Stainless Insights in China from September 29th to October 12th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,070 | -9 | -0.48% |

| Foshan | 2,115 | -9 | -0.47% | ||

| Hongwang | Wuxi | 1,960 | 0 | 0.00% | |

| Foshan | 1,995 | 0 | 0.00% | ||

| 304/NO.1 | ESS | Wuxi | 1,910 | -7 | -0.40% |

| Foshan | 1,915 | -7 | -0.39% | ||

| 316L/2B | TISCO | Wuxi | 3,745 | -66 | -1.80% |

| Foshan | 3,820 | -38 | -1.02% | ||

| 316L/NO.1 | ESS | Wuxi | 3,605 | -48 | -1.36% |

| Foshan | 3,635 | -50 | -1.40% | ||

| 201J1/2B | Hongwang | Wuxi | 1,265 | 0 | 0.00% |

| Foshan | 1,260 | 0 | 0.00% | ||

| J5/2B | Hongwang | Wuxi | 1,150 | 0 | 0.00% |

| Foshan | 1,160 | 0 | 0.00% | ||

| 430/2B | TISCO | Wuxi | 1,200 | 0 | 0.00% |

| Foshan | 1,215 | 7 | 0.65% |

TREND | U.S. Tariffs at 100%, Stainless Steel Prices Take a Hit

After China’s National Day holiday, stainless steel prices in Wuxi initially rose before falling back. When trading resumed on October 9, stainless steel futures surged on the first trading day but later gave up their gains. On October 10, Donald Trump announced a 100% tariff on Chinese goods, causing further declines in stainless steel futures. Combined with an influx of arrivals from steel mills during the holiday, market inventories grew sharply. By Friday, October 10, the main stainless steel futures contract had fallen US26.9/MT to US$1915/MT, down 1.48%.

Stainless steel 300 Series: Sharp Inventory Build-Up Pressures Prices

The 304 market saw prices rise then fall last week. By October 11th, the mainstream base price for cold-rolled stainless steel 304 four-foot coils in Wuxi stood at US$1905/MT, down US$7/MT from pre-holiday levels. Hot-rolled stainless steel prices were US$1895/MT, down US$21/MT.

Commodity market sentiment has been volatile, leading to choppy adjustments in stainless steel prices. Inflation expectations and post-holiday restocking provided some support, but the global macro environment remains challenging. Market attention now turns to the sustainability of downstream purchasing and the impact of U.S.–China trade policy.

Stainless steel 200 Series: Prices Rise Briefly Before Stabilizing

The stainless steel 201 market was generally stable last week. On October 9, futures gains lifted sentiment, prompting traders to hold firm on offers while low-priced resources diminished. Some transactions saw spot prices of stainless steel rise US$7/MT in the afternoon, though downstream acceptance was limited and overall trading remained subdued. By October 10, as futures slightly reduced, buying interest improved modestly, but overall trading volume stayed constrained as night trading erased weekly gains.

Influenced by disruptions at Indonesian nickel mines and U.S. policy changes, non-ferrous metals strengthened broadly after the holiday. Copper rose significantly, and manganese prices increased by US$14/MT, giving the stainless steel 201 solid cost support. However, stainless steel 200-series crude steel output remains high, and inventories accumulated over the holiday, keeping supply pressure in place. Market focus now shifts to whether demand can recover quickly. The cold-rolled stainless steel 201J2/J5 base price is expected to remain in the US$1105-US$1180 range in October.

Stainless steel 400 Series: Increased Arrivals and Noticeable Post-Holiday Inventory Build-Up

Prices for stainless steel 430 remained stable last week. As of Friday, state-owned cold-rolled stainless steel 430 material in Wuxi was quoted at US$1210-US$1215/MT, while state-owned hot-rolled stainless steel’s prices held steady at US$1060/MT, both unchanged from pre-holiday levels.

With more deliveries arriving post-holiday, inventories grew visibly. Despite firming in the broader metals complex driven by Indonesian supply disruptions and U.S. trade policy shifts, the stainless steel 400-series market continues to face supply-side pressure. Sustained demand will be crucial to support prices in the weeks ahead.

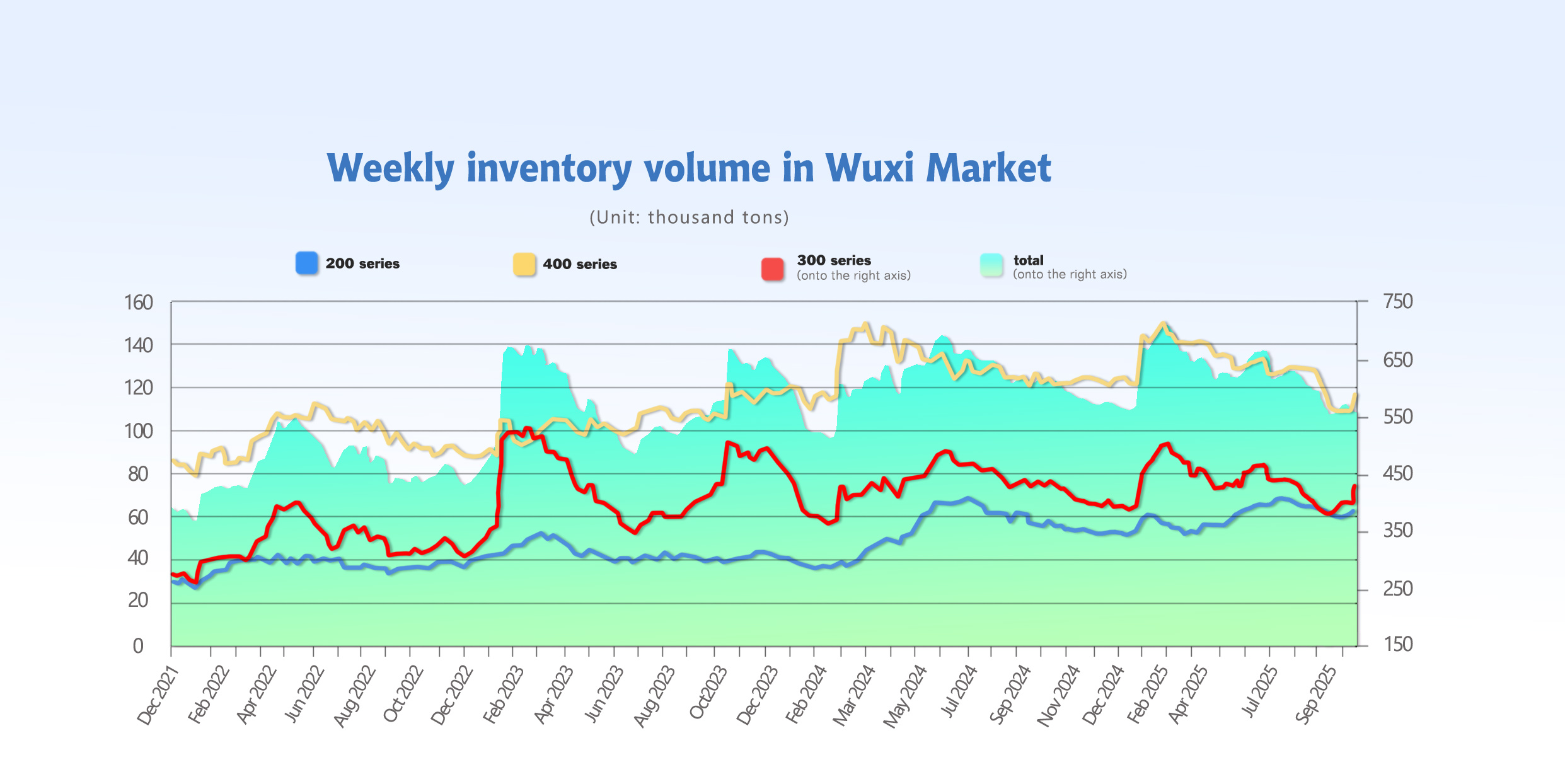

INVENTORY | Trading Halt During Holiday Leads to Stainless steel Inventory Build-Up

As of October 10th, total stainless steel inventory in Wuxi sample warehouses increased by 52,143 tons to 613,179 tons.

Breakdown:

·Stainless steel 200 Series: 7,274 tons up to 67,052 tons.

·Stainless steel 300 Series: 35,791 tons up to 429,162 tons.

·Stainless steel 400 Series: 9,078 tons up to 116,965 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Sep 30th | 59,778 | 393,371 | 107,887 | 561,036 |

| Oct 10th | 67,052 | 429,162 | 116,965 | 613,179 |

| Difference | 7,274 | 35,791 | 9,078 | 52,143 |

Stainless steel 300 Series: Trading Stalled During Holiday, Noticeable Rise in Cold- and Hot-Rolled Stainless Steel Stocks

During the National Day holiday, stainless steel mill deliveries continued, but trading activity came to a standstill, leading to a significant accumulation of social inventory.

Stainless steel market traders remain cautiously optimistic about the October outlook, with some downstream buyers beginning to restock. The coming weeks will hinge on how quickly sales pick up and inventories are drawn down.

Stainless steel 200 Series: Increased Mill Deliveries, Slight Inventory Accumulation

1.Inventory structure: New arrivals from Baosteel and Hongwang added to overall supply pressure.

2.With trading frozen during the holiday and mills continuing deliveries, inventories climbed. After the break, spot prices followed futures slightly higher, but downstream buyers stayed cautious, limiting high-priced transactions and contributing to a cold-rolled build-up.

3.Hot-rolled prices held steady, and downstream buyers focused on low-priced purchases, leaving overall trade volumes moderate.

With post-holiday Stainless steel 201 inventories increasing and 200-series crude steel output still at high levels, the market faces significant destocking pressure. Downstream players are generally adopting a wait-and-see attitude, showing limited acceptance of higher prices. If sales improve slightly, a mild inventory drawdown could occur next week.

Stainless steel 400 Series: Demand Falls Short of Expectations, Supply Pressure Persists

During the National Holiday, a large influx of resources from TISCO and JISCO hit the stainless steel market while trading was mostly frozen, resulting in a noticeable accumulation. With downstream demand weaker than expected and traders purchasing cautiously, leading to limited overall transactions.

In the short term, stainless steel 430 prices are expected to remain stable under persistent supply pressure.

Stainless Steel Output & Consumption in China, 2025

In the first half of 2025, China’s large-scale stainless steel producers recorded 20.47 million tons of crude steel output, up 1.04 million tons year-on-year, an increase of 5.36%.

All major series saw output growth:

·Stainless steel 200 series: 6.30 million tons, up 284,000 ton, or 4.72%.

·Stainless steel 300 series: 10.37 million tons, up 481,000 ton, or 4.86%.

·Stainless steel 400 series: 3.79 million tons, up 276,000 ton, or 7.85%.

Production also rose across long products, coil, and narrow strip categories:

·Wide coil crude steel: 14.87 million tons, up 650,000 tons, or 4.57%.

·Narrow strip crude steel: 2.81 million tons, up 129,000 tons, or 4.8%.

·Long stainless products: 2.78 million tons, up 261,000 tons, or 10.38%.

At the beginning of the year, the Spring Festival holiday and weak downstream demand led many mills to implement maintenance shutdowns, keeping January–February production low. As demand recovered after the holiday and raw material costs rose, stainless steel prices rebounded in both futures and spot markets, restoring mill margins. Production peaked in April, reaching around 3.7 million tons, the highest monthly output of the first half.

However, as U.S.–China tariff tensions persisted, downstream exports weakened, market demand slowed, and stainless steel prices fell. Mills saw margins shrink, and production declined month by month through May and June, with July output expected to slip slightly to around 3.42 million tons.

Stainless Steel Apparent Consumption Up 3.1% in H1 2025

On the demand side, expectations of U.S.–China tariff actions triggered a front-loaded export rush in the first quarter, boosting stainless steel and downstream product exports.

Following the joint statement between China and the U.S. in early May, trade tensions eased slightly. Overall, domestic stainless steel consumption showed mild recovery.

According to data from 51bxg, China’s apparent stainless steel consumption in the first half of 2025 reached 17.2 million tons, up 510,000 tons year-on-year, a 3.1% increase.

By late June 2025, inventory across major domestic trading markets stood at 1.1727 million tons, up 114,000 tons year-on-year, an increase of 10.8%.

In January, trading activity was near-stagnant due to the Lunar New Year, while mill deliveries continued, causing a clear build-up of inventories through February.

Between March and April, synchronized gains in futures and spot prices stimulated stronger downstream demand and higher transaction volumes, driving sustained destocking.

From May to June, production remained high, but demand weakened, raw material cost support softened, and stainless prices fell to multi-year lows, leading to pessimism and cautious, need-based purchasing. By the end of Q2, inventories began to accumulate again.

Raw Materials | Indonesia’s RKAB Policy Aims to Control Nickel Prices

Last week, high-nickel pig iron prices remained steady, closing Friday US$135/ nickel point, down US$0.7 from pre-holiday levels.

After the holiday, Tsingshan purchased over 10,000 tons of high-nickel pig iron at US$134.2/nickel point (tax-included, ex-warehouse) — US$1.4 lower than September prices. Historically, nickel ore prices tend to ease in Q4, but the Indonesian government, aiming to stabilize prices, has required mining companies to submit 2026 production quotas (RKAB) in October, warning against low-price sales. This policy has prevented short-term price declines, providing cost support for nickel pig iron. Overall, nickel ore prices are expected to remain stable, with market attention focused on procurement trends among major stainless mills.

The Indonesian government also announced that, starting October 3rd, 2025, the validity period of mining production quotas will be shortened from three years to one year to enhance control over key commodities such as coal and nickel.

Under the new rules, while 2025 quotas remain valid, miners must submit new RKAB work plans between October 1st and November 15th each year, detailing expected output volumes and obtaining approval before production.

The Indonesian Coal Mining Association expressed concerns that the shorter approval cycle could disrupt normal production planning. Analysts noted the policy is part of Indonesia’s broader effort to tighten supply, stabilize commodity prices, and strengthen environmental oversight.

According to Sumitomo Metal Mining (SMM), the global nickel market is projected to remain in surplus for a third consecutive year in 2026, with an oversupply of 256,000 tons, slightly lower than the 263,000-tonne surplus in 2025.

The report forecasts Indonesian NPI production to grow 4.1% to 1.76 million tons in 2026. However, stainless steel demand growth will be partially offset by weaker battery-sector demand, particularly in China, where the rise of LFP (lithium iron phosphate) batteries continues to dampen nickel usage.

Industry observers believe nickel prices will remain under pressure in the short term due to high inventories and weak demand, though supply disruptions from tighter Indonesian policy and the cost advantage of Indonesian producers could moderate the pace of price decline.

MACRO | Volatile Stainless Steel Market, Focus on Indonesia, EU, and Brazil

Indonesia’s Stainless Steel Exports Could Rise 20% Next Year

As of October 12, 2025, it was reported that Indonesia won a WTO case against the EU concerning anti-dumping duties on stainless steel, opening new opportunities for the country’s downstream nickel industry exports. Industry analysts say this critical “breakthrough” is expected to significantly boost Indonesian stainless steel exports in 2026, with an annual growth rate of 15–20%.

The core of the victory lies in the WTO ruling that the EU must remove anti-dumping (AD) and countervailing duties (CVD) ranging from 10% to 21% on Indonesian stainless-steel products. Mohammad Rizal Taufikrahman, director of the Economic and Financial Development Research Center (Indef), stated:

“Eliminating tariff barriers will directly lower the border prices of Indonesian stainless steel, especially cold-rolled products, in the EU market, restoring their competitiveness.”

This gives Indonesian stainless steel an important price advantage in one of the largest high-end markets. Although the EU can still appeal, and final implementation will take time, the ruling is a major confidence boost for the Indonesian stainless-steel sector. Data show that Indonesian stainless-steel exports were already strong: in 2024, export value reached USD 8.7 billion, with volumes exceeding 11 million tons, up nearly 20% year-on-year. However, the market has long been heavily concentrated in Asia. The WTO decision is seen as a strategic opportunity for Indonesia to break into the more profitable European market.

Opportunities come with challenges. Reports note that the Indonesian industry must consider the EU’s Carbon Border Adjustment Mechanism (CBAM) starting in 2026. Currently, Indonesia’s stainless steel carbon intensity is about 2.3 tons of CO₂ per ton, far above the European average, potentially adding future carbon costs that could reduce its price advantage.

EU Plans 50% Tariff on Steel Imports Beyond Quotas

Recently, the EU announced new steel import restrictions, planning to cut the tariff-exempt quota significantly and raise steel tariffs from 25% to 50%.

According to a statement from the European Commission, the annual steel import quota will be set at 18.3 million tons, a 47% reduction from the 2024 quota. For steel imports beyond this quota, the EU plans to impose a 50% tariff, doubling the current 25% rate.

Brazil’s Second Anti-Dumping Measure on Chinese Cold-Rolled Stainless Steel

On October 10th, 2025, the China Trade Remedy Information Network announced in “Brazil Issues Second Anti-Dumping Sunset Review Final Ruling on Chinese Cold-Rolled Stainless Steel”:

“On September 30th, 2025, the Brazilian Foreign Trade Committee’s Executive Board (GECEX) issued Resolution No. 798, concluding a second anti-dumping sunset review on cold-rolled stainless steel originating from Mainland China and Taiwan, and decided to continue imposing a five-year anti-dumping duty.”

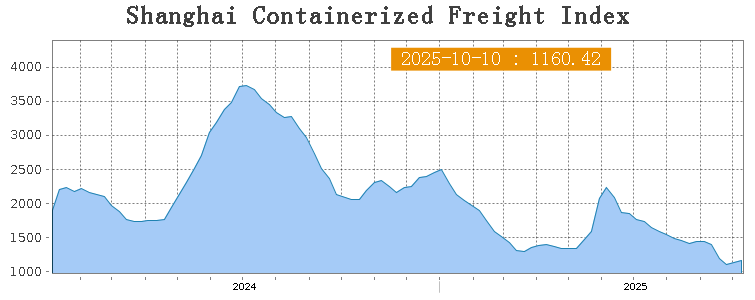

SEA FREIGHT | Ocean Freight Rates Rebound

Last week, China’s export container shipping market showed stable performance following the National Day holiday, with ocean freight rates rebounding, driving an increase in the composite shipping index.

On October 10th, the Shanghai Containerized Freight Index (SCFI) rose 4.1% at 1160.42 points.

Europe/ Mediterranean:

On October 10th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1068/TEU, which increased by 10%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$1558/TEU, which up 4.9% from previous week.

North America:

During the holiday, the U.S. officially announced that, starting October 14, it would impose additional fees on vessels owned, operated, or built by China, as well as all foreign-built car carriers entering U.S. ports. In response, on October 10, China’s transportation authorities announced that, effective October 14, they would charge special port fees on vessels owned, operated, or built by the U.S.

Last week, shipping demand showed signs of stabilization, which contributed to a moderate rise in market freight rates.

On October 10th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$1468/FEU and US$2452/FEU, reporting 0.5% and 2.8% gain accordingly.

The Persian Gulf and the Red Sea:

On October 10th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf surged 15.7% to US$975/TEU.

Australia & New Zealand:

On October 10th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand increased by 6% to US$1159/TEU.

South America:

On October 10th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports jumped by 14.7% to US$2446/TEU.