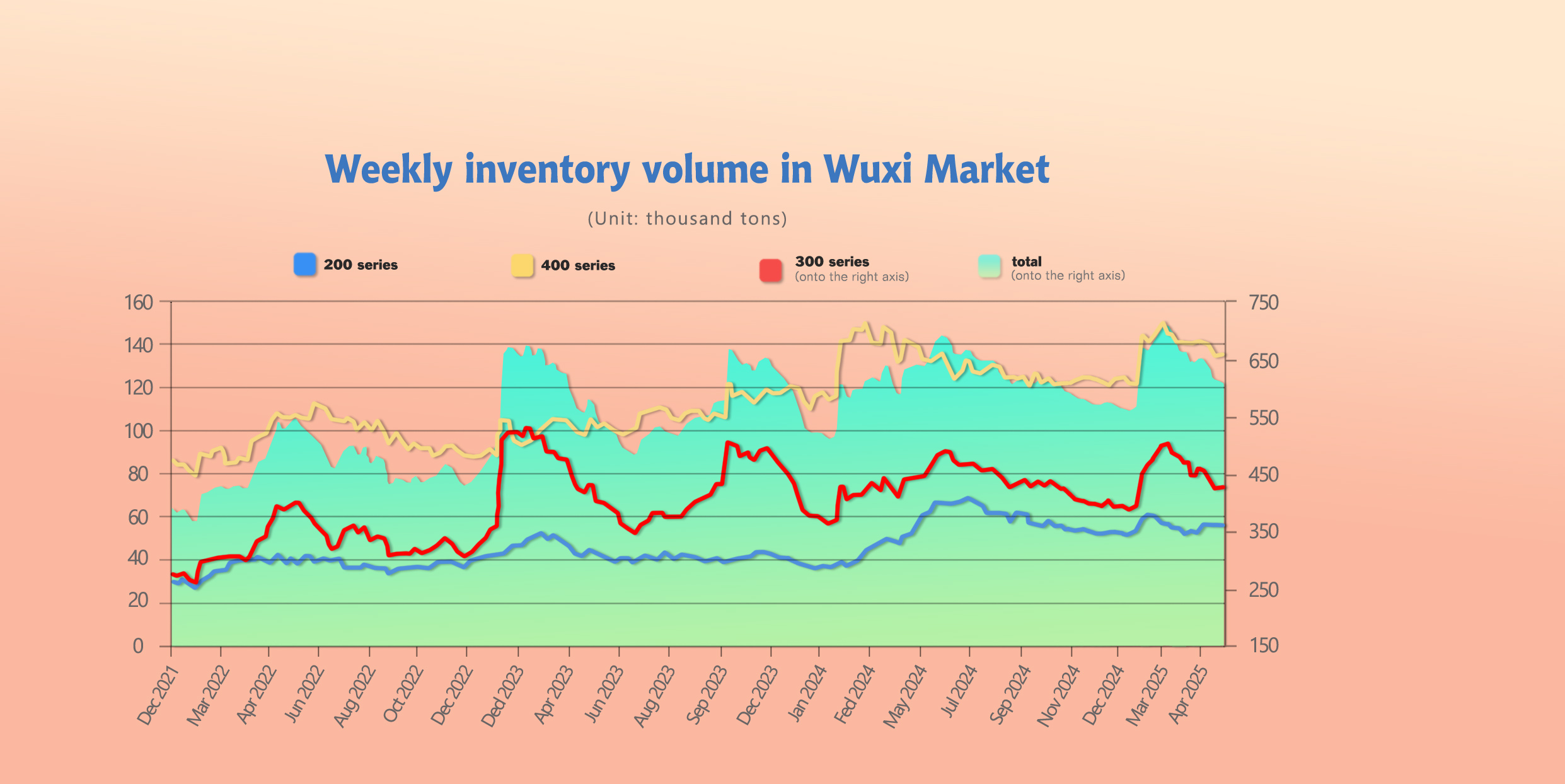

INVENTORY|| Market Optimism Drives a 4,300-Ton Stock Reduction

As of May 15th, total inventory in Wuxi sample warehouses decreased by 4,265 tons to 619,865 tons. Breakdown:

200 Series: 859 tons up to 58,114 tons.

300 Series: 2,604 tons down to 429,291 tons.

400 Series: 2,520 tons down to 132,460 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| May 8th | 57,255 | 431,895 | 134,980 | 624,130 |

| May 15th | 58,114 | 429,291 | 132,460 | 619,865 |

| Difference | 859 | -2,604 | -2,520 | -4,265 |

200 Series: Continued Arrivals Drive Inventory Build-Up

Last week, Resources from Baosteel Desheng, Zhoushan Hongwang, and other mills continued to arrive, maintaining supply-side pressure.

Steel mill price hikes and ongoing macro-level support have led to a more optimistic market sentiment. A slight inventory reduction is expected next week.

300 Series: Futures-Driven Price Rally Boosts Low-Price Inventory Clearance

Macroeconomic optimism and industry news, such as production shifts and firm pricing from mills, improved supply-demand dynamics. Downstream buyers showed stronger purchasing intent, and speculative restocking increased, resulting in a slight inventory drawdown.

400 Series: Increased Downstream Buying

Improved transactions led to continued inventory depletion in the spot market.

RAW MATERIAL || Improved Steel Mill Profitability

1. High-Nickel Pig Iron (NPI)

Last week, high-NPI transaction prices stabilized.

Driven by supportive macro policies, stainless steel prices surged during the week, prompting short-term price-holding sentiment among NPI suppliers. However, mills remain cautious in their raw material procurement.

With downstream demand recovering and production costs rising, a short-term price floor for high-NPI is likely to hold.

2. High-Carbon Ferrochrome

In the raw material market, high-carbon ferrochrome retail prices fell by another US$14, to US$1125-US$1153/50 reference ton.

Taigang and Tsingshan’s May procurement tender prices were US$1110-US$1138/50 reference ton, both up US$70 from the previous month.

Last week, high-carbon ferrochrome prices remained generally stable with a slight downward bias.

With major steel mills soon to announce June tenders, the market remains cautious. Although mills are pushing for lower prices and supply has increased, high ore prices are keeping factory price resistance strong.

As a result, the price floor for high-carbon ferrochrome appears firm, and the market is expected to remain stable in the short term.

MACRO || The Surge in Exports Reflects an Underlying Sense of Insecurity

Is the 90-Day Agreement Merely Borrowing from Future Demand?

On May 19, 2018, China and the United States also released a joint statement. However, just ten days later, on May 29, 2018, the U.S. government unilaterally overturned the consensus.

This lingering uncertainty about the future is what’s driving the current “rush to export” to the U.S. — a surge that is essentially front-loading future shipment volumes. The “strong present, weak expectations” dynamic is becoming even more apparent.

Applied to the ferrous metals market, the sharp increase in steel export expectations has also shifted what was an extremely pessimistic outlook. The price gap between hot-rolled and cold-rolled steel is now expected to narrow. However, the rebound in ferrous metal prices remains capped by export pricing levels, meaning there is limited upside.

Looking deeper into the data: even though tariffs have been reduced to some extent, the tariff rates for most industries still exceed 50%. while most industries’ profit margins are below 10%. This means that, relative to industry profitability, tariffs remain excessively high.

In some sectors, the imposed tariff rates exceed 60%, such as:

The automotive and auto parts industry,

The construction and engineering sector, and

The tobacco industry.

For industries related to black metals — including metal, non-metal, and mining — tariffs remain as high as 57.9%. And due to Section 232 measures, tariffs on Chinese steel exports to the U.S. are currently above 70%.

Looking ahead, there is potential for export growth to remain high from May through August. However, a key observation is that on May 14, the European shipping futures contracts (EU Line 2506 and 2508) hit their daily limit-up. The contracts within the 90-day agreement period saw sharp gains, while those beyond the agreement window saw limited increases. This reflects the market’s belief that tariff risks may return after the 90-day window ends.

The surge in exports — driven by the uncertainty surrounding future trade relations with the U.S. — is accelerating the depletion of future demand. The "strong reality, weak expectations" effect is increasingly pronounced.

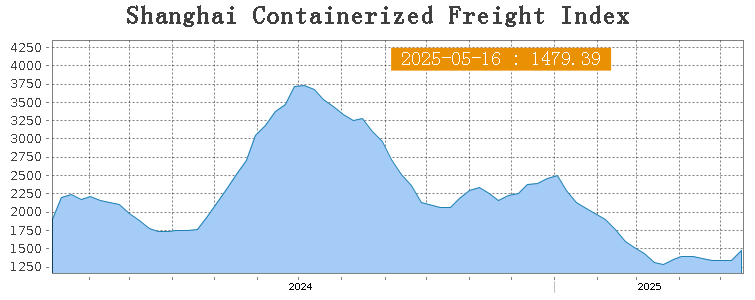

SEA FREIGHT || Shanghai–US West Coast Rates Surge by 31.7%

Last week, China’s container shipping export market received a significant boost from the positive news surrounding the "tariff war" resolution.

Last week, China’s container export shipping market remained generally stable, with slight fluctuations observed on some routes. On May 16th, the Shanghai Containerized Freight Index (SCFI) rose 10% to 1479.39 points.

Europe/ Mediterranean:

Transport demand on relevant trade lanes rebounded noticeably, with most long-haul routes seeing freight rates increase, pushing the composite index higher. However, the outlook for U.S.–EU trade negotiations remains unclear, and the prospects for Europe’s economic recovery still face considerable uncertainty. Last week, overall transport demand remained stable on European routes, with freight rates experiencing a slight decline.

On May 16th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1154/TEU, which decreased by 0.6%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$2082/TEU, which fell 0.3% from previous week.

North America:

Following the 90-day tariff reduction agreement between China and the United States, U.S. companies have quickly restarted their supply chains, and importers are now racing to process previously backlogged orders. The market anticipates a surge in freight volumes over the coming weeks. Last week, shipping demand rebounded significantly, but the total capacity available has not yet returned to pre–trade war levels. Space remains tight, and spot booking rates have risen sharply.

On May 16th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$3091/FEU and US$4069/FEU, reporting 31.7% and 22% surge accordingly.

The Persian Gulf and the Red Sea:

On May 16th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf gain 4% to US$1191/TEU.

Australia&New Zealand:

On May 16th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand lost 4.4% to US$737/TEU.

South America:

On May 16th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports took a 17.2% hike to US$1725/TEU.

At present, carriers have begun implementing contingency measures by reallocating capacity from European, Middle Eastern, and Mediterranean routes back to U.S.-bound lanes. However, it will take at least 1 to 2 weeks for this capacity to be restored. This reallocation may subsequently drive up rates on routes like Europe and the Mediterranean as well, though the impact will depend on how carriers manage their overall fleet deployment.