WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,055 | 0 | 0.00% |

| Foshan | 2,095 | 0 | 0.00% | ||

| Hongwang | Wuxi | 1,945 | 1 | 0.08% | |

| Foshan | 1,970 | 4 | 0.23% | ||

| 304/NO.1 | ESS | Wuxi | 1,890 | 6 | 0.32% |

| Foshan | 1,895 | 1 | 0.08% | ||

| 316L/2B | TISCO | Wuxi | 3,815 | 54 | 1.49% |

| Foshan | 3,820 | 14 | 0.39% | ||

| 316L/NO.1 | ESS | Wuxi | 3,635 | 20 | 0.57% |

| Foshan | 3,635 | 6 | 0.16% | ||

| 201J1/2B | Hongwang | Wuxi | 1,245 | -4 | -0.38% |

| Foshan | 1,255 | 1 | 0.12% | ||

| J5/2B | Hongwang | Wuxi | 1,145 | -4 | -0.41% |

| Foshan | 1,155 | 1 | 0.14% | ||

| 430/2B | TISCO | Wuxi | 1,210 | 0 | 0.00% |

| Foshan | 1,200 | -3 | -0.26% |

Trend | Stainless Steel 304 Futures Rise for Four Consecutive Sessions

From October 20th to 24th, stainless steel prices in Wuxi showed a weak performance. At the start of the week, prices plunged sharply after Donald Trump announced that, starting November 1, he would impose a 100% tariff on Chinese imports—though he later softened his tone, saying the issue “could be discussed.” Futures prices fell to a three-month low early in the week before rebounding on Thursday. As of October 24th, the most-traded contract of stainless steel futures closed at US$1915/MT, down US$24.8 or 1.37% from last Friday.

Stainless Steel 300 Series: Slight Increase in Spot Prices

Last week, 304 stainless steel prices edged higher. By Friday, the mainstream base price for private 304 cold-rolled (four-foot) coils in Wuxi rose to US$1910/MT, up US$7/MT from last week. The private hot-rolled price also increased by US$7MT, reaching US1895/MT.

Stainless Steel 200 Series: Prices Stable, Slightly Higher Trading Volume

Prices for 201 stainless steel remained generally stable. Early in the week, 201J2 traded around US$1115/MT, but many traders offered discounts to stimulate sales, leading to more low-priced resources in the market. Supportive macroeconomic sentiment lifted market confidence, and futures prices continued to rise, prompting some merchants to test higher offers. However, downstream buyers remained cautious, limiting transactions at higher price levels. Overall, trading volume improved slightly compared with last week, with both cold-rolled and hot-rolled stainless steel inventories showing a mild reduction.

Stainless Steel 400 Series: Cost Support Weakens, Prices Under Pressure

Prices for 430 stainless steel stayed largely stable last week. As of Friday, Wuxi cold-rolled stainless steel 430 offered by state-owned mills was quoted at US$1215/MT, while hot-rolled stood at US$1080/MT, both unchanged from last week. Futures prices fluctuated but remained slightly firm, and market sentiment showed mild recovery. Traders offered small discounts to boost liquidity, while steel mills ramped up deliveries of previous orders. As a result, agent pickups increased, leading to a modest drawdown in spot inventories.

Summary | Raw Materials Support Stainless Steel Prices

Stainless Steel 300 Series:

Overall, the futures market extended its rebound last week, and market sentiment improved notably from last week. However, peak-season demand remains weaker than expected, keeping the demand side under pressure and causing prices to fluctuate within a narrow, weak range. With nickel pig iron (NPI) prices falling, upstream raw materials are facing negative feedback pressure, prompting steel mills to push for lower NPI prices, which has weakened cost support. In the short term, the market is expected to maintain a volatile trend, with attention focusing on inventory drawdown progress and how quickly buying interest returns once prices stabilize.

Stainless Steel 200 Series:

Last week, copper and manganese prices continued to rise, strengthening the cost-side support for 201 stainless steel and leaving limited downside room. However, with inventory and production levels still high, and mill deliveries continuing, supply pressure persists. Downstream demand remains muted, so short-term 201 prices are likely to remain steady, with direction depending on upcoming macroeconomic policy signals.

Stainless Steel 400 Series:

High-chromium retail prices dropped significantly last week, weakening the cost support for 400-series stainless steel. Mill production in October remains high, which could further increase supply pressure in the coming period. Meanwhile, downstream consumption remains sluggish, with actual transactions below expectations and mostly driven by rigid demand, leading to slow inventory digestion. Given ongoing expectations for macro policy support, 430 stainless prices are expected to remain steady to slightly weak in the short term amid supply-demand tensions.

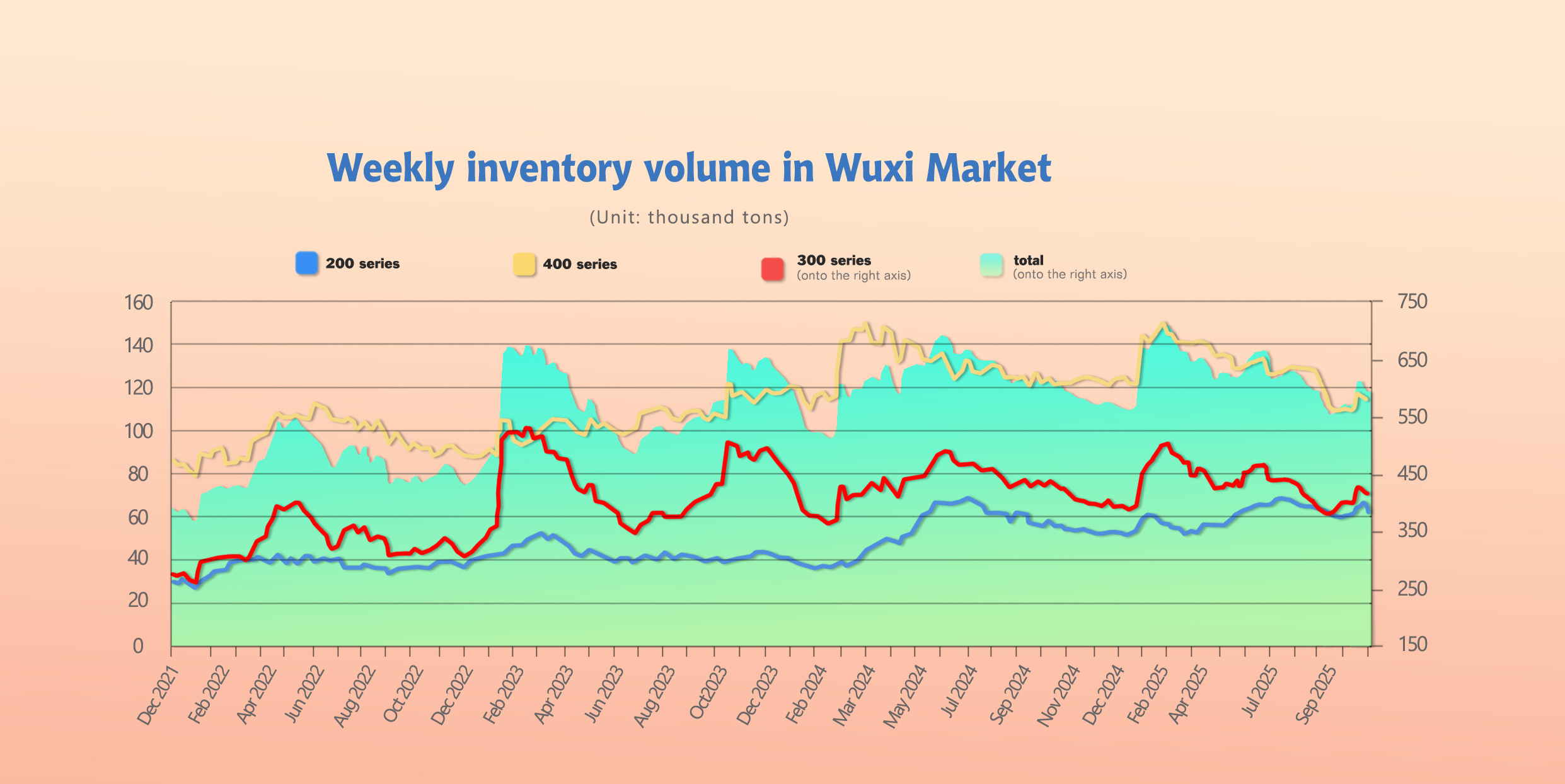

Inventory | Stainless Steel Stocks Down Slightly by 6,400 Tons

As of October 28th, total stainless steel inventory in Wuxi sample warehouses decreased by 6,380 tons to 586,298 tons.

Breakdown:

·Stainless steel 200 Series: 4,433 tons down to 60,167 tons.

·Stainless steel 300 Series: 875 tons up to 413,778 tons.

·Stainless steel 400 Series: 2,822 tons down to 11,253 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Oct 16th | 64,600 | 412,903 | 115,175 | 592,678 |

| Oct 30th | 60,167 | 413,778 | 112,353 | 586,298 |

| Difference | -4,433 | 875 | -2,822 | -6,380 |

Stainless Steel 300 Series: More Cold-Rolled Arrivals, Hot-Rolled in Short Supply

New cold-rolled and hot-rolled stainless steel shipments arrived in the market, but since the hot-rolled supply was tight, most materials were immediately picked up from pre-delivery warehouses, resulting in cold-rolled buildup and hot-rolled depletion.

1. A mill delayed deliveries of hot-rolled stainless steel 304 coils due to a logistics change, exacerbating hot-rolled shortages.

2. Regular arrivals of cold-rolled stainless steel 304 stock added supply pressure to the market.

Throughout the week, stainless steel 304 prices held steady, and after futures prices rebounded, trading improved slightly. As the “Golden October” season winds down, downstream users are focused on just-in-time restocking. However, with mills still operating at high production levels and costs inverted, the risk of inventory buildup remains elevated.

Stainless Steel 200 Series: Improved Trading Sentiment, Cold & Hot-Rolled Stocks Decline

Last week, Wuxi 200-series inventories dropped by 4,400 tons to 60,200 tons (cold-rolled down 2,300 tons, hot-rolled down 2,100 tons).

1. Hongwang’s incoming resources declined, easing supply pressure in the market.

2. Futures prices continued to rise, improving market confidence and stimulating downstream restocking, which helped reduce cold-rolled inventories.

3. 201 hot-rolled prices stayed stable, but buying interest from end-users increased, leading to better overall market activity.

Stainless Steel 400 Series: Slight Cold-Rolled Inventory Reduction

1. JISCO delivered large volumes of previous orders, boosting agent pickups and pre-delivery warehouse drawdowns, leaving fewer tradable resources in the market.

2. Traders offered small discounts to accelerate sales and improve cash flow, slightly reducing cold-rolled stainless steel inventories.

3. 430 hot-rolled stainless steel prices remained stable, but after recent price hikes, buyers resisted higher offers, sticking mainly to essential purchases, resulting in sluggish inventory digestion.

China’s Stainless Steel Mills to Jointly Cut 200-Series Output by Over 500,000 Tons

To ease Q4 supply–demand tensions, reduce market inventory pressure, and maintain industry stability, several leading mills have announced coordinated production cuts:

·Tsingshan Group plans to reduce production by over 300,000 tons between November 2025 and January 2026, mainly in 200-series stainless steel.

·Beigang New Materials will cut production by over 100,000 tons during November–December 2025.

·Baosteel Desheng intends to reduce its steel output by 80,000 tons over the same period.

In total, the three major SS201 producers are expected to cut more than 500,000 tons of output. Meanwhile, another Guangxi-based mill has suspended billet casting operations on October 26 for low-carbon equipment upgrades, expected to last 20–25 days, affecting 200-series sheet and coil output by 24,000–30,000 tons.

Statistics show that in 2024, Tsingshan, Beigang New Materials, and Baosteel Desheng together accounted for 64% of China’s total 200-series crude stainless steel output and 92% of the wide-plate 200-series market.

Such a large-scale production cut signals a clearer and more positive outlook for 201 stainless steel going forward.

Macro | Policy Shifts Closely Shaping Global Demand

1. Macroeconomic Improvement

Between October 25th–26th, China and the U.S. agreed to strengthen bilateral economic and trade communication under the strategic guidance of both leaders, aiming to promote healthy, stable, and sustainable development of economic relations.

As tariff tensions ease, China and overseas sentiment have improved, and export trade is expected to remain volatile at high levels.

2. Production Growth Continues, Imports Rising

In October, stainless steel production reached 3.447 million tons, representing a 0.6% increase compared to the previous month and a 4.75% increase year-on-year. China's domestic mills have continued to increase their output, which has kept supply pressures high. As a result, mills are adjusting their delivery schedules to manage market supply, leading to ongoing shortages of hot-rolled products and maintaining firm prices.

Additionally, imports, particularly from Indonesia’s Yongwang, have steadily increased through August and September. It is anticipated that stainless steel imports will continue to rise into the fourth quarter.

As the "Golden October" season concludes, November arrivals are expected to significantly increase. This rise in market circulation may lead to a slight correction in spot prices.

3. Downstream Demand Weakens; Overseas Demand Fluctuates with Tariff Policy

Demand of downstream industries is diverse — traditional sectors remain weak and worsening, while emerging industries are growing slowly.

In real estate, new project starts fell 18.9% year-on-year, completed area dropped 15.3%, and construction area decreased 9.4%. The sector continues to trade price for volume, with sales weaker than expected and inventories rising, dampening demand across related supply chains.

In contrast, the auto sector remains a bright spot. From January to September 2025, China’s total vehicle sales reached 24.36 million units, with new energy vehicles (NEVs) exceeding 11 million units, accounting for 46.1% of the market share. Although growth rates are slowing, overall market scale and stainless steel consumption continue to expand steadily.

In September 2025, stainless steel exports totaled 418,500 tons, down 29,400 tons (–6.6%) month-on-month and 34,200 tons (–7.6%) year-on-year. Exports to Southeast Asia were 114,600 tons, nearly unchanged from August. With U.S.–China tariff negotiations stabilizing, exports are expected to remain volatile at high levels.

JINLING METALS Insights

The bull–bear tug-of-war in the stainless market is intensifying. Improving macro sentiment, both domestically and abroad, continues to support stainless futures and spot prices.

However, supply pressures may rise further, while demand remains highly uneven and could weaken into the off-season, making it difficult to escape the supply-surplus structure.

With strong expectations but weak fundamentals, stainless steel prices are likely to remain range-bound in the short term.

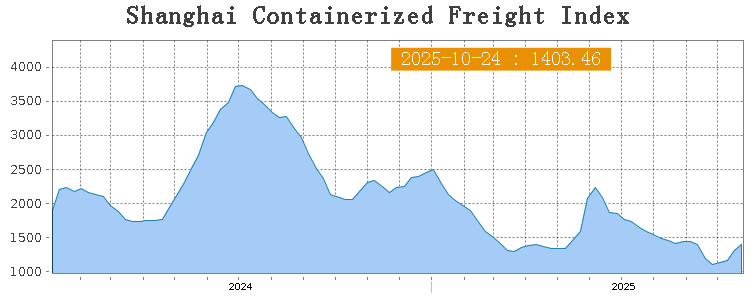

Sea Freight | Most Routes See Rising Rates

Last week, China’s export container shipping market continued its rebound, with stable transport demand. Freight rates increased on most routes, driving the composite index higher. On October 28th, the Shanghai Containerized Freight Index (SCFI) rose 7.1% to 11403.46 points.

Europe/ Mediterranean:

On October 28th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1,246/TEU, which increased by 8.8%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$1764/TEU, which is up 9.4% from the previous week.

North America:

China and the U.S. held economic and trade consultations in Malaysia, with the market closely watching how the talks may affect the future outlook for China–U.S. trade.

On October 28th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$2153/FEU and US$3032/FEU, reporting 11.2% and 6.3% gains accordingly.

The Persian Gulf and the Red Sea:

On October 28th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf surged 14% to US$1423/TEU.

Australia & New Zealand:

On October 28th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand increased by 5.6% to US$1385/TEU.

South America:

On October 28th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports fell by 1.5% to US$2619/TEU.