Stainless Insights in China from August 4th to August 10th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,030 | 17 | 0.89% |

| Foshan | 2,075 | 17 | 0.87% | ||

| Hongwang | Wuxi | 1,935 | 7 | 0.39% | |

| Foshan | 1,940 | 11 | 0.62% | ||

| 304/NO.1 | ESS | Wuxi | 1,860 | 13 | 0.73% |

| Foshan | 1,870 | 10 | 0.56% | ||

| 316L/2B | TISCO | Wuxi | 3,660 | 53 | 1.53% |

| Foshan | 3,675 | 31 | 0.88% | ||

| 316L/NO.1 | ESS | Wuxi | 3,505 | 42 | 1.26% |

| Foshan | 3,515 | 52 | 1.56% | ||

| 201J1/2B | Hongwang | Wuxi | 1,225 | 8 | 0.76% |

| Foshan | 1,225 | 3 | 0.25% | ||

| J5/2B | Hongwang | Wuxi | 1,125 | 7 | 0.70% |

| Foshan | 1,125 | 3 | 0.28% | ||

| 430/2B | TISCO | Wuxi | 1,130 | 1 | 0.14% |

| Foshan | 1,125 | 0 | 0.00% |

TREND | Stainless Steel Supply Tightens, Prices Rise

Last week, stainless steel futures moved higher in a choppy trend, with moderate gains. As of the close on Friday, August 8, the most-traded September 2025 contract (2509) settled at US$1,940/MT, up US$20.3/MT from the previous week, representing a weekly gain of 1.13%. Overall, stainless steel prices maintained a firm trend during the week.

A wave of concentrated maintenance at steel mills has significantly eased supply pressures for the coming weeks, while downstream demand remains primarily driven by essential procurement. In the spot market, prices rose by US$7–28/MT last week. Social inventory pressure continued to ease, with spot availability remaining sufficient. Looking ahead, market attention will focus on actual demand recovery, mill production schedules, and raw material price fluctuations. Prices are expected to remain firm yet volatile in the near term.

300-Series: Improved Supply-Demand Balance, Faster Inventory Drawdown

The 304 market saw a modest price increase last week. As of Friday, mainstream prices for private 304 cold-rolled 4-foot coil in Wuxi stood at US$1,900/MT, up US$14/MT, while private hot-rolled prices reached US$1,870/MT, up US$21/MT.

•Tsingshan raised opening offers during the week, prompting agents to strengthen price support.

•Traders under Tsingshan’s umbrella also adjusted prices upward slightly, with Delong following suit, leaving few low-priced resources in the market.

•Macro sentiment softened, with downstream buyers cautious toward higher-priced cargoes, sticking mainly to essential purchases.

•Market arrivals fell noticeably, hot-rolled supply remained scarce, and inventory drawdown accelerated.

200-Series: Limited Supply, Low-End Prices Edge Higher

Last week, 201 prices generally increased. Both 201J1 and 201J2 cold-rolled products rose by US$7/MT, while 201J1 hot-rolled prices remained unchanged.

•Early in the week, 201J2 cold-rolled shipments clustered around US$1,095/MT, with downstream buyers resistant to higher prices, resulting in average transactions.

•As futures prices climbed, low-end offers also rose by Friday.

•Raw material shortages limited arrivals, and subsequent price rises improved transaction volumes, supporting faster inventory drawdown.

400-Series: Stable Demand, 430 Prices Slightly Up

The 430 market gained US$7/MT last week. In Wuxi:

•State-owned 430 cold-rolled offers were quoted at US$1,135–1,145/MT

•State-owned 430 hot-rolled prices remained steady at US$1,040/MT

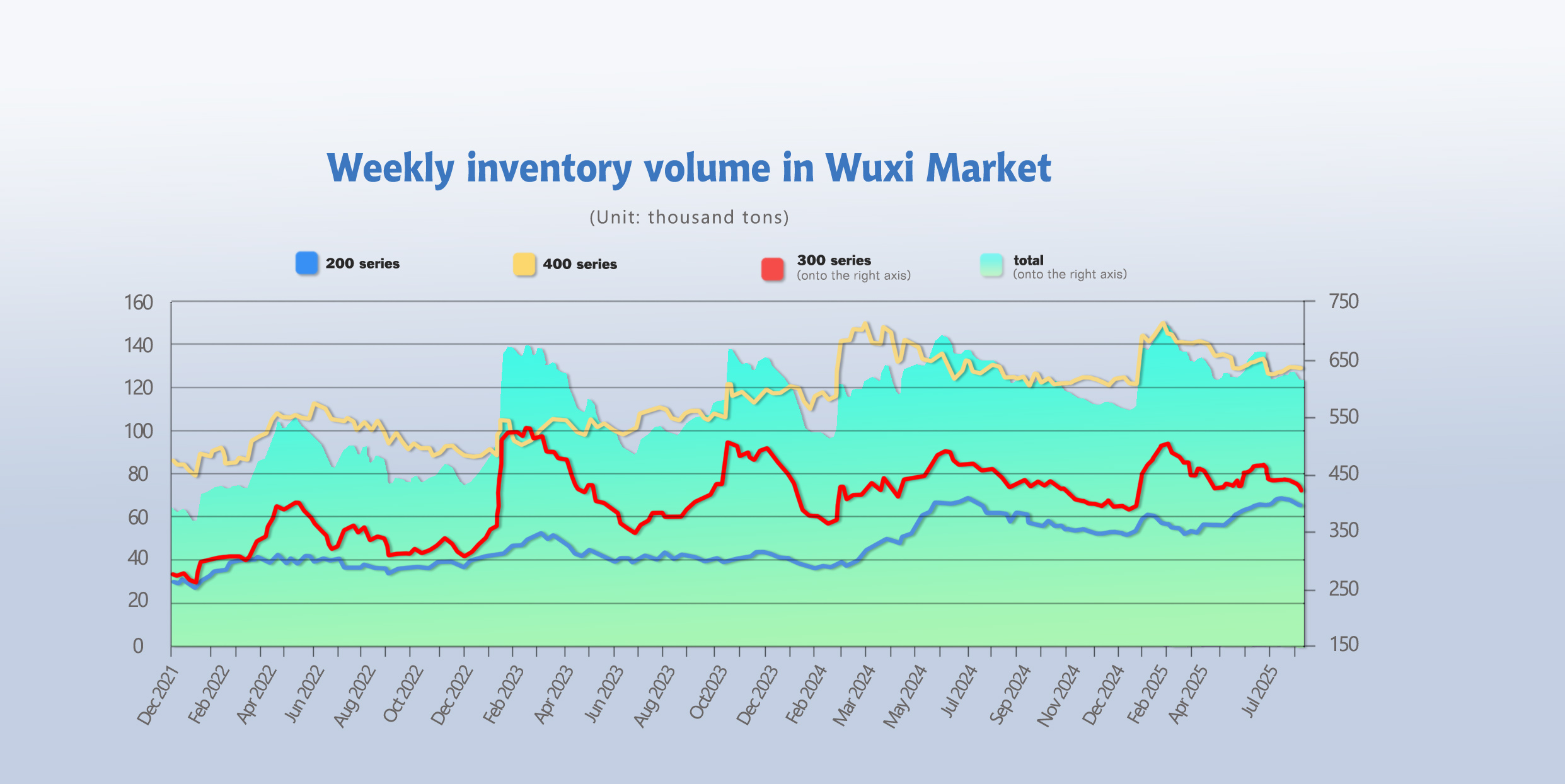

INVENTORY | Output Cuts of 210,000 Tons Tighten Market Supply

As of August 7, total inventory in Wuxi sample warehouses decreased by 16,236 tons, reaching 604,537 tons.

Inventory Breakdown:

•200 Series: 63,777 tons, down 1,324 tons

•300 Series: 412,494 tons, down 15,192 tons

•400 Series: 128,266 tons, up 280 tons

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Jul 31st | 65,101 | 427,686 | 127,986 | 620,773 |

| Aug 7th | 63,777 | 412,494 | 128,266 | 604,537 |

| Difference | -1,324 | -15,192 | 280 | -16,236 |

300-Series: Output Cuts Accelerate Destocking

Futures prices rebounded after recent lows, with spot agents and traders more willing to hold prices. Downstream buyers increased purchases on dips. With supply pressures easing, rising raw material costs, and improving macro sentiment, demand gradually picked up, driving faster destocking.

200-Series: Purchasing Sentiment Improves

Arrivals from Zhoushan Hongwang decreased last week, easing market supply pressures.

400-Series: Higher Cold-Rolled Arrivals Slightly Lift Inventories

•JISCO cold-rolled stocks increased

•TISCO cold-rolled stocks fell sharply

•Hot-rolled stocks declined slightly overall, leading to a minor net inventory increase

Factors: Higher mill deliveries and a slight slowdown in market transactions.

Outlook:

•Gradual price recovery has stimulated downstream buying interest.

•Mill production cuts reduce supply, accelerating inventory drawdown.

•Multiple mills have announced intensive production cut or suspension plans.

•Last week, stainless steel registered warehouse receipts fell by 3 tons, totaling 102,983 tons.

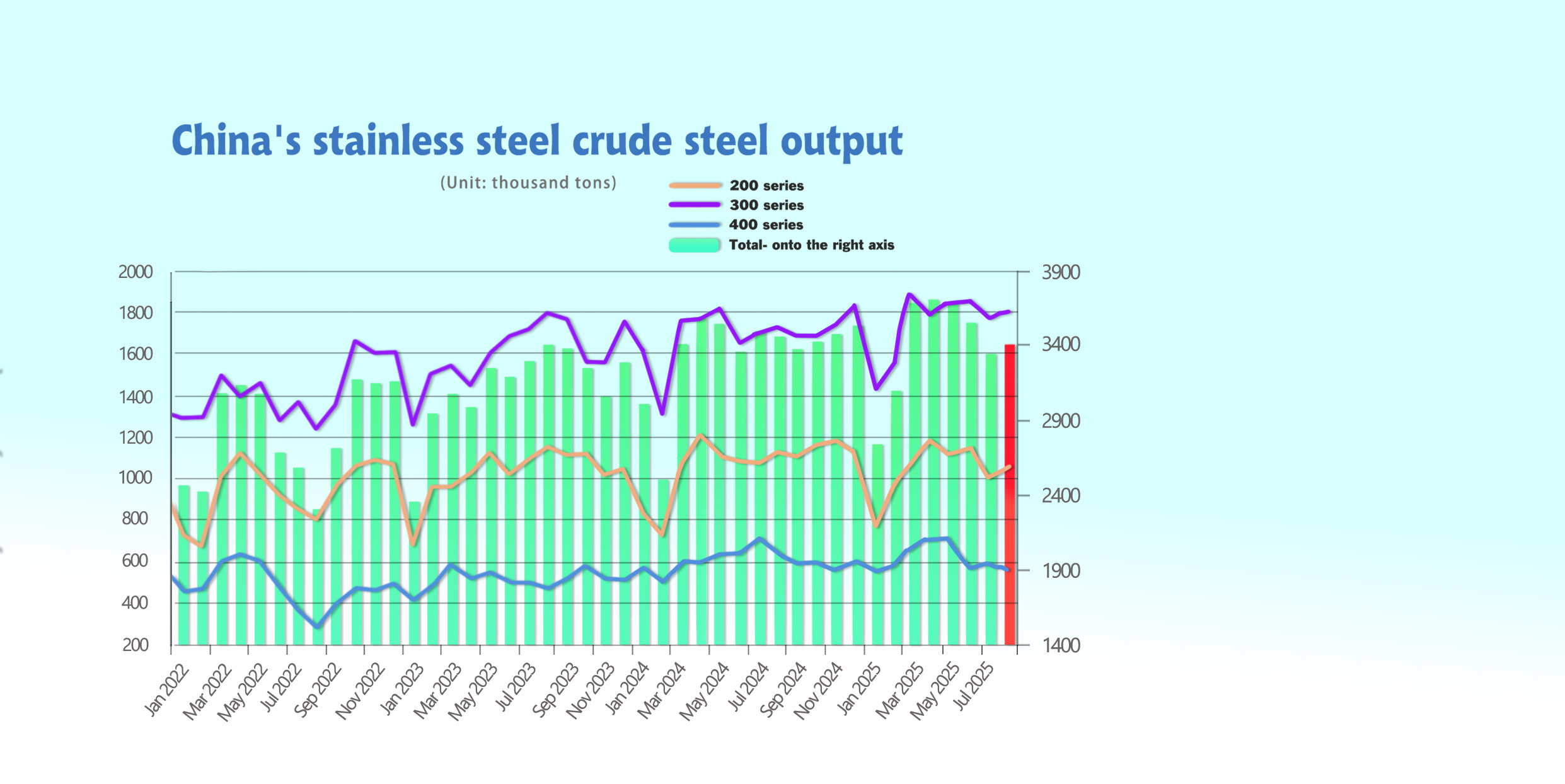

July Crude Stainless Steel Output

Weak terminal demand and high inventories pushed 304 cold-rolled spot prices down to US$1,845/MT, the lowest in nearly five years.

•July 2025 crude stainless steel output: 3.35 million tons, down 210,000 tons MoM and 121,800 tons YoY

Output by Series:

•200 Series: 993,200 tons, -13.38% MoM, -7.07% YoY

•300 Series: 1.7706 million tons, -3.87% MoM, +4.75% YoY

•400 Series: 585,600 tons, +2.57% MoM, -17.76% YoY

Drivers:

•300-Series: Weak June orders; Tsingshan and Xin Hai maintained low output (-70,000 tons MoM)

•200-Series: Price declines deepened mill losses; Tsingshan and Desheng cut output; Jin Hai and Beigang New Materials maintained low production due to maintenance/low-carbon upgrades

•400-Series: Seasonal weakness offset by small production adjustments

August Output Forecast

China’s crude stainless steel output is expected to increase 57,000 tons MoM to approximately 3.41 million tons:

•300 Series: +28,000 tons → 1.8 million tons

•200 Series: +60,000 tons → 1.05 million tons

•400 Series: -30,000 tons → 550,000 tons

Drivers:

•Policy: “Anti-involution” capacity-cut targets

•Events: Northern mills’ maintenance for September military parade

•Demand: Gradual recovery; high temperatures/heavy rainfall affect downstream industries

•Key mills’ reductions: Jiangsu D Steel (-30–40k), East China L Steel (-20k), East China S Steel (capacity-constrained)

Price Outlook: Futures and spot prices likely to remain range-bound with upward bias, with market participants monitoring mill maintenance and restocking pace closely.

SUMMARY | Supply Contraction Strengthens, Prices Remain Volatile

•300-Series: Prices fluctuate, driven by policy changes. Downstream buyers maintain rigid-demand purchases. Reduced production improves supply-demand balance. Infrastructure investment and inconsistent “anti-involution” policies create mixed sentiment. Spot prices expected to align with futures in short term.

•200-Series: Slight increase in output adds supply pressure, but positive macro outlook supports market optimism. 201 prices expected stable to slightly stronger.

•400-Series: Retail prices for high-chrome raw materials stable; Taigang and Tsingshan procurement prices declined slightly, still supporting 400-Series. 430 prices expected mostly stable.

MACRO | EU Stainless Steel Imports from Indonesia Hit Record High

As of August 10, 2025, Eurostat data shows EU imports of Indonesian stainless steel slabs likely to exceed 240,000 tons in 2025 — a historical record.

•2019 baseline: Hot-rolled coil imports from Indonesia <13,000 tons, with anti-dumping/anti-subsidy measures.

•Current paradox: EU mills buy large quantities of cheap slabs while advocating anti-dumping measures.

Factors:

1.Cost Advantage:

◦Abundant nickel resources, lower coal and electricity costs

◦Tariff evasion via re-export/semi-finished processing

2.Insufficient Domestic Capacity:

◦Energy costs, CBAM compliance, limited domestic production

◦Demand recovery in automotive & machinery sectors

3.Policy Loopholes:

◦Lower slab tariffs, simple processing circumvents restrictions

◦Domestic double standards: lobbying vs. bulk purchasing

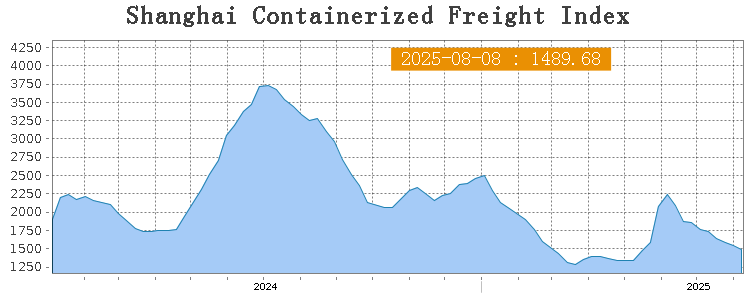

SEA FREIGHT | Stable Market, Most Route Rates Decline

China Exports: July 2025 grew 7.2% YoY in USD terms, maintaining momentum.

•Shanghai Containerized Freight Index (SCFI) fell 3.9% to 1,489.68 points on August 8.

Regional Freight Trends:

•Europe/Mediterranean: Shanghai → Europe: US$1,961/TEU (-4.4%); Shanghai → Mediterranean: US$2,318/TEU (-0.6%)

•North America: Shanghai → US West: US$1,823/FEU (-9.8%); Shanghai → US East: US$2,792/FEU (-10.7%)

•Persian Gulf/Red Sea: Shanghai → PG/RS: US$1,233/TEU (+6.9%)

•Australia & New Zealand: Shanghai → ANZ: US$1,197/TEU (+6.8%)

•South America: Shanghai → SA: US$3,811/TEU (-18.3%), impacted by Brazil tariffs up to 50%

Trade Shift: EU now China’s second-largest trading partner, bilateral trade 3.35 trillion yuan (+3.9% YoY), accounting for 13% of China’s total foreign trade. Export shift from the U.S. to EU drives greater competitive pressures.