Stainless Insights in China from August 11th to August 15th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,055 | 27 | 1.40% |

| Foshan | 2,100 | 27 | 1.36% | ||

| Hongwang | Wuxi | 1,960 | 29 | 1.62% | |

| Foshan | 1,960 | 22 | 1.23% | ||

| 304/NO.1 | ESS | Wuxi | 1,880 | 21 | 1.21% |

| Foshan | 1,890 | 20 | 1.12% | ||

| 316L/2B | TISCO | Wuxi | 3,690 | 28 | 0.79% |

| Foshan | 3,720 | 42 | 1.19% | ||

| 316L/NO.1 | ESS | Wuxi | 3,540 | 36 | 1.08% |

| Foshan | 3,560 | 42 | 1.24% | ||

| 201J1/2B | Hongwang | Wuxi | 1,240 | 18 | 1.64% |

| Foshan | 1,250 | 24 | 2.14% | ||

| J5/2B | Hongwang | Wuxi | 1,145 | 18 | 1.80% |

| Foshan | 1,150 | 24 | 2.35% | ||

| 430/2B | TISCO | Wuxi | 1,150 | 20 | 1.93% |

| Foshan | 1,135 | 10 | 0.97% |

Trend | Stainless Steel Futures Surge then Retreat, Market Cautiousness Intensifies

Stainless steel futures prices surged early last week before retreating. On last Monday, stainless steel futures rallied sharply with heavy volume, breaking above previous highs, but gradually declined in the following days. Trading remained active throughout the week, with open interest continuing to rise, though market divergence increased at higher price levels. Entering August, much of the earlier rally had been driven by expectations, with sentiment already released, and now the focus shifts to the actual implementation of policies. The supply-demand imbalance in stainless steel has eased somewhat, but whether prices can sustain strength will depend on upcoming steel mill production schedules. Last week, the main stainless steel futures contract settled at US$1945/MT, up 0.19% week-on-week, stainless steel prices rose by US$7-US$28/MT.

300 Series: Futures and Spot Prices Diverge, Inventory Depletes Faster

Last week, 304 prices saw a modest increase. By last Friday, mainstream private 304 cold-rolled four-foot base prices in Wuxi reached US$1915/MT, up US$21/MT from last week, while private hot-rolled stood at US$1880/MT, up US$14/MT. Early in the week, most mills raised offers to secure orders, prompting agents to follow with higher quotes. Low-priced resources were withheld from sales, while downstream buyers remained cautious. With hot-rolled resources especially scarce, agents showed strong willingness to hold firm on prices. Meanwhile, arrivals to the market dropped sharply, with significant declines from Tsingshan and Delong, easing supply pressure and accelerating destocking. However, as futures prices edged lower later in the week, spot market transactions saw modest discounts, with end-users purchasing only on a need basis, slowing the pace of inventory drawdown.

200 Series: Prices Continue to Rise, but Buyers Turn Cautious

Last week, 201 prices maintained an upward trend. Both 201J1 and J2 cold-rolled prices increased by US$14/MT, while 201J1 hot-rolled prices also rose by US$14/MT. The slight rise in hot-rolled prices drove some downstream restocking, though overall transaction volumes remained limited. At the start of the week, futures edged higher, lifting confidence in the spot market, with high-end offers probing near US$1125/MT and trading sentiment more active. However, as futures turned from gains to losses in the second half of the week, downstream buyers shifted back to a wait-and-see stance.

400 Series: Rising Costs and Slight Inventory Build Drive Prices Higher Before Stabilizing

Last week, mainstream high-chrome ex-factory quotations increased by US$14/MT to around US$1107-US$1136/50 reference ton, providing solid support for the 400 series. Producers raised prices consecutively. In the Wuxi spot market, state-owned 430 cold-rolled prices steadily increased by a cumulative US$21/MT, now quoted at around US$1165/MT, while state-owned 430 hot-rolled rose by US$7/MT to US$1045/MT.

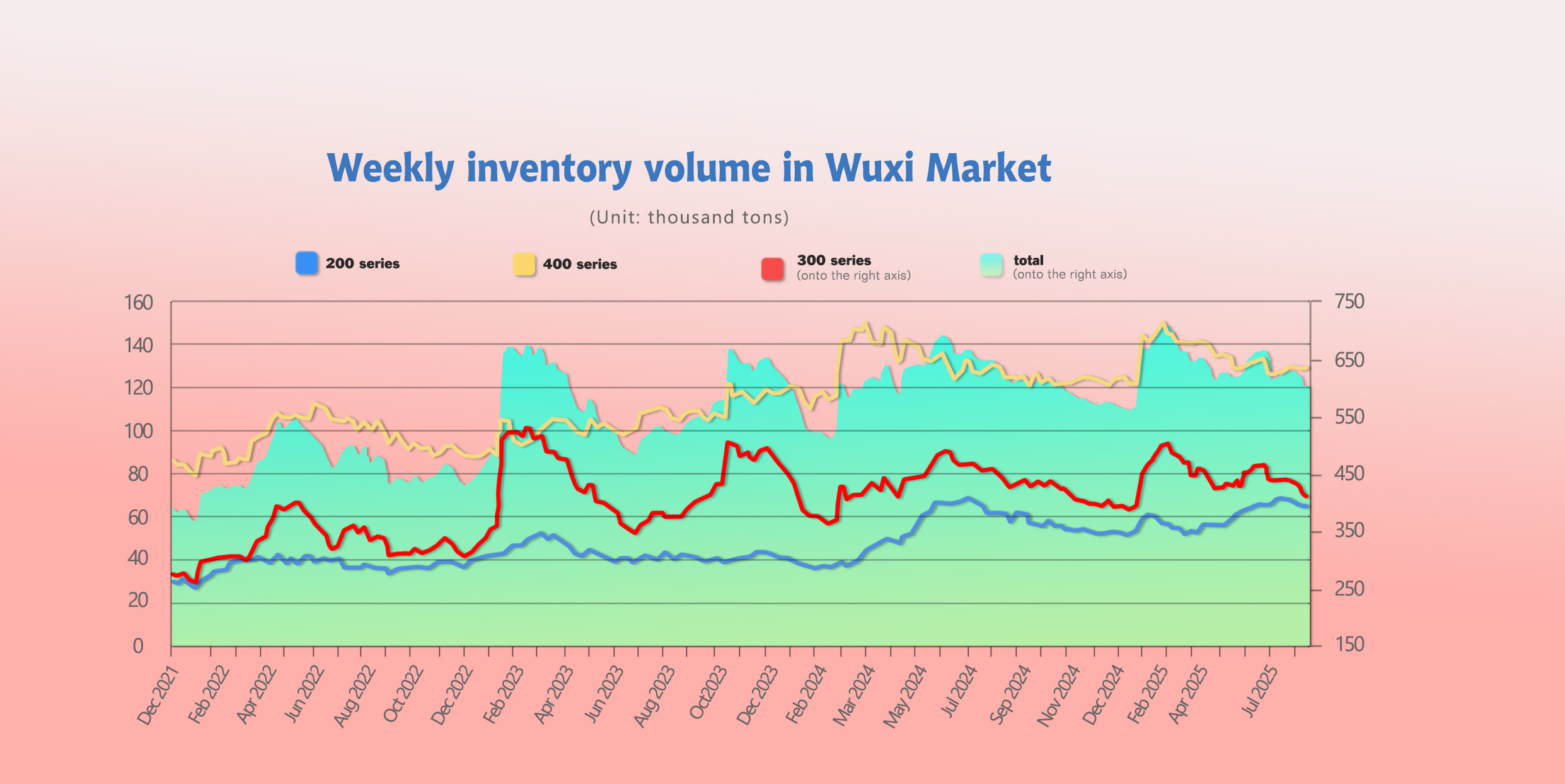

Inventory | Tight Supply of Hot-Rolled Stainless Steel

As of August 14th, total inventory in Wuxi sample warehouses decreased by 8,799 tons to 595,738 tons.

Breakdown:

•200 Series: 2,035 tons up to 65,812 tons.

•300 Series: 10,984 tons down to 401,510 tons.

•400 Series: 150 tons up to 128,416 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Aug 7th | 63,777 | 412,494 | 128,266 | 604,537 |

| Aug 14th | 65,812 | 401,510 | 128,416 | 595,738 |

| Difference | 2,035 | -10,984 | 150 | -8,799 |

300 Series: Inventory Continues to Decline, Hot-Rolled Supply Tightens

From the structure of spot inventory, both cold-rolled and hot-rolled arrivals decreased last week, leading to a clear decline in 300-series stocks and easing supply pressure. With Delong and TISCO production remaining at low levels, hot-rolled arrivals fell, and 304 hot-rolled inventory declined more sharply than cold-rolled. Currently, as macroeconomic frictions intensify at home and abroad, and with more production cuts at steel mills, supply pressure has eased. With prices moving higher, speculative demand has emerged, and inventories continue to decline. As peak season approaches, fundamentals are gradually improving, and inventories are expected to continue falling. Close attention is needed on steel mill production and market consumption.

200 Series: Stronger Downstream Wait-and-See Sentiment, Slight Inventory Increase

Last week, spot prices continued to rise last week, but as futures turned from gains to losses, high-priced resources were difficult to move. In the short term, 201 prices are expected to remain stable, with focus on steel mill output trends and market transactions.

400 Series: Increase in Cold-Rolled Arrivals, Slight Inventory Build

From the structure of spot inventory, JISCO’s cold-rolled stock decreased slightly, while TISCO’s cold-rolled and hot-rolled inventories remained largely unchanged. However, a small increase in trader-held spot stocks led to a slight overall rise. Last week, arrivals from steel mills decreased, while downstream demand for 400-series stainless steel remained active. The pace of stock inflow and drawdown was relatively balanced.

Raw Material | Nickel and Chrome Prices Expected to Rise in August

On August 13, mainstream high-chrome ex-factory quotations increased by US$14/MT to around US$1107-US$1136/50 reference ton. Since the beginning of August, mainstream high-chrome quotations have cumulatively risen by US$28/50 reference ton. The upward momentum for high-chrome prices still comes from rising costs. Recently, the domestic chrome ore spot market has remained stable, while futures prices have shown a clear increase.

From early July to now, the overall production cost of high-chrome has increased by about US$16.8/50 reference ton, putting more pressure on high-chrome producers. Some producers with more traditional processes are once again facing losses. As a result, high-chrome producers have shown stronger price-supporting sentiment, and ex-factory quotations have increased significantly.

It is expected that as stainless steel output recovers in August, downstream demand for high-chrome will increase, and price support will strengthen. Given that high-chrome output has been climbing recently, market supply is not tight. In the short term, high-chrome prices are expected to remain steady with a firm tone.

Regarding nickel, domestic high-nickel pig iron output in July recorded a slight decline, with both nickel pig iron plants and steel mills reducing production. In July, macro sentiment improved, stainless steel prices stopped falling and rebounded, and nickel pig iron prices also stabilized. Coupled with a slight downward adjustment in nickel ore prices, domestic nickel pig iron production costs edged lower, but losses remained severe. Plants continued to operate at low capacity, and steel mills mainly relied on external procurement of nickel pig iron. With stainless steel prices continuing to rise in August, steel mills are increasing production, driving up demand for raw materials. Domestic high-nickel pig iron output is expected to increase slightly in August.

Summary | Centralized Maintenance at Steel Mills in August Supports Stainless Steel Prices

On the macro policy side, although many monetary policy incentives have already been introduced, the rollout of fiscal stimulus has been slow, with limited impact on the real economy. Market arrivals remain low, social inventories continue to decline, and pressure is easing. On the raw material side, rising prices are further supporting steel production costs, and steel mill profits have slightly narrowed. With steel mills conducting concentrated maintenance in August, short-term supply pressure is reduced, providing support for stainless steel prices. However, downstream demand remains focused on rigid needs, and traders have already replenished inventories earlier, leaving spot resources relatively sufficient. The extension of the tariff schedule between China and the U.S. temporarily eases tensions, but uncertainty remains the main concern for the market. Overall, close attention should be paid to steel mills’ production schedules, raw material prices, and the extent of recovery in downstream demand as the peak season approaches.

300 Series: Current Prices Fluctuate, Market Sentiment Tracks Policy Changes

Current 300-series prices are fluctuating repeatedly, with market sentiment tracking policy changes. Downstream buyers are purchasing only for low-price rigid demand. On the supply side, more steel mills are reducing production, easing supply pressure and improving the supply-demand balance. Infrastructure investments have boosted sentiment across related industries, while anti-“involution” policies fluctuate and overseas tariff measures emerge, intensifying the tug-of-war between bullish and bearish forces. In the short term, 304 cold-rolled and hot-rolled spot prices are expected to follow futures and fluctuate, with focus on market transactions and inventory digestion.

200 Series: Mixed Futures, Stable Spot Prices

Last week, futures showed mixed movements, and spot prices adjusted slightly. However, expectations of favorable macro policies continue to drive optimism. Crude steel output for the 200 series is set to increase slightly in August, which may add supply pressure later. In the short term, 201 prices are expected to remain stable.

400 Series: High-Chrome Retail Prices Rise, Supporting 400-Series Market

Last week, high-chrome retail prices rose another US$14/50 reference ton, providing support to the 400-series stainless steel market. Recently, 430 prices have continued to climb steadily at a gradual pace. On one hand, producers’ price-supporting sentiment has strengthened; on the other hand, market demand remains acceptable, further reinforcing price support. Next week, 430 prices are expected to stabilize.

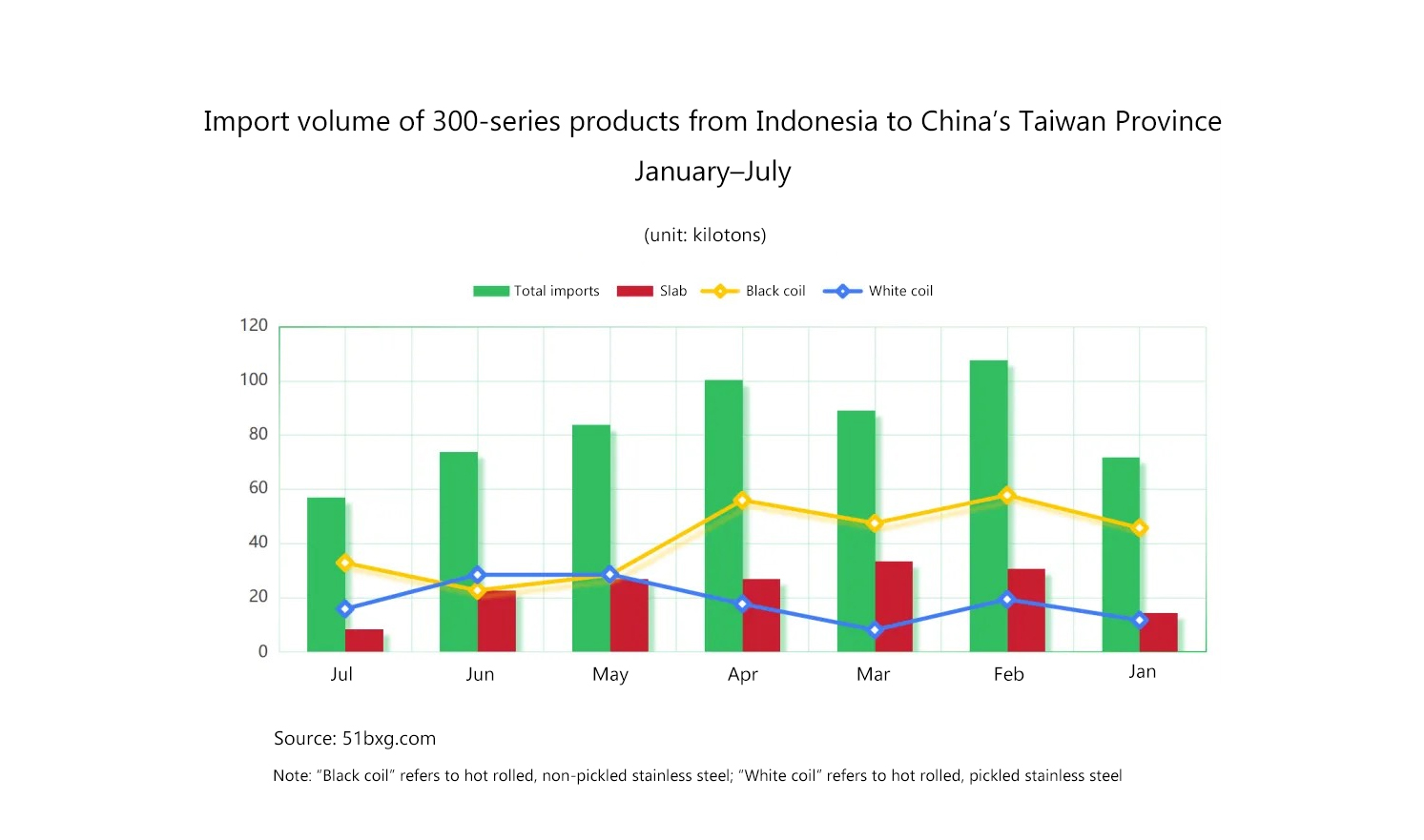

Macro | Taiwan’s July Imports from Indonesia Plunge 45.6% Year-on-Year

Indonesia Tsingshan’s July stainless steel exports to Taiwan hit a record low. On August 17, 2025, according to customs data, Indonesia’s exports of 300-series stainless steel products to Taiwan continued to decline in July 2025, mainly due to weak demand and intensifying structural contradictions.

Data showed that total imports in July were only 56,967 tons, down 22.7% from June (73,731 tons), and down 47.1% from the February peak (107,664 tons), remaining below the 100,000-ton level for the fifth consecutive month.

1. Data Analysis: Overall Contraction and Structural Shifts

Imports in July fell sharply by 45.6% compared with 104,718 tons in the same period last year, reflecting an accelerated demand decline.

•300-series black coil imports: 32,812 tons, down 43.6% from 58,131 tons last year, confirming intensified idle capacity at local mills.

•300-series slab imports: 15,787 tons, up 30.5% from 12,092 tons last year, but plunging 44.4% from June, showing severe volatility in substitution demand.

•300-series white coil imports: 8,368 tons, down 75.7% from 34,495 tons last year, hitting a historic low. Notably, the boom of monthly averages around 19,000 tons in the first half of the year also came to an abrupt end in July, with the share falling back to 27.7% (from 38.5% in June).

2. Three Main Reasons Behind Import Data

Industry sources pointed out three main reasons for the current import characteristics:

A. Futures-based model transmits production cuts

B. Direct sales disrupt agent system

C. Systemic collapse in manufacturing demand

Insights:

Indonesia Tsingshan’s 300-series stainless steel exports to Taiwan collapsed, mainly due to persistently weak demand in Taiwan and supply-demand imbalance. On the supply side, Tsingshan’s futures-based order system meant July arrivals reflected June orders, and June production cuts due to nickel volatility directly reduced July arrivals. Its direct sales model, bypassing agents and connecting with end-users, optimized its own channels but disrupted Taiwan’s procurement system, leading agents to cut purchases. Local mills’ procurement strategies became disordered, amplifying import volatility. With a cumulative increase of 70 USD/ton between July and August, September’s announced data, reflecting July orders, may show a different picture.

Indonesia Holds 60% of Global Nickel Supply, Key Force in Battery Raw Materials Market

According to foreign media reports on August 14, 2025, Macquarie released a report showing that Indonesia’s nickel product exports achieved a historic breakthrough—surpassing coal for the first time to become the country’s top export product. More importantly, by controlling about 60% of global nickel supply, Indonesia is consolidating its global influence in battery metals, with nickel being a core material for lithium batteries.

The report, authored by analysts including Jim Lennon, confirmed nickel’s “rise to the top”: in the first half of 2025, Indonesia’s overseas nickel sales revenue reached 16.5 billion USD, compared with 14.4 billion USD for coal, with nickel surpassing coal by 2.1 billion USD to become Indonesia’s largest foreign exchange earner.

The key driver behind this shift was Indonesia’s 2020 ban on ore exports. After the ban, Indonesia accelerated localized processing of nickel, with large-scale participation and leadership from Chinese enterprises in building smelters. This pushed Indonesia’s transformation from an “ore exporter” to a “processed goods exporter,” enabling it to quickly seize control of core links in the global nickel supply chain, ultimately achieving about 60% control of global supply.

Despite nickel price volatility, Indonesia’s nickel industry has shown resilience. Macquarie noted that nickel currently contributes 12% of Indonesia’s total export revenue. Although nickel prices on the London Metal Exchange have fallen 30% since peaking in June 2024, the significant increase in Indonesia’s nickel export volume has offset the impact of falling prices. In sharp contrast, Indonesia’s coal sector has cooled. Global oversupply has pushed coal prices down. Combined with China and India both expanding domestic coal production and accelerating renewable energy adoption, their import demand for Indonesian coal has weakened, further dragging down coal export performance.

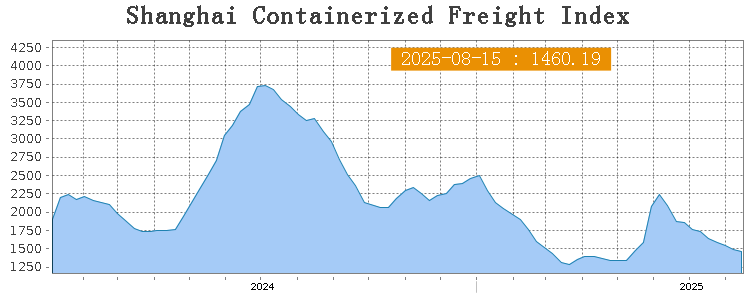

Sea Freight | Market Remains Stable, Most Route Rates Decline

Last week, China’s export container shipping market continued to adjust, with freight rates on most routes declining, dragging down the overall index. On August 15th, the Shanghai Containerized Freight Index (SCFI) fell 2% to 1460.19 points.

Europe / Mediterranean

Last week, transport demand lacked further growth momentum, and spot booking prices continued to fall. On August 15th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1820/TEU, which decreased by 7.2%. The freight rate for exports from Shanghai Port to the Mediterranean major ports market was US$2279/TEU, which dipped 1.7% from the previous week.

North America

Last week, the market supply–demand fundamentals appeared slightly weak, and the shipping market continued to adjust. Last week, transport demand continued to lack upward momentum, and freight rates in most trade lanes adjusted downward. On August 15th, the freight rates for exports from Shanghai Port to the US West and US East major ports were US$1759/FEU and US$2719/FEU, reporting 3.5% and 2.6% slide accordingly.

The Persian Gulf and the Red Sea

On August 15th, the freight rate exported from Shanghai Port to the major ports of the Persian Gulf gained 12% to US$1381/TEU.

Australia & New Zealand

On August 15th, the freight rate for exports from Shanghai Port to the major ports of Australia and New Zealand gained 3.5% to US$1239/TEU.

South America

On August 15th, the freight rate for exports from Shanghai Port to South American major ports decreased by 12.4% to US$3340/TEU.