Stainless Insights in China from April 21st to April 27th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,020 | -6 | -0.29% |

| Foshan | 2,065 | -6 | -0.28% | ||

| Hongwang | Wuxi | 1,925 | -12 | -0.68% | |

| Foshan | 1,945 | -11 | -0.60% | ||

| 304/NO.1 | ESS | Wuxi | 1,870 | -6 | -0.31% |

| Foshan | 1,875 | -6 | -0.31% | ||

| 316L/2B | TISCO | Wuxi | 3,405 | -8 | -0.25% |

| Foshan | 3,485 | 8 | 0.25% | ||

| 316L/NO.1 | ESS | Wuxi | 3,270 | -4 | -0.13% |

| Foshan | 3,310 | 0 | 0.00% | ||

| 201J1/2B | Hongwang | Wuxi | 1,255 | -4 | -0.36% |

| Foshan | 1,240 | -12 | -1.09% | ||

| J5/2B | Hongwang | Wuxi | 1,145 | -12 | -1.19% |

| Foshan | 1,140 | -12 | -1.20% | ||

| 430/2B | TISCO | Wuxi | 1,150 | -3 | -0.27% |

| Foshan | 1,140 | 0 | 0.00% |

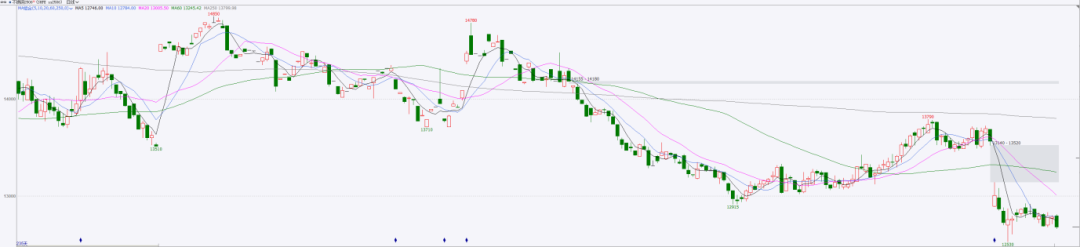

TREND || Stainless Steel Futures Prices Decline Again

Last week, spot stainless steel prices in the Wuxi market followed futures lower, posting slight declines. On the cost side, raw material price drops have led to weaker production costs. With a steady stream of incoming shipments, supply pressure remains high, and weak demand has shown no significant improvement, keeping the overall supply-demand dynamic in a state of weak oscillation. As of Friday, the main stainless steel futures contract price fell by US$14/MT from previous week to US$1870/MT.

In the spot market, stainless steel prices fell by US$7-US$28 during the week. Futures prices remained weak, and the worsening supply-demand imbalance further dragged spot prices down. Although there are potential improvements on the macroeconomic front, the resulting uncertainty continues to weigh heavily on the market, and the short-term outlook remains challenging.

300 Series: Mills Slash Prices Again, Market Panic Spreads

Last week, 304 spot prices edged lower. As of Friday, mainstream base prices for private cold-rolled four-foot 304 coils in Wuxi were quoted at US$1875/MT, down US$21/MT from last Friday. Private hot-rolled 304 prices were quoted at US$1845/MT, down US$28/MT week-on-week.

In the first half of last week, futures prices fluctuated downward, and spot prices were adjusted lower amid strong market caution and moderate trading activity. In the second half of the week, news that Trump suggested lower tariffs on China drove a rebound in futures prices. Spot prices stabilized, lower-priced inventory sold better, and de-stocking accelerated.

However, on Friday, Tsingshan opened with a US$28/MT price cut, which again dampened market sentiment. Agents followed by lowering prices to stimulate sales, with market transactions mainly driven by low-priced, essential demand.

200 Series: Spot Prices Fall, Inventory Depletion Slows

Last week, 201 prices declined. cold-rolled 201J2 was quoted at US$1095/MT (EXW), cold-rolled 201J1 at US$1190/MT, and hot-rolled 201J1 at US$1150/MT.

At the beginning of the week, futures prices remained weak, prompting traders to offer discounts. hot-rolled 201J1 prices fell by US$7/MT.

By last Friday, Tsingshan announced a US$28/MT drop for both hot- and cold-rolled 201, further eroding market confidence. Low-priced resources flooded the market, with some 201J2 products quoted around US$1080/MT. Downstream demand was limited to essential purchases, and overall trading sentiment remained subdued.

400 Series: Cost Support Remains, Prices Hold Steady

Last week, 430 spot prices stabilized. In the Wuxi market, state-owned 430 cold-rolled products were quoted between US$1150-US$1155/MT, unchanged from last weekend. State-owned hot-rolled 430 products were quoted at US$1065/MT, also flat week-on-week.

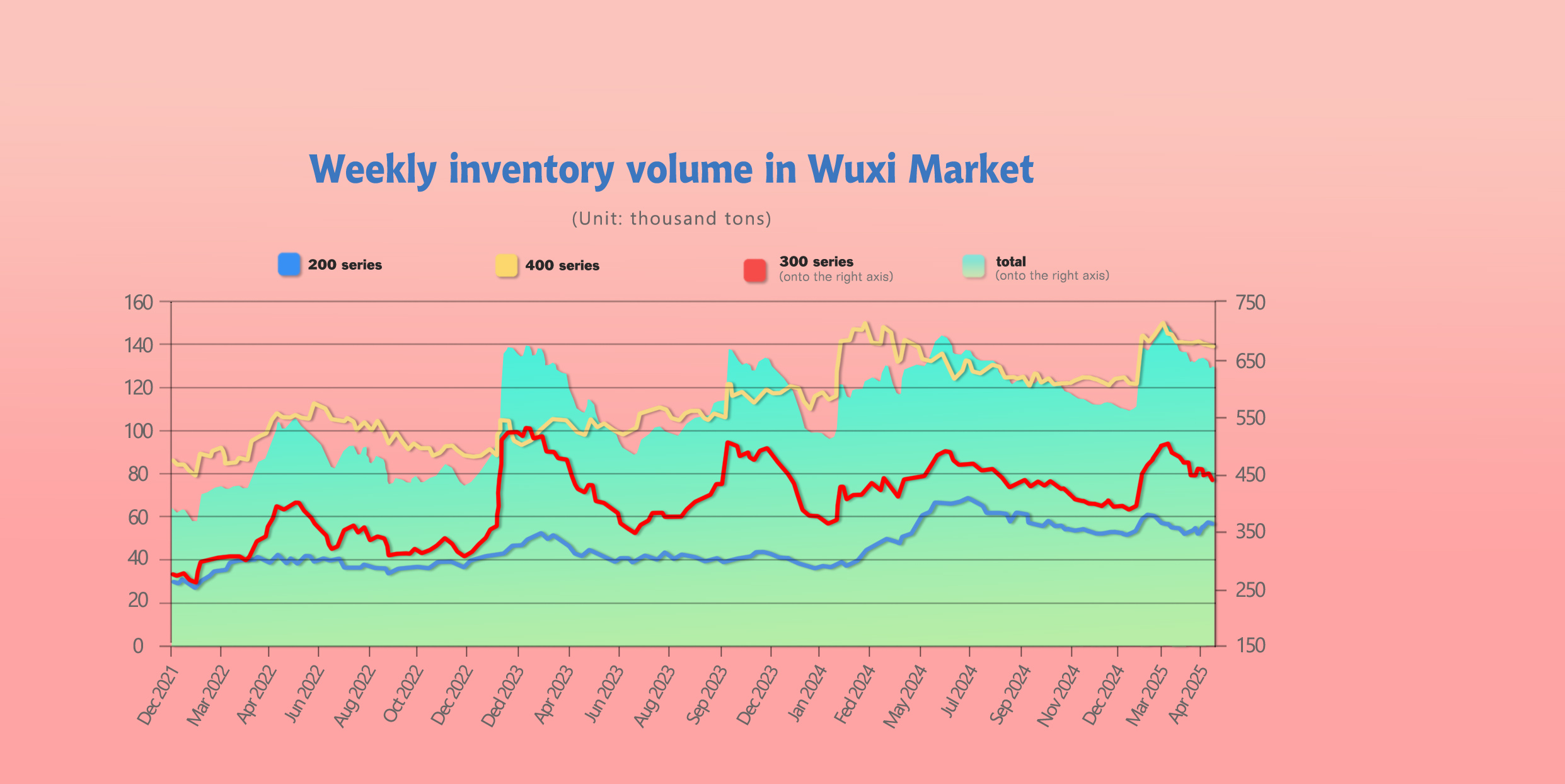

INVENTORY || Pre-Holiday Restocking Drives 2.73% Inventory Reduction

As of April 25th, total inventory in Wuxi sample warehouses decreased by 17,528 tons to 623,498 tons. Breakdown:

200 Series: 21 tons down to 55,460 tons.

300 Series: 14,960 tons down to 430,952 tons.

400 Series: 2,547 tons down to 137,086 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Apr 17th | 55,481 | 454,912 | 139,633 | 641,026 |

| Apr 24th | 55,460 | 430,952 | 137,086 | 623,498 |

| Difference | -21 | -14,960 | -2,527 | -17,528 |

300 Series: April Output Declines

Last week, futures and spot prices remained weak overall. Increased inflows of Delong resources into the market prompted agents to lower prices to boost sales, leading to more low-priced inventory and stronger downstream buying at low prices, which accelerated inventory clearance.

Sino-U.S. trade tensions have eased somewhat, and China has seized the opportunity to implement cuts to reserve requirement ratios and interest rates, improving the macro sentiment. However, supply pressures remain due to abundant market resources.

Demand continues to be largely driven by essential purchasing, keeping the market fundamentally weak. As the May Day holiday approaches, inventories may slightly build after the break.

On the supply side, several mills have announced maintenance and production cuts.

As of April 2025, national cold-rolled stainless steel production rose by 62,000 tons month-on-month to 1.482 million tons (up 4.34%). However, 300-series production dropped by 18,500 tons to 746,000 tons (down 2.4%).

TISCO have seen sharp production cuts due to raw material supply issues and have suspended order-taking for locked-price contracts.

Delong (Xiangshui) has also reduced daily output significantly due to cost pressures and weak demand, with April 300-series production expected to shrink by nearly 30,000 tons.

Other mills like Dongfang Special Steel and Zhangjiagang Pohang also reported varying levels of production reductions.

200 Series: Tight Supply Eases, Inventory Stable

Shortages of thin 201 cold-rolled materials have somewhat eased, but certain specifications like 0.45mm, 0.48mm, and 0.58mm remain scarce.

With the holiday approaching, stockpiling demand may increase, leading to a possible slight inventory buildup next week.

400 Series: Strong Cost Support, Slow Inventory Drawdown

Breaking down the spot inventory, Taigang’s cold- and hot-rolled stock saw significant declines, and Jiugang’s cold-rolled inventory continued its gradual drawdown, resulting in a noticeable overall inventory reduction.

As the effects of tariff-related policies were absorbed, the decline in stainless steel prices slowed. Essential demand from downstream buyers picked up, accelerating inventory clearance for the 400 series.

430 cold-rolled prices remained stable, downstream demand improved, inventory reduction accelerated, and cost support strengthened. Close attention should be paid to future tariff policies and their impact on stainless steel prices.

RAW MATERIALS || Nickel Pig Iron Imports Exceed 1 Million Tons, Setting a New Record

Last week, high-grade nickel pig iron (NPI) ex-works prices continued to weaken, quoted at US$135.5/nickel point as of Friday, down US$2/nickel point compared to previous Friday.

Indonesia’s new export tariff policy on nickel products will officially take effect on April 26. Under the new policy, the export duty for NPI remains at 5% (same as before), but the export duty on nickel ore will increase from 10% to 14%.

Following Tsingshan’s move on Friday to cut prices across all cold-rolled 304 and hot-rolled products by US$28/MT, stainless steel prices weakened again. This has further intensified the issue of inverted production costs at domestic mills. As a result, mills are largely purchasing raw materials on a need-only basis, and nickel pig iron prices are expected to remain under pressure in the short term.

Additionally, surging NPI imports have added further downward pressure on prices.

According to customs data, China imported 1.0133 million tons of nickel pig iron in March 2025, up 11.51% from the previous month and 60.01% year-on-year. Of this, imports from Indonesia totaled 989,100 tons, up 10.54% month-on-month and 61.14% year-on-year.

For the first quarter of 2025, China’s total NPI imports reached 2.8508 million tons, an increase of 26.2% year-on-year, with imports from Indonesia alone at 2.7827 million tons, up 27.8% compared to the same period last year.

As of now, chrome ore spot prices have remained stable for two consecutive weeks.

Even after a US$69/50 reference ton increase in May’s mainstream ferrochrome tender prices, chrome ore prices have continued to hold steady.

Despite significantly higher production costs, ferrochrome producers are still seeing poor profit margins and are less willing to accept high-priced ore.

However, due to the impact of tariff policies, exports of stainless steel and related products have been hampered, dragging down stainless steel prices. This weak trend has spilled over into the raw material market, putting pressure on ferrochrome retail prices and suppressing chrome ore prices as well.

On the supply side, customs data shows that China imported 1.3292 million tons of chrome ore in March 2025, a 27.14% drop from February and a 19.30% decrease year-on-year.

Meanwhile, domestic ferrochrome production rose significantly in March. Under the conditions of reduced supply and growing demand, chrome ore prices have remained firm.

However, as chrome ore prices climbed higher, ferrochrome producers’ willingness to pay high ore prices noticeably declined. Some production restarts were also delayed. This has weakened the upward momentum for chrome ore prices, and prices are expected to remain largely stable in the short term.

SUMMARY || Stainless Steel Social Inventories Remain High; Mills Expected to Cut Production

Stainless steel prices fluctuated weakly last week. Market demand was cautious, with buyers mostly adopting a wait-and-see attitude. Some mills have begun cutting production, and attention is focused on how much production will eventually be reduced. While social inventory levels fell slightly, they remain relatively high, and spot supplies are still abundant. Looking ahead, attention should be paid to demand recovery, mill production scheduling, and inventory depletion. Overall, stainless steel prices are expected to continue fluctuating.

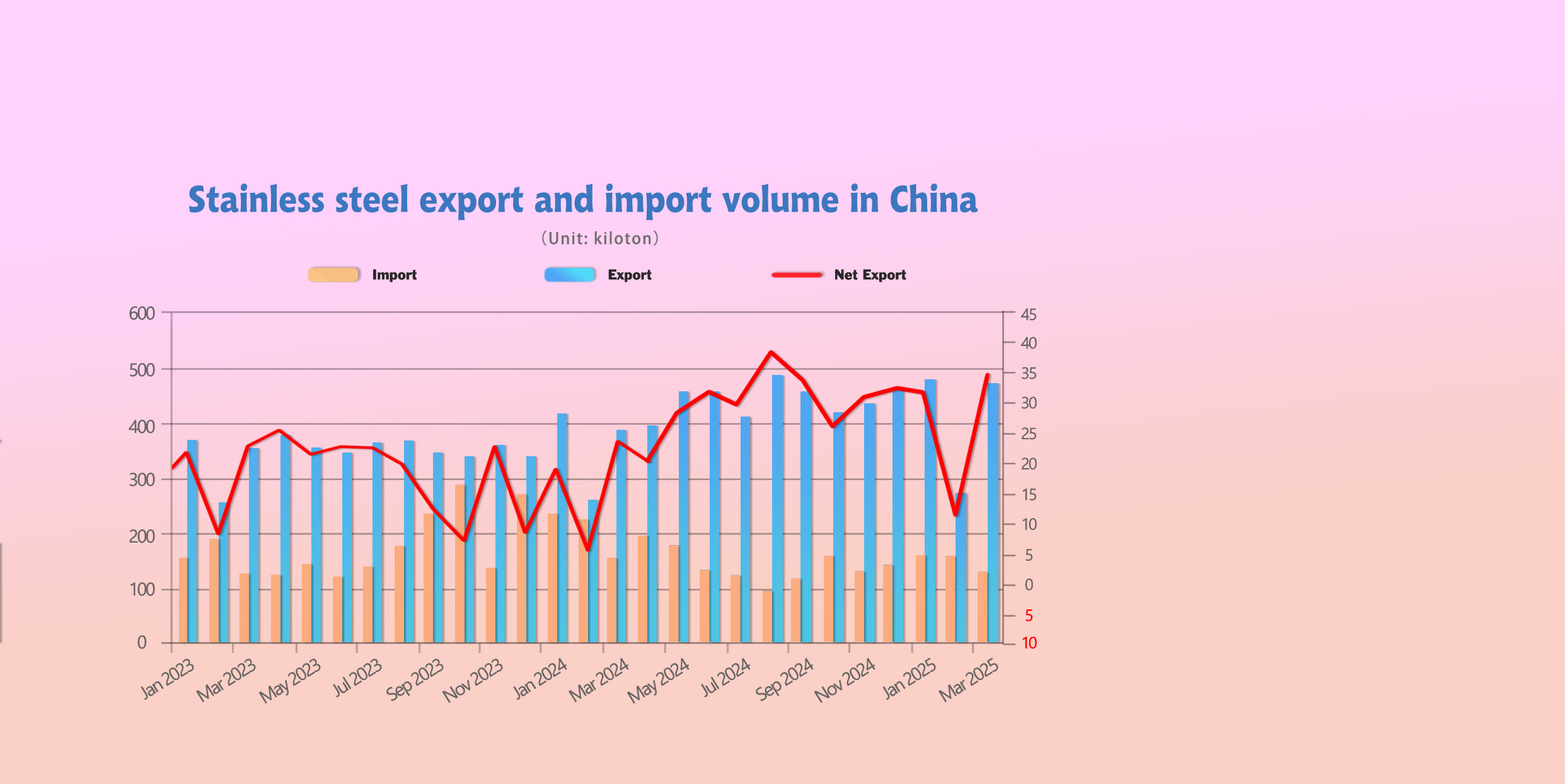

300 Series: Domestic imports of stainless steel declined, and mills have scaled back production, easing supply-side pressure. With tariff tensions easing somewhat, consumer sentiment has slightly improved, and low-priced transactions have picked up. The March rush to export clearly boosted shipments, but going forward, tariffs are expected to impact external demand. In the short term, demand may see a small release ahead of the May Day holiday. Stainless steel prices are expected to remain range-bound in the near term.

200 Series: As macroeconomic tensions eased, the commodity market saw a slight recovery, and rising copper prices provided cost support. However, mills lowered their list prices, and spot prices followed downward. Downstream buying enthusiasm remains low, and overall trading volumes are limited. Under the current supply-strong, demand-weak pattern, 201 prices are expected to continue fluctuating with a weak bias in the short term.

400 Series: Last week, retail prices of ferrochrome edged down slightly. However, the tender prices from mills for May rose, narrowing the price gap significantly. Cost support for 400-series stainless steel remains solid, and downstream purchasing demand has improved, accelerating inventory clearance. Nevertheless, the impact of tariffs on stainless steel and related product exports has not yet fully dissipated. In the short term, stainless steel prices are still under pressure. Next week, 430 stainless steel prices are expected to remain largely stable.

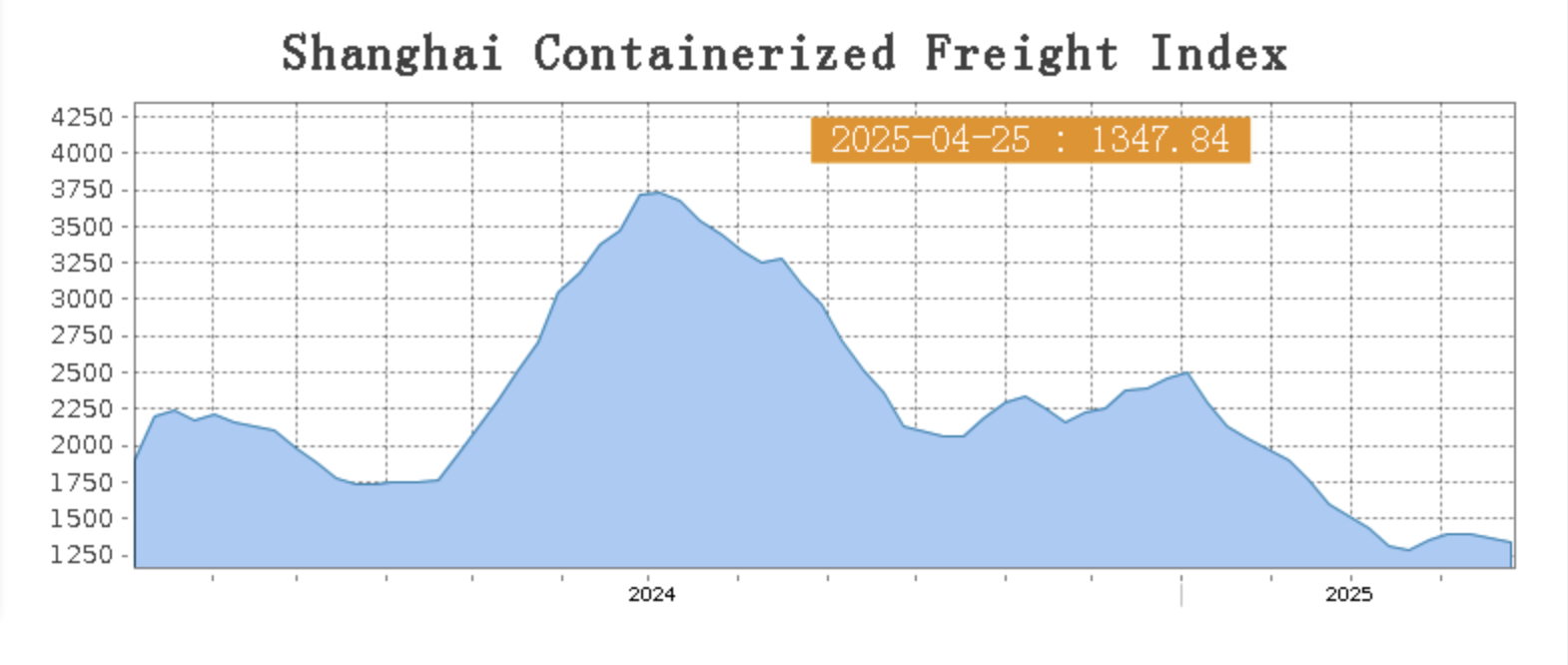

SEA FREIGHT || Market Remains Generally Stable with Slight Fluctuations on Some Routes

Last week, China’s container export shipping market remained generally stable, with slight fluctuations observed on some routes. On April 25th, the Shanghai Containerized Freight Index (SCFI) fell 1.7% to 1347.84 points.

Europe/ Mediterranean:

According to the Economic and Financial Affairs Council of the European Union, the Eurozone Consumer Confidence Index for April was -16.7, lower than expected and showing a significant decline compared to the previous month. Combined with geopolitical risks, the European economy is facing considerable downward pressure. Last week, overall cargo volume remained steady, but carriers mainly adopted price-cutting strategies to attract cargo.

On April 25th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1260/TEU, which decreased by 4.3%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$2129/TEU, which dropped by 1.5%.

North America:

Affected by U.S. tariff policies, the market has broadly revised down its expectations for the U.S. economy. According to recent data released by the University of Michigan, the U.S. Consumer Confidence Index for April was 50.8, a sharp decline from the previous reading, indicating a deteriorating economic environment and a heightened risk of short-term economic downturn in the U.S. In response, shipping capacity deployment is being gradually adjusted, and the market remains in a wait-and-see phase. Last week, with the upcoming May Day holiday approaching, spot booking prices in the immediate market showed an upward trend.

On April 25th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$2141/FEU and US$3257/FEU, reporting 1.8% and 0.2% growth accordingly.

The Persian Gulf and the Red Sea:

On April 25th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf slipped 8.3% to US$1161/TEU.

Australia&New Zealand:

On April 25th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand lost 4% to US$855/TEU.

South America:

On April 25th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports plunged 10.1% to US$1414/TEU.