WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,025 | -26 | -1.32% |

| Foshan | 2,055 | -26 | -1.30% | ||

| Hongwang | Wuxi | 1,930 | -16 | -0.86% | |

| Foshan | 1,945 | -20 | -1.08% | ||

| 304/NO.1 | ESS | Wuxi | 1,865 | -23 | -1.28% |

| Foshan | 1,870 | -24 | -1.36% | ||

| 316L/2B | TISCO | Wuxi | 3,750 | -45 | -1.24% |

| Foshan | 3,775 | -54 | -1.46% | ||

| 316L/NO.1 | ESS | Wuxi | 3,545 | -60 | -1.72% |

| Foshan | 3,560 | -63 | -1.79% | ||

| 201J1/2B | Hongwang | Wuxi | 1,265 | 7 | 0.62% |

| Foshan | 1,265 | 6 | 0.50% | ||

| J5/2B | Hongwang | Wuxi | 1,150 | 1 | 0.14% |

| Foshan | 1,150 | -3 | -0.27% | ||

| 430/2B | TISCO | Wuxi | 1,210 | 0 | 0.00% |

| Foshan | 1,200 | 0 | 0.00% |

TREND | Stainless Steel Market Enters Traditional Off-Season, Steel Mills Face Losses

Stainless steel prices moved weakly last week. Macroeconomic support for market sentiment has gradually weakened, downstream buyers remain cautious, and supply-side pressure persists, leaving steel mills operating at a loss. Market sentiment has turned more watchful, with attention focused on potential macro policy support, mill production schedules, and raw material price changes. As the industry enters the off-season, mills are cutting output, and the market faces a “weak supply and weak demand” situation.

As of Friday, the main stainless steel futures contract fell by US$12.7/MT from last week to US$1905/MT a weekly decline of 0.71%.

Stainless steel 300 Series: Inventory Falls for Fourth Straight Week, Spot Prices Remain Weak

Last week, stainless steel 304 stainless steel prices continued to weaken. As of Friday, the main price for privately produced cold-rolled four-foot stainless steel 304 coils in Wuxi stood at US$1880/MT, down US$14/MT from last week; hot-rolled stainless steel coils were quoted at US$1860/MT, down US$28/MT.

Early in the week, Tsingshan lifted its price control measures, causing both spot and futures markets to come under pressure. The futures market posted three consecutive declines, and transactions cooled again. Increased arrivals of 304 hot-rolled stainless steel resources boosted available supply. Coupled with overall market weakness, the price gap between cold-rolled and hot-rolled stainless steel products widened again to US$21.

Stainless steel 200 Series: Both Futures and Spot Prices Decline, Downstream Remains Cautious

The stainless steel 201 series prices stayed weak and stable last week. Early in the week, mainstream stainless steel 201J2 prices were quoted around US$1130/MT. As the futures market continued to fall and earlier bullish sentiment from mill output cuts faded, downstream buying turned cautious, and trading volume dropped noticeably from last week.

Traders offered discounts to move inventory, with mainstream quotations falling to around US$1120/MT, and many deals were made at lower levels. Cold-rolled stainless steel inventory increased slightly during the week, while hot-rolled stainless-steel inventory saw a small drawdown.

Stainless steel 400 Series: Downstream Demand Weakens, Inventory Continues to Accumulate

The 430 series prices remained stable last week. As of Friday, Wuxi spot prices for cold-rolled stainless steel 430 products wereUS$1215/MT, and hot-rolled stainless steel prices wereUS$1080/MT, both unchanged from last week.

During the week, macro sentiment cooled further while raw material prices continued to fall. Traders lost confidence in the near-term outlook, downstream purchasing slowed, and inventory digestion weakened. The spot market has now seen two consecutive weeks of slight inventory buildup.

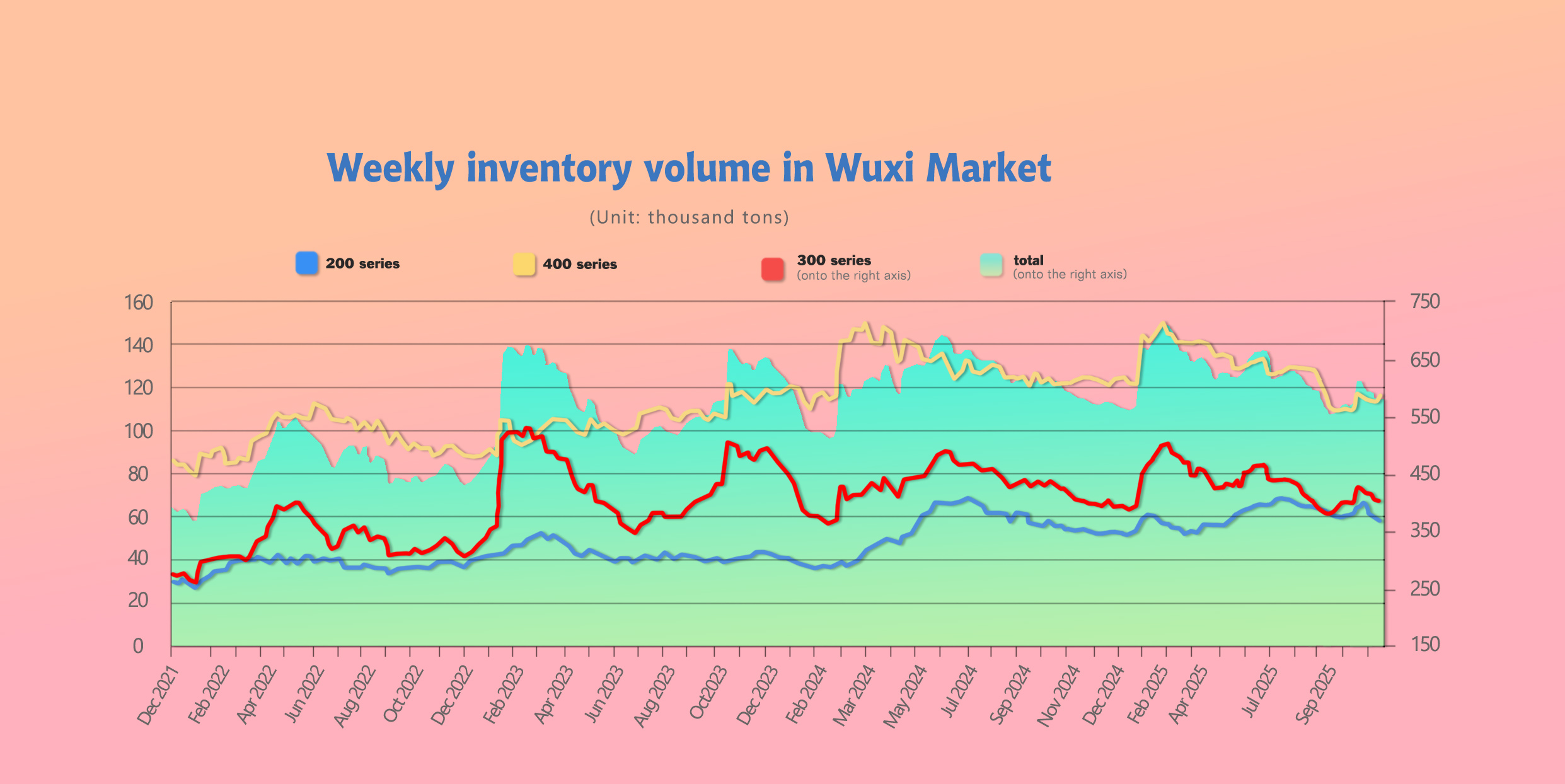

INVENTORY | Stainless steel Stocks Rebound at the Start of the Month

As of November 6th, total stainless steel inventory in Wuxi sample warehouses increased by 5,301 tons to 575,078 tons.

Breakdown:

Stainless steel 200 Series: 207 tons down to 56,726 tons.

Stainless steel 300 Series: 2,445 tons up to 402,386 tons.

Stainless steel 400 Series: 3,063 tons up to 115,966 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Oct 30th | 56,933 | 399,941 | 112,903 | 569,777 |

| Nov 6th | 56,726 | 402,386 | 115,966 | 575,078 |

| Difference | -207 | 2,445 | 3,603 | 5,301 |

Stainless steel 300 Series: Poor Sales After Price Cuts, Sharp Inventory Increase in Agency Warehouses

1.In terms of inventory structure, front-end warehouses in Jiangyin and Jingjiang showed little change last week. However, six vessels are scheduled to unload soon, which will bring additional supply pressure to the market.

2.At the end of October, steel mill agents were required to take delivery, leading to a notable increase in inventory at certain agency warehouses.

3.Market arrivals of 304 hot-rolled products increased, expanding available supply. Combined with the recent overall weakness in stainless steel prices, the price gap between cold-rolled and hot-rolled coils widened again US$21/MT.

Stainless steel 200 Series: Bullish Sentiment Fades, Weak Demand Leads to Cold-Rolled Accumulation

1.In terms of inventory structure, arrivals from Baosteel and Beigang decreased compared to last week, easing overall supply pressure.

2.Throughout the week, the futures market continued to decline. cold-rolled stainless steel 201 prices were quoted around US$1120/MT. Earlier bullish sentiment has been gradually digested, and more low-priced resources have appeared in the market. Downstream buyers turned cautious, resulting in lower trading volumes and an accumulation of cold-rolled inventory.

3.hot-rolled stainless steel 201 prices remained stable, with demand driven mainly by immediate needs. Trading activity was moderate, and hot-rolled inventory saw a small drawdown.

Stainless steel 400 Series: Loose Supply Continues, Sales Become More Difficult

1.From an inventory perspective, JISCO delivered a large volume of new resources last week, increasing market availability.

2.TISCO announced a maintenance plan and will reduce agent contract volumes in November. As a result, market quotations stayed firm, but downstream buyers showed low acceptance of high-priced materials, and overall demand remained weak, slowing inventory digestion.

3.The futures market of stainless steel trended downward last week, weakening trader confidence. Sales became increasingly difficult, and overall transaction volumes were limited.

RAW MATERIAL | Nickel and Chromium Prices Weaken

Chromium: Output Rising, Downside Risks Increasing

Since early November, high-carbon ferrochrome prices have continued to weaken, with mainstream ex-factory prices down by US$14/50 reference ton, now standing at US$1295/50 reference ton.

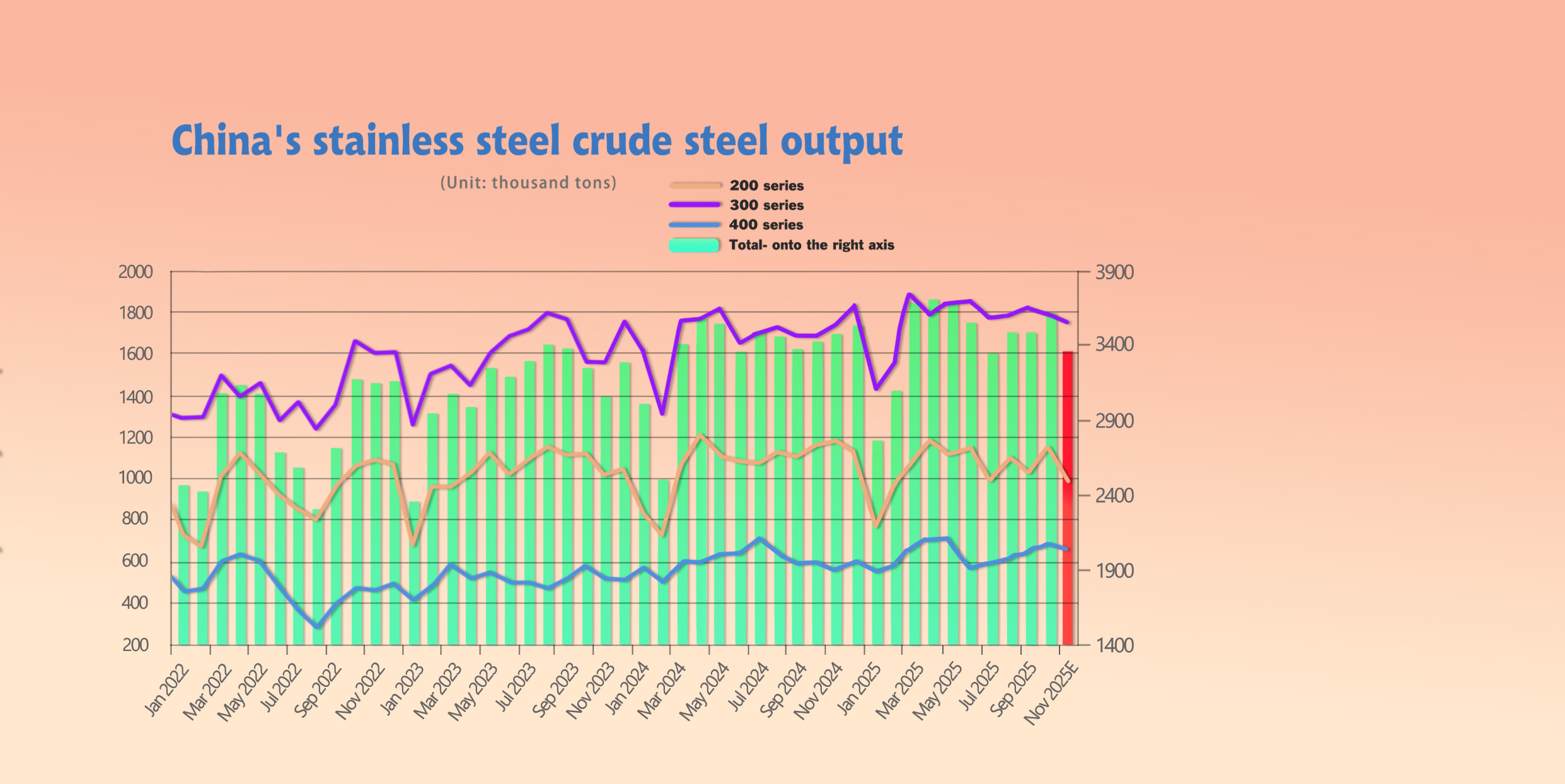

The increase in supply is the main factor behind the price decline. According to data, China’s high-carbon ferrochrome output in October 2025 rose significantly to around 832,100 tons, up 15,800 tons (1.94%) from September’s 816,300 tons.

Looking ahead, November’s ferrochrome production is expected to continue rising. A smelter in Inner Mongolia recently commissioned new submerged arc furnaces at the end of October, which will gradually add output. Meanwhile, falling chrome ore prices have reduced production costs for ferrochrome producers. Coupled with a rebound in ferrochrome imports, the market’s price support remains weak, and further downside cannot be ruled out in the short term.

Nickel: Weak Demand, Producers Losing Profitability

1.Nickel Pig Iron (NPI) Margins Squeezed from Both Sides

On the demand side, stainless steel spot prices have continued to decline. Weak stainless steel consumption has led mills to push back hard on raw material prices, forcing negotiation ranges lower.

On the cost side, shipping of nickel ore from the Philippines has been disrupted as several regions enter the rainy season, keeping ore prices firm. In Indonesia, the 2026 RKAB mining quota reapproval has added policy uncertainty, prompting some NPI producers to stockpile feedstock. Meanwhile, the grade of available ore has fallen, while high-grade ore remains expensive, providing strong cost support for NPI prices.

Although nickel iron prices have been sliding, they are now approaching Indonesia’s lowest all-in cost line. With losses widening for some smelters, the downside room for NPI prices is narrowing.

2.Oversupply Persists

On the supply side, data show that in September 2025, China produced 15,300 tons of mid-to-high-grade NPI metal, down 6.92% month-on-month and 17.49% year-on-year. In contrast, Indonesia’s NPI output reached 156,500 tons of nickel metal, up 1.16% month-on-month and 26.52% year-on-year.

China’s NPI imports in September totaled 136,100 tons of nickel metal, of which 127,700 tons came from Indonesia.

On the demand side, China’s 300-series stainless steel output in September was about 1.7627 million tons, with scrap stainless steel accounting for roughly 23% of input materials. This corresponds to an estimated nickel iron consumption of about 113,100 tons, leaving a monthly surplus of around 37,000 tons of NPI.

Market reports indicate that NPI liquidity has weakened, while oversupply pressure continues to rise. As a result, producers’ bargaining power has diminished, and nickel iron prices remain on a downward trajectory.

SUMMARY

Overall, the nickel pig iron (NPI) market remains caught between oversupply pressure and cost support, and is unlikely to break out of its low range in the short term. The market’s price negotiation center may continue to drift lower, though high ore prices are strengthening support for the NPI floor.

Market sentiment has turned increasingly cautious, with growing concerns over the outlook. In the near term, NPI prices are expected to remain weak, and close attention should be paid to:

Indonesia’s 2026 nickel ore RKAB quota approval process,

policy changes between China and the U.S., and

the operating rates and cost margins of downstream steel mills and NPI producers.

MACRO | Manufacturing PMI Shows Broad Weakness in Supply and Demand

In October, China’s Manufacturing PMI fell by 0.8 percentage points month-on-month to 49.0%, below market expectations (Bloomberg consensus: 49.6%).

Beyond seasonal factors, both supply and demand weakened. The 0.8-point drop in October’s PMI exceeded the 2013–2019 historical average decline of 0.2 points, and the absolute level of 49.0% sits near the lower end of the historical range, suggesting that manufacturing momentum remains weak even after excluding holiday effects.

On a component level, supply fell faster than demand. The production sub-index dropped 2.2 points to 49.7%, entering contraction territory, while new orders declined 0.9 points to 48.8%.

We believe production was likely more affected by seasonal factors, as noted by the National Bureau of Statistics: “Due to some demand being released ahead of the National Day holiday and an increasingly complex international environment, manufacturing activity slowed from last month.”

However, in absolute terms, the pace of contraction in new orders still exceeds that of production, indicating that insufficient effective demand remains a key challenge for China’s economy. Structurally, new export orders fell 1.9 points to 45.9%, weaker than total new orders. This likely reflects heightened trade frictions during the October PMI survey period.

Nonetheless, following the China–U.S. trade consultations in Kuala Lumpur, which reached a preliminary consensus, exports may see marginal softness in Q4, but are expected to remain broadly resilient overall.

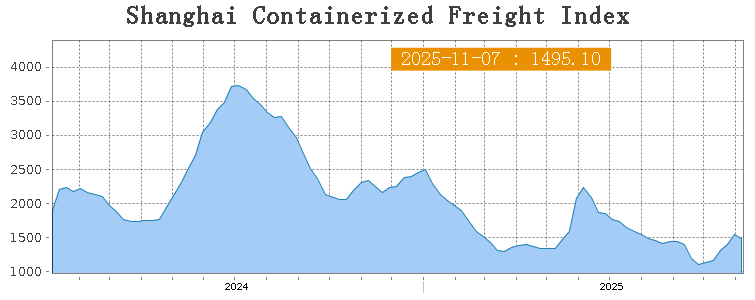

SEA FREIGHT | Entering the Off-Season, Freight Rates Show a Downward Trend

This week, China’s export container shipping market remained generally stable. However, freight rate movements diverged across routes due to differences in supply–demand fundamentals, causing the overall composite index to edge lower.

According to the latest data from China’s General Administration of Customs, October exports (measured in U.S. dollars) fell by 1.1% year-on-year, marking a slower growth pace compared with September. Over the first ten months of 2025, China’s exports have maintained an overall stable growth trend.

On November 7th, the Shanghai Containerized Freight Index (SCFI) rose 7.1% at 1495.1 points.

Europe/ Mediterranean:

On November 7th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1323/TEU, which decreased by 1.6%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$2029/TEU, which was up by 2.3% from previous week.

North America:

Last week, transport demand continued to lack upward momentum, and freight rates in most trade lanes adjusted downward.

On November 7th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$2212/FEU and US$2848/FEU, reporting 16.4% and 17.2% loss accordingly.

The Persian Gulf and the Red Sea:

On November 7th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf gain 8.4% to US$1619/TEU.

Australia & New Zealand:

On November 7th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand increased by 5.6% to US$1385/TEU.

South America:

On November 7th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports fell by 15.4% to US$2171/TEU.