Stainless Insights in China from May 5th to May 11th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,045 | 9 | 0.49% |

| Foshan | 2,090 | 9 | 0.48% | ||

| Hongwang | Wuxi | 1,940 | -2 | -0.13% | |

| Foshan | 1,960 | 0 | 0.00% | ||

| 304/NO.1 | ESS | Wuxi | 1,890 | 9 | 0.53% |

| Foshan | 1,890 | 5 | 0.30% | ||

| 316L/2B | TISCO | Wuxi | 3,455 | 21 | 0.64% |

| Foshan | 3,540 | 12 | 0.34% | ||

| 316L/NO.1 | ESS | Wuxi | 3,330 | 26 | 0.81% |

| Foshan | 3,355 | 4 | 0.11% | ||

| 201J1/2B | Hongwang | Wuxi | 1,240 | 0 | 0.00% |

| Foshan | 1,225 | 0 | 0.00% | ||

| J5/2B | Hongwang | Wuxi | 1,130 | -8 | -0.75% |

| Foshan | 1,125 | 0 | 0.00% | ||

| 430/2B | TISCO | Wuxi | 1,160 | 0 | 0.00% |

| Foshan | 1,155 | 0 | 0.00% |

TREND || Market Confidence Remains Unstable

Last week, stainless steel spot prices in the Wuxi market remained stable. Futures prices fluctuated repeatedly under the influence of macroeconomic policies, while market confidence was weak, with most participants holding positions and adopting a wait-and-see approach. On the cost side, raw material price declines led to a slight cost reduction. Market arrivals continued, resulting in inventory accumulation. As of Friday, the main stainless steel futures contract price rose by US$7/MT compared to pre-holiday levels, reaching US$1910/MT—an increase of 0.39% for the week, with a weekly high of US$1925/MT.

300 Series: Trading Halted During Holiday, Inventory Shifted from Decline to Increase

Last week, the 304 spot market remained stable. As of Friday, the mainstream base price for privately-produced cold-rolled (four-foot) 304 in Wuxi was quoted at US$1900/MT, while the price for hot-rolled was at US$1890/MT—both unchanged from pre-holiday levels. Post-holiday, arrivals increased, while end-user buying interest remained low. Steel mills opened at steady prices, and overall trading sentiment was lukewarm. Although interest rate cuts and reserve requirement reductions by the central bank temporarily boosted sentiment, pushing futures prices up briefly, the rally was short-lived. Trading volume increased within the day, but consistent market arrivals before and after the holiday led to inventory accumulation throughout the week.

200 Series: Spot Prices Declined, Inventory Depletion Slowed

Last week, 201 prices trended mildly weaker. cold-rolled 201J2 was quoted at US$1095/MT, cold-rolled 201J1 at US$1210/MT, and hot-rolled 201J1 at US$1170/MT.

The market initially showed strength before turning weaker during the week. With trading paused over the holiday and steel mills continuing to deliver, supply-side pressure intensified. cold-rolled J2 traders made concessions of US$7/MT to secure sales, with quotes mainly around US$1095. Downstream buyers remained cautious, overall trading was moderate, and inventory saw a slight increase.

400 Series: Cost Support Still Present, Prices Remain Stable

Last week, 430 prices in the market ran weakly stable. In the Wuxi spot market, state-owned 430 cold-rolled was quoted steadily US$1160-US$1170/MT, while 430 hot-rolled remained at US$1085/MT—both unchanged from pre-holiday levels.

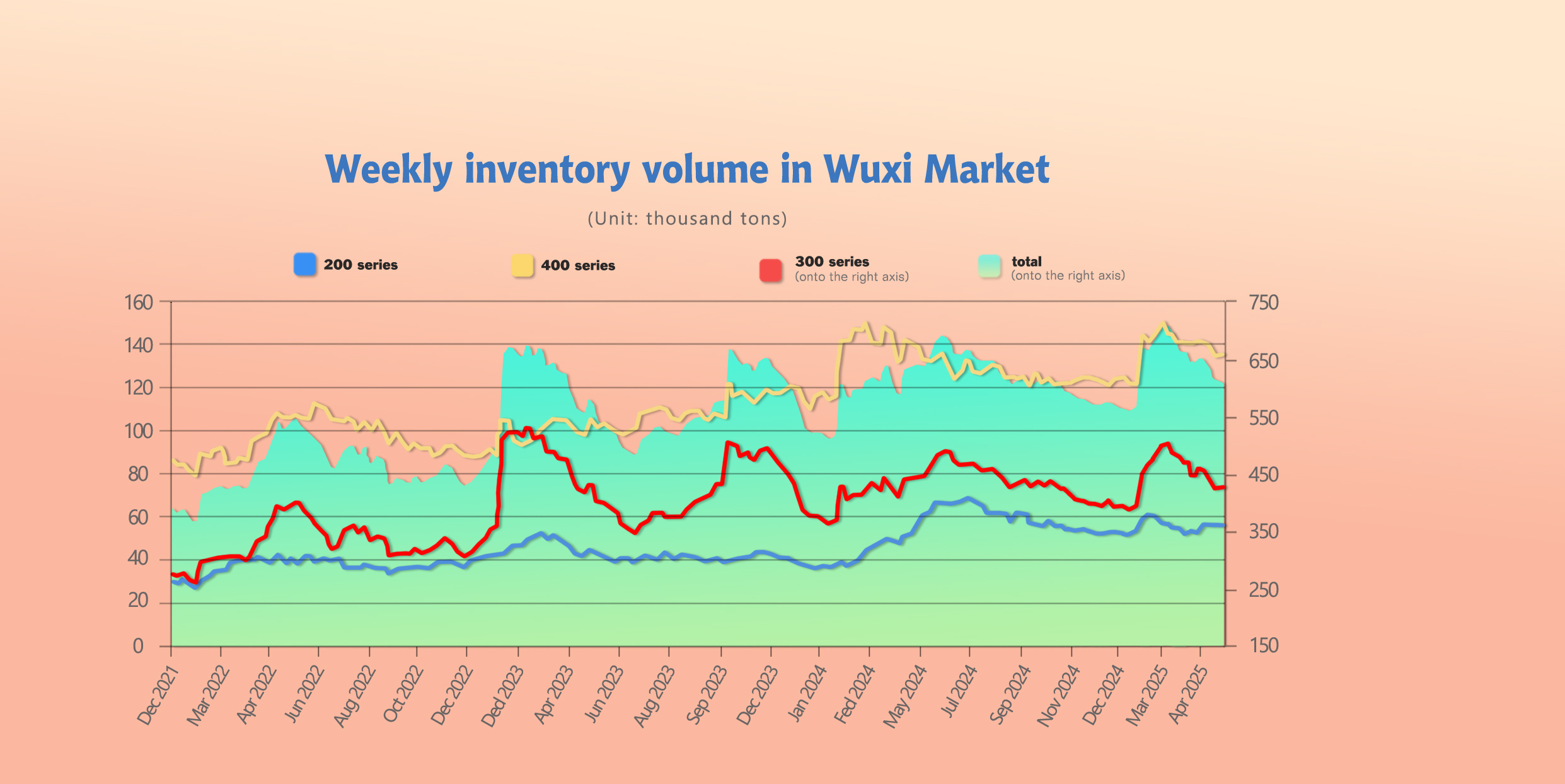

INVENTORY || Inventory Increased by 3.00%

As of May 8th, total inventory in Wuxi sample warehouses increased by 18,180 tons to 624,130 tons. Breakdown:

200 Series: 2,437 tons up to 57,255 tons.

300 Series: 13,443 tons up to 431,895 tons.

400 Series: 2,300 tons up to 134,980 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Apr 30th | 54,818 | 418,452 | 132,680 | 605,950 |

| May 8th | 57,255 | 431,895 | 134,980 | 624,130 |

| Difference | 2,437 | 13,443 | 2,300 | 18,180 |

200 Series: Slight Weakening in Demand

During the May Day holiday, trading activity came to a halt while deliveries from steel mills continued, increasing the volume of available resources in the market.

With macroeconomic positives such as reserve requirement and interest rate cuts and China-U.S. dialogues unfolding, market confidence saw some support. Transaction activity may improve next week, and a slight inventory reduction in 201 is expected. Market attention will remain on mill pricing and trading dynamics.

300 Series: Trading Halted During Holiday, Inventory Significantly Increased

Trading was stagnant during the holiday, while arrivals remained normal. The weak supply-demand structure persisted, shifting inventories from decline to growth.

Though reserve and rate cut policies have helped lift sentiment, the overcapacity issue remains unresolved. The contradiction between strong expectations and weak reality is intensifying. Downstream terminals mostly continue with just-in-time purchasing, speculative demand remains subdued, and inventory build-up is significant.

400 Series: Slower Downstream Purchasing

In terms of spot inventory structure, there was a noticeable influx of JISCO cold-rolled arrivals last week, and both TISCO cold-rolled and hot-rolled inventories also saw increases. Overall, spot inventory showed a significant uptick.

RAW MATERIAL || Cost Pressure Forces Nickel and Chrome Prices Down

NICKEL: Nickel Pig Iron Prices Under Pressure

Last week, high-grade nickel pig iron (NPI) ex-factory prices dropped significantly, reaching US$134.31/Nickel poinnt as of Thursday, down US$3.5 from before the holiday. Since early April, NPI prices have fallen by a total of US$11.25/Nickel point, a 7.8% decrease.

Shanghai nickel futures were volatile last week. By Thursday’s close, the main contract settled at US$17388/MT, down US$12.65/MT from pre-holiday levels, a 0.07% drop.

On the supply side, Indonesian RKEF nickel premiums remain high, and some smaller plants have started to reduce or halt production due to losses. Domestically, the rainy season in the Philippines has ended, allowing nickel ore supplies to recover for Chinese NPI plants. However, with production costs exceeding market prices, output growth remains limited.

With stainless steel prices remaining low in China, pressure has shifted upstream to raw materials. NPI prices are expected to stay weak in the short term.

CHROME: Sudden 80,000-Ton Supply Surge Impacts May Market

In the first week of May, high-chrome prices declined. Mainstream ex-factory prices dropped by US$14/50reference ton, with retail market offers now ranging from US$1139.24-US$1167.36/50reference ton.

Besides weakening demand, the primary reason for the price drop is a sharp increase in high-chrome output, intensifying supply pressure.

According to data, domestic high-chrome output reached around 702,100 tons in April 2025, up significantly from 613,900 tons in March—a 14.37% month-on-month increase of 88,200 tons.

In May 2025, both TISCO and Tsingshan raised their high-chrome tender procurement prices by US$70/50 reference ton, easing production losses. Meanwhile, southern China’s major production regions began implementing normal and wet-season electricity tariffs, prompting many high-chrome plants to accelerate restarts and ramp up output.

Production in Inner Mongolia, Guizhou, and Guangxi saw particularly large increases, while other regions had smaller fluctuations. With the wet season underway in the south, overall power costs are dropping, further supporting higher production rates.

Expectations for continued supply growth in May, coupled with reduced stainless steel output, point to weaker demand for high-chrome. With supply rising and demand falling, high-chrome prices remain at risk of further decline.

SUMMARY || Raw Material Support Weakens, Stainless Steel Faces Post-Holiday Supply Pressure

Stainless steel prices fluctuated last week. Buyers remained cautious, adopting a wait-and-see approach. Some steel mills scheduled maintenance in May, reducing production output. Social inventories remain high, and spot supplies are abundant.

Attention should be paid to downstream consumption capacity, mill production plans, and inventory drawdowns. Stainless steel prices are expected to move in a volatile pattern.

300 Series: Central bank stimulus policies helped improve sentiment, briefly boosting transactions, but post-holiday inventory pressure persists, and demand remains weak. Some mills reduced production due to shrinking margins and falling costs, or shifted production to 300-series, easing supply-side pressure. Although trade tensions have temporarily eased, uncertainties remain. If domestic policies take effect, internal demand could see further support. In the short term, stainless steel prices are likely to fluctuate, with attention on downstream buying behavior and inventory changes.

200 Series: Domestic policy stimulus continues, while the U.S. Federal Reserve held rates steady in May. This has pressured commodity markets, causing copper prices to dip slightly. However, raw material prices remain high, supporting 201-grade costs. With mixed macro signals, the market leans toward caution. Focus remains on upcoming mill pricing announcements, with 201 prices expected to remain stable in the short term.

400 Series: Retail prices of high-chrome have dropped significantly, weakening cost support for 400-series stainless steel, although levels are still high. Meanwhile, downstream demand has softened and inventory drawdowns are slow, reducing price support. 430 prices are expected to remain stable to slightly weak next week. Keep a close eye on raw material price trends and macro policy developments affecting the stainless steel market.

MACRO|| Stainless Steel Futures Rebound on China-U.S. Statement and Policy Boost

On May 12, encouraged by the China-U.S. Geneva Joint Statement, the three major U.S. stock index futures rose by more than 2%, Hong Kong stocks also rose sharply, and most London metals rose.

Since the China-US trade war in early April, stainless steel futures prices have suffered sharp setbacks, with stainless steel futures prices falling as low as 12,445 yuan/ton, a record low in the past five years. The spot market has been sluggish, and steel mills' losses have intensified. Many steel mills have plans to reduce or switch production in May, and downstream orders have dropped significantly. With the release of the joint statement, import and export trade began to recover, which greatly boosted market sentiment. With the recovery of exports of stainless steel products, downstream end-users' willingness to purchase has increased, coupled with the implementation of China's domestic policies (see below) to boost domestic demand, macro expectations are improving, and stainless steel prices are expected to be strong in the short term.

China's Domestic Macro Policy

China's domestic monetary policy adjustments (such as RRR cuts and interest rate cuts) have released liquidity, reduced market capital costs, and prompted more funds to flow into the commodity market. At the same time, the stimulating effect of policies on the economy has enhanced market expectations for stainless steel demand growth, further strengthening the upward momentum of futures prices.

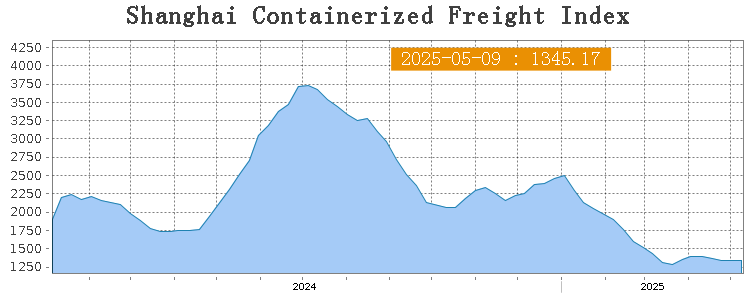

SEA FREIGHT || Market Remains Generally Stable with Slight Fluctuations on Some Routes

China’s export container shipping market remained generally stable following the short holiday, though different trade lanes showed divergent trends due to varying fundamentals. Last week, China’s container export shipping market remained generally stable, with slight fluctuations observed on some routes. On May 9th, the Shanghai Containerized Freight Index (SCFI) rose 0.3% to 1345.17 points.

Europe/ Mediterranean:

The overall composite index recorded a slight increase. Transport demand held steady throughout the week, while spot booking prices saw a minor decline.

On May 9th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1161/TEU, which decreased by 3.3%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$2089/TEU, which remained flat from previous week.

North America:

According to data released by the General Administration of Customs, in April 2025, China’s exports to the U.S. (measured in USD) dropped by more than 20% year-on-year. Since the start of the “tariff war” in April, China’s exports to the U.S. have declined significantly, which is expected to place pressure on the North American container shipping market.

On May 9th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$2347/FEU and US$3335/FEU, reporting 3.3% and 1.6% growth accordingly.

The Persian Gulf and the Red Sea:

On May 9th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf gain 2.0% to US$1145/TEU.

Australia&New Zealand:

On May 9th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand lost 5.3% to US$771/TEU.

South America:

On May 9th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports rose 5.7% to US$1472/TEU.