Stainless Insights in China from July 21th to July 27th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,020 | 17 | 0.90% |

| Foshan | 2,060 | 17 | 0.88% | ||

| Hongwang | Wuxi | 1,930 | 25 | 1.42% | |

| Foshan | 1,935 | 18 | 1.02% | ||

| 304/NO.1 | ESS | Wuxi | 1,845 | 24 | 1.40% |

| Foshan | 1,860 | 17 | 0.98% | ||

| 316L/2B | TISCO | Wuxi | 3,550 | 20 | 0.58% |

| Foshan | 3,620 | 14 | 0.41% | ||

| 316L/NO.1 | ESS | Wuxi | 3,410 | 31 | 0.95% |

| Foshan | 3,420 | 18 | 0.56% | ||

| 201J1/2B | Hongwang | Wuxi | 1,210 | 31 | 2.91% |

| Foshan | 1,220 | 25 | 2.34% | ||

| J5/2B | Hongwang | Wuxi | 1,110 | 34 | 3.51% |

| Foshan | 1,120 | 25 | 2.58% | ||

| 430/2B | TISCO | Wuxi | 1,125 | 8 | 0.84% |

| Foshan | 1,115 | 6 | 0.56% |

Stainless Steel Market Weekly Brief | Prices Firm on Policy Optimism Amid Supply Overhang

Executive Summary

Driven by macroeconomic stimulus and improving sentiment in the bulk commodity market, stainless steel prices firmed across futures and spot segments last week. However, with fundamental oversupply still unresolved, the sustainability of this uptrend will hinge on production cutbacks and downstream demand recovery.

Stainless Steel Futures Gain as Market Sentiment Improves

The main stainless steel futures contract closed at US$1,950/MT, up 2.4% on the week, hitting an intraweek high of US$1,955/MT. Spot prices also edged up by US$21–28/MT, underpinned by policy tailwinds and speculative buying. Despite the upbeat sentiment, oversupply of stainless steel raw materials remains a constraint on further upside.

300 Series: Sentiment-Driven Gains, But Supply Pressure Persists

•Cold-rolled 304 stainless steel coils were quoted at US$1,890/MT, and hot-rolled at US$1,850/MT, each up US$28/MT.

•Infrastructure stimulus and speculative activity fueled short-term demand.

•However, as arrivals stabilized and inventory pressure resurfaced, late-week trading softened, reflecting a fragile supply-demand balance.

Insight: Unless mill production is meaningfully reduced, the rebound in 300-series stainless steel could lose steam. Spot market resilience will depend on real consumption—not sentiment alone.

200 Series: Prices Rise, Inventory Draws Moderately

•201J2 Cold-Rolled: ↑ US$35/MT to US$1,085/MT

•201J1 Cold-Rolled: ↑ US$28/MT to US$1,185/MT

•201J1 Hot-Rolled: ↑ US$28/MT to US$1,155/MT

Improved macro outlook supported price hikes. However, with downstream buyers resisting higher costs, trading momentum cooled midweek. Cold-rolled inventory drawdowns remain modest, leaving room for further adjustment.

400 Series: 430 Prices Tick Up, But Inventory Grows

•430 Cold-Rolled: ↑ US$7/MT to US$1,125–1,135/MT

•Hot-Rolled: Flat at US$1,040/MT

Steady end-user demand and limited downstream flexibility kept price movement mild. However, increasing mill shipments contributed to rising inventory, signaling ongoing supply pressure.

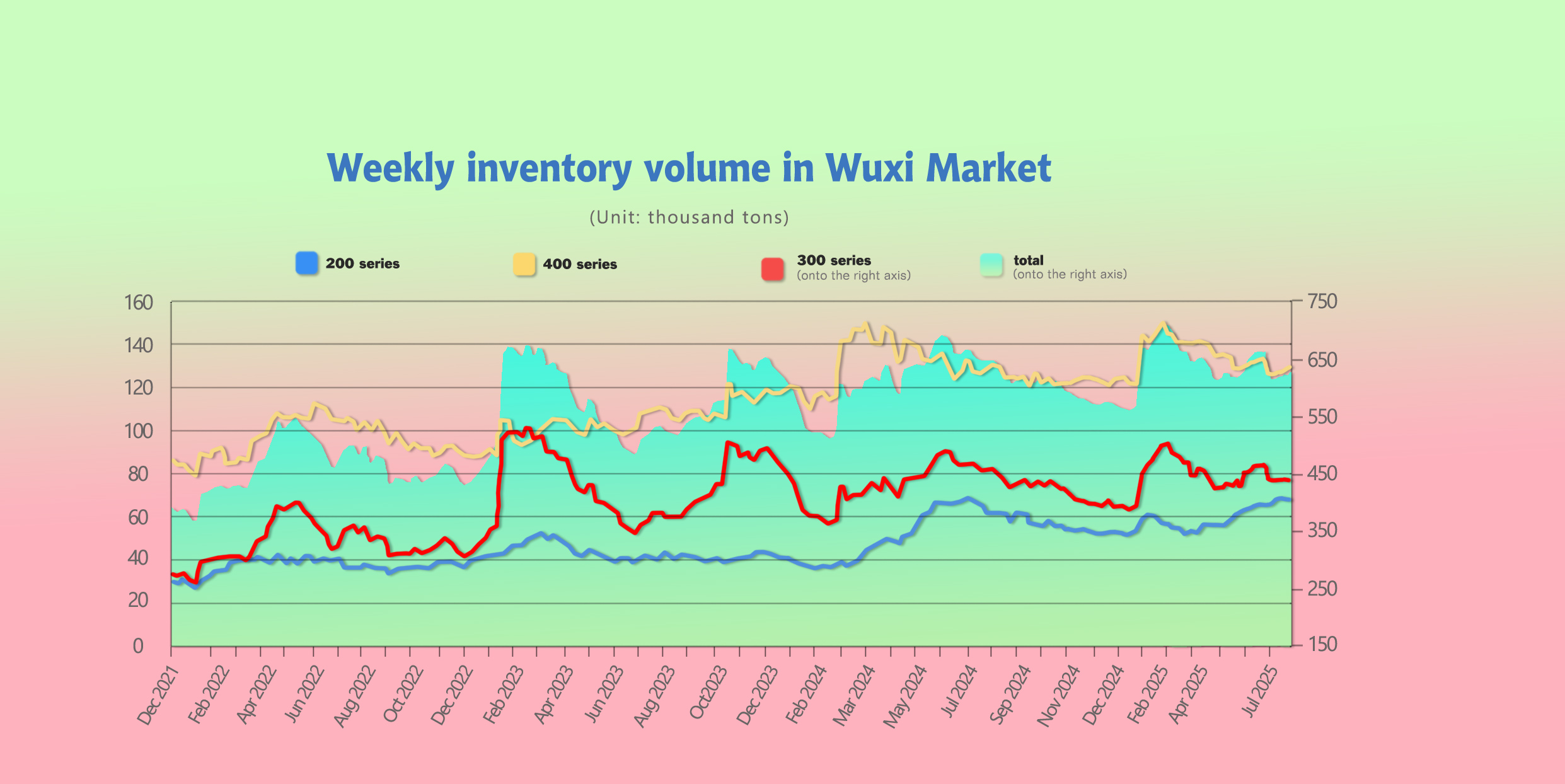

Inventory Trends | Wuxi Warehouse Stock Climbs

As of July 24, total inventory in Wuxi rose by 3,967 tons to 633,453 tons, with increases across all major series:

•200 Series: +449 tons → 67,910 tons

•300 Series: +1,549 tons → 436,119 tons

•400 Series: +1,969 tons → 129,424 tons

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

|

Jul 17th |

67,461 | 434,570 | 127,455 | 629,486 |

| Jul 24th | 67,910 | 436,119 | 129,424 | 633,453 |

| Difference | 449 | 1,549 | 1,969 | 3,967 |

Despite favorable policy conditions, inventory buildup suggests structural oversupply. Output control and demand recovery will be critical to reversing this trend.

Supply Update | Maintenance in Indonesia Impacts Cold-Rolled Output

•Acerinox Indonesia’s maintenance shutdown since May will continue through August, slashing 304 cold-rolled stainless steel supply by over 150,000 tons.

•Chinese imports of wide-width cold-rolled stainless coils from Indonesia dropped significantly in May–June, easing competitive pressure.

Raw Material Snapshot | Nickel Pig Iron Rallies on Mill Demand

•High-grade NPI rose to US$128/nickel point, up US$0.7 WoW

•SHFE Nickel gained US$630/MT to US$17,490/MT (+3.74%)

•Ferrochrome prices remained stable, but major mills trimmed August procurement prices:

◦TISCO: ↓ US$28/MT

◦Tsingshan: ↓ US$21/MT

Despite firm stainless steel coil prices, raw material oversupply—especially domestically—limits room for further cost inflation.

Export Update | Tariffs and Trade Friction Pressure China’s Stainless Steel Exports

•June stainless steel exports: 390,000 tons, down 10.6% MoM / 13.9% YoY

•Net exports: Down 9.9% MoM, but +33% YoY for H1

With tightening international trade policies, including potential U.S. tariff hikes, Chinese stainless steel coil exports may face further headwinds. JINLING METALS and other exporters should monitor trade policy shifts closely.

Global Market Watch | Crude Steel Output Down 5.8% in June

According to the World Steel Association, global crude steel production in June fell to 151.4 million tons, down 5.8% YoY.

Notable shifts include:

•China: ↓ 9.2% to 83.18 Mt

•India: ↑ 13.3% to 13.6 Mt

•Germany: ↓ 15.9% to 2.7 Mt

This reflects continued structural realignment in global steel supply.

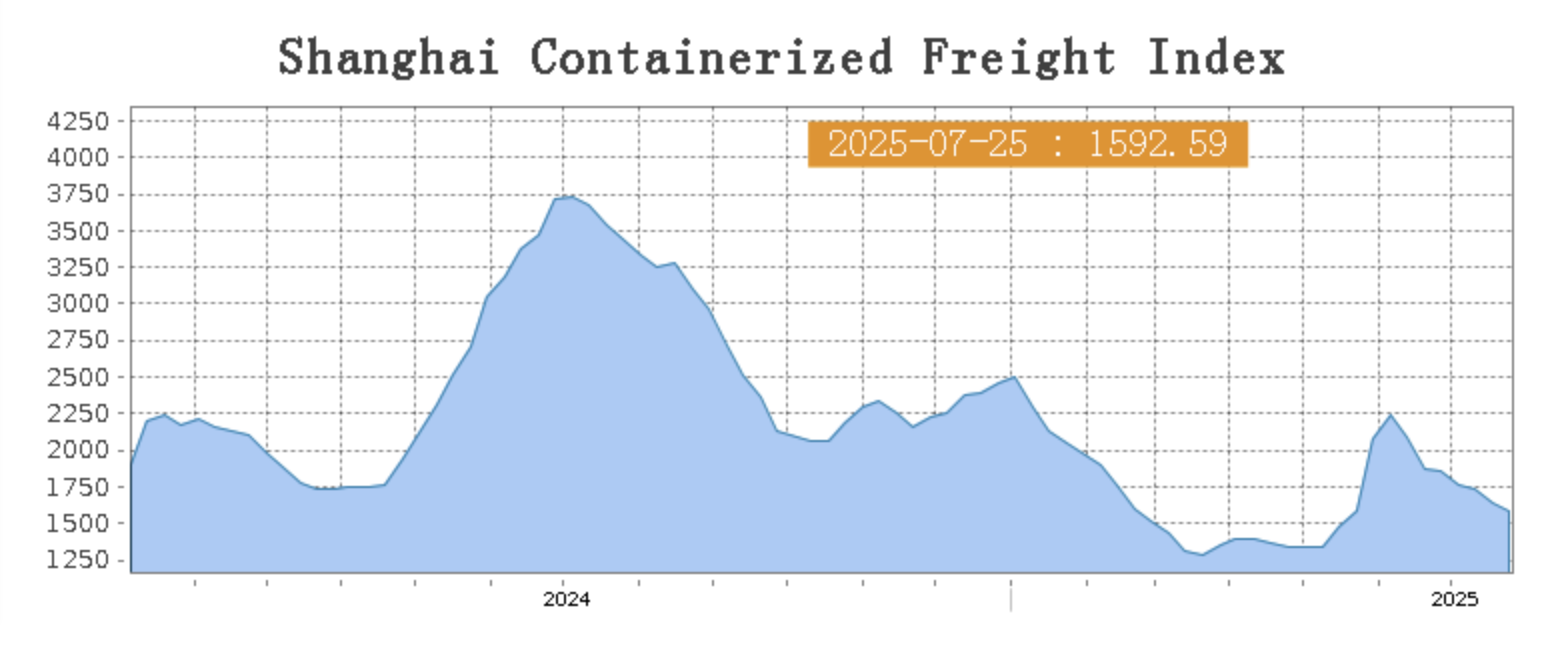

Freight Market | Shipping Costs Continue to Soften

On July 25, the Shanghai Containerized Freight Index (SCFI) fell 3.3% to 1,592.59.

Most trade lanes posted declines:

•Europe: +0.9% to US$2,090/TEU

•Mediterranean: ↓ 4.4% to US$2418/TEU

•US West Coasts: ↓ 3.5% to US$2067/FEU

•US East Coasts: ↓ 6.5% to US$3378/FEU

•Persian Gulf: ↓ 12.8% to US$1152/TEU

•South America: ↓ 7.8% to US$5188/TEU

•Australia/NZ: +2.8% to US$1071/TEU

Soft freight rates may ease export costs, but they also reflect subdued global demand for stainless steel raw materials and finished steel products.

Strategic Outlook | Market to Remain Firm But Volatile in Short Term

Despite short-term strength in stainless steel prices, uncertainty remains. Key market drivers include:

•Mill production cuts vs. oversupply dynamics

•Downstream demand elasticity

•Social warehouse destocking rates

•Global trade disruptions and tariffs