Stainless Insights in China from August 18th to August 24th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,060 | -13 | -0.65% |

| Foshan | 2,100 | -13 | -0.64% | ||

| Hongwang | Wuxi | 1,955 | -20 | -1.07% | |

| Foshan | 1,960 | -16 | -0.84% | ||

| 304/NO.1 | ESS | Wuxi | 1,880 | -16 | -0.88% |

| Foshan | 1,900 | -6 | -0.32% | ||

| 316L/2B | TISCO | Wuxi | 3,745 | 31 | 0.87% |

| Foshan | 3,775 | 31 | 0.86% | ||

| 316L/NO.1 | ESS | Wuxi | 3,615 | 48 | 1.40% |

| Foshan | 3,605 | 23 | 0.65% | ||

| 201J1/2B | Hongwang | Wuxi | 1,250 | -1 | -0.12% |

| Foshan | 1,240 | -20 | -1.73% | ||

| J5/2B | Hongwang | Wuxi | 1,140 | -8 | -0.82% |

| Foshan | 1,140 | -20 | -1.89% | ||

| 430/2B | TISCO | Wuxi | 1,170 | 10 | 0.95% |

| Foshan | 1,145 | 4 | 0.41% |

TREND | Weak Supply and Demand, Stainless Steel Prices Volatile and Falling

Last week, stainless steel futures prices in the Wuxi market moved downwards, with most commodities falling. Traders lowered prices to stimulate transactions, but actual improvement was limited, and spot prices continued to decline. On the cost side, raw material prices edged higher, while arrivals at some steel mills remained low, leading to slight inventory drawdowns. By Friday, the main stainless steel futures contract had fallen by US$37/MT from last week to US$1920/MT, a drop of 2.00%.

300 Series: Futures and Spot Prices Fall Together, Inventory Drawdowns Slow

Last week, 304 market prices fell weakly. By Friday, the mainstream base price for private cold-rolled four-foot coil in Wuxi was quoted at US$1900/MT, down US$28/MT from last week; private hot-rolled was quoted at US$1870/MT, down US$21/MT. At the start of the week, many mills raised their opening prices to take orders, but the futures market kept weakening, dampening bullish sentiment on stainless steel. Futures saw seven consecutive daily declines, dragging spot prices lower, with weak transactions in the week. On the hot-rolled side, shipments from Delong, Shengyang, and Xinhai remained at low levels, leaving some hot-rolled specifications out of stock. As a result, hot-rolled destocking outpaced cold-rolled.

Last week, 316L stainless steel spot prices continued to rise, up by US$28-US$56/MT. Strong raw material costs and tight supply were the key drivers, keeping prices firm in the short term. On Tuesday, Tsingshan raised its list prices: Yongjin’s 316L cold-rolled was US$3685/MT, up US$42 from the previous opening; Tsingshan’s 316L hot-rolled coil was US$3605/MT, also up US$42. The spot market followed: by Friday, Yongjin 316L cold-rolled was at US$3685/MT; private 316L hot-rolled at US$3635/MT; 316L hot-rolled at US$3680/MT; and 316L cold-rolled trimmed coil at US$3805/MT. On the supply–demand side, Tsingshan recently allocated resources on a daily basis, with weekly volumes limited and very few arrivals, leading to ongoing shortages in the market, especially for hot-rolled, which showed a more pronounced supply–demand imbalance.

200 Series: Prices Edge Lower, Low-Priced Transactions Increase

Last week, 201 prices continued to weaken, with 201J1, J2 cold-rolled and 201J1 hot-rolled down US$7/MT week-on-week. Early in the week, futures fell sharply, undermining confidence in the spot market. Trader offers weakened slightly to around US$1100/MT, while downstream buyers largely stayed cautious, leaving transactions muted. As futures continued to fall later in the week, traders cut prices further, some down to around US$1100/MT, prompting downstream to buy at lower levels, though overall demand remained average.

400 Series: Raw Material Prices Rise Continuously, Cost Pressures Increase

Last week, 430 market prices remained firm. In Wuxi, state-owned 430 cold-rolled was steady at US$1175/MT, unchanged from last weekend; state-owned 430 hot-rolled was steady at US$1050/MT, also flat from last weekend. At the macro level, the U.S. announced an expansion of 50% tariffs on steel and aluminum derivative products, which could negatively impact export demand for 400-series stainless steel, further weighing on market confidence.

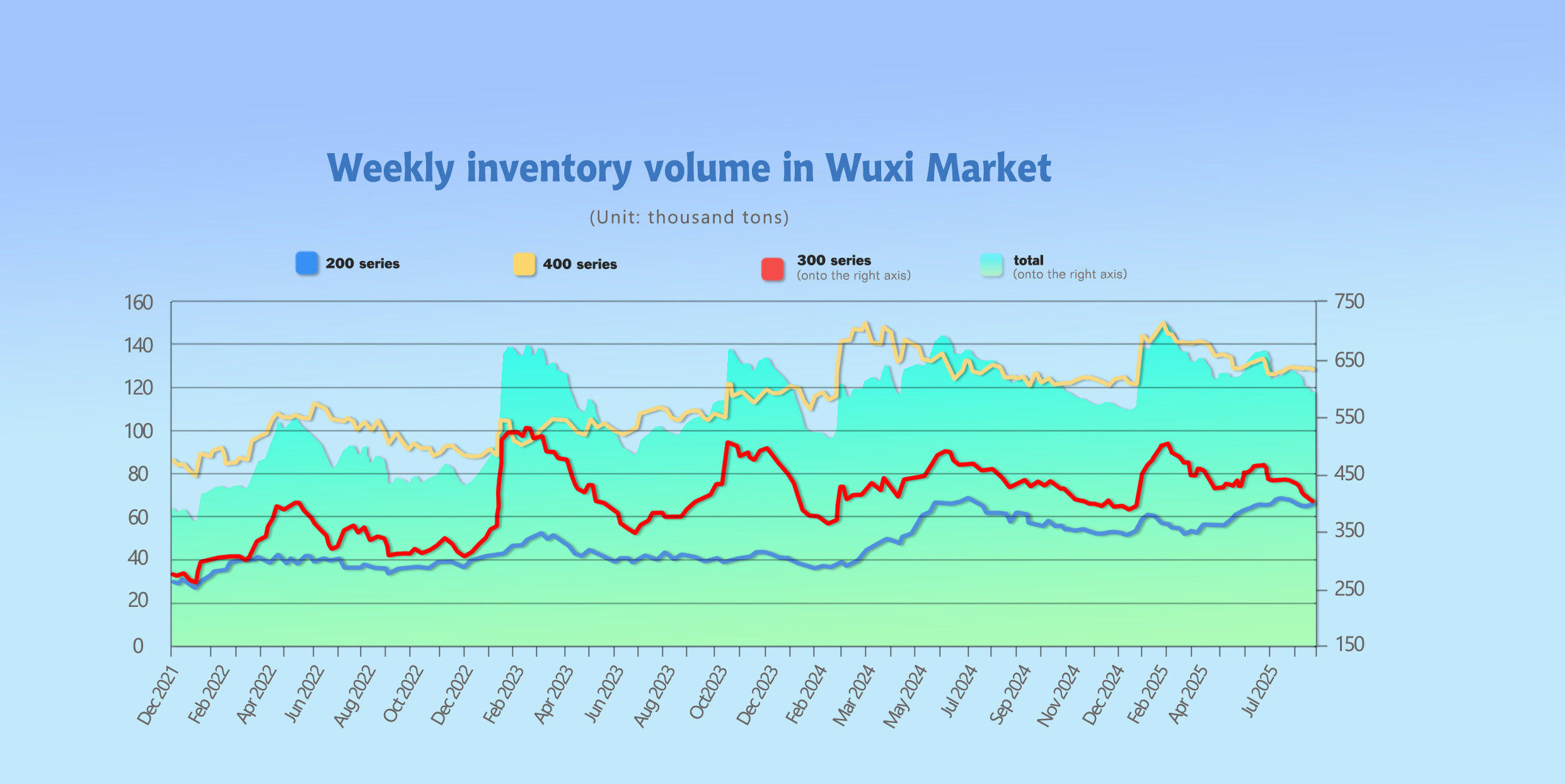

INVENTORY | More than 8,000 Tons Drawn! Prices Fall but Peak Season Nears

As of August 21st, total inventory in Wuxi sample warehouses decreased by 8,353 tons to 587,385 tons.

Breakdown:

- 200 Series: 1,009 tons down to 64,803 tons.

- 300 Series: 6,379 tons down to 395,131 tons.

- 400 Series: 965 tons down to 127,451 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Aug 14th | 65,812 | 401,510 | 128,416 | 595,738 |

| Aug 21st | 64,803 | 395,131 | 127,451 | 587,385 |

| Difference | -1,009 | -6,379 | -965 | -8,353 |

300 Series: Prices Fall, Inventory Drawdowns Slow

From the structure of spot inventories, both cold- and hot-rolled arrivals at Tsingshan’s forward warehouses decreased, and 300-series drawdowns were evident, easing supply pressure. With Delong and Taigang output at low levels, hot-rolled arrivals decreased, leading to stronger destocking for 304 hot-rolled than cold-rolled, with some hot-rolled specs even short. During the week, stainless steel futures and spot prices fell sharply, cooling spot demand, and inventory drawdowns slowed compared with the previous two weeks. With intensified global macro headwinds, combined with steel production cuts and earlier improvements in transactions, social inventories continue to decline. As September peak season approaches, inventories are expected to keep falling. Close attention should be paid to mill production and market consumption.

200 Series: Spot Prices Track Futures Lower, Low-Priced Resources Dominate Transactions

From the spot structure, circulating resources from Hongwang and others decreased last week. 201 cold-rolled prices dropped US$14/MT week-on-week, with mainstream shipments centered around US$1110. Traders cut prices to boost volumes, and low-priced resources appeared, leading to stronger downstream buying and cold-rolled destocking. 201 hot-rolled prices fell US$7, with downstream buying as needed and average transaction activity. As futures weakened through the week, both 201 cold- and hot-rolled prices edged lower, with small discounts in actual transactions. In the short term, 201 prices are expected to run weak to steady, with focus on subsequent trading.

400 Series: Downstream Demand Decent, Inventory Slightly Reduced

From the spot structure, JISCO cold-rolled stocks declined slightly, while TISCO cold- and hot-rolled both saw clear reductions, leaving overall inventories slightly lower. Last week, downstream demand for 400-series stainless steel was decent, while arrivals from mills were limited, driving noticeable drawdowns in spot stocks. Recently, spot inventories have edged down, easing supply pressure. Next week, Wuxi 400-series stainless steel may see restocking demand, pushing inventories slightly higher.

RAW MATERIAL | Partial Suspension of High-Chrome Production

On August 22, mainstream ex-factory prices of high-carbon ferrochrome rose by another US$7 to US$1151/50 reference ton. Since August, prices have cumulatively increased by US$49/50 reference ton. In recent days, retail prices of high-chrome have continued to rise. On one hand, chrome ore and coke prices remain firm, providing strong cost support; on the other hand, with major steel mills’ September tenders approaching, ferrochrome producers’ price-supporting sentiment has strengthened.

In addition, unexpected situations have occurred one after another in the high-chrome market recently. According to recent market sources, in preparation for the September 3rd military parade, production and vehicle transportation of some enterprises around Hebei have been affected, and suppliers have used this to hold up prices. Meanwhile, news has spread that a large ferrochrome producer in Inner Mongolia, a major production region, has suspended operations, which may affect market supply. However, according to industry feedback, given the current high operating rate and strong production enthusiasm among ferrochrome producers, even if production cuts reduce supply by tens of thousands of tons, it will be quickly replenished.

Overall, with mainstream steel mills entering the September bidding period, increased inquiries and procurement in the ferrochrome market, combined with the above favorable factors, will keep prices stable to firm in the short term.

Philippine Rainy Season May Halt 50% of Nickel Ore Production

With only 60 days remaining before the onset of the Philippine rainy season, this seasonal factor will become a “key variable” for nickel ore supply. According to industry trends, approximately 50% of nickel ore production in the Philippines is expected to be suspended during the rainy season. As the Philippines is a key supplier of raw materials to China’s nickel pig iron industry, accounting for more than 40% of China’s nickel ore imports, this capacity contraction will directly lead to a tight global nickel ore market balance.

The market has already reacted in advance: nickel ore suppliers generally expect supply to tighten and are holding firm on pricing, while China’s earlier attempts to curb ore prices have had limited effect. Selby analysis noted: “The cyclical supply tightness caused by the Philippine rainy season often breaks nickel’s range-bound movement. This year, combined with globally low inventories—the London Metal Exchange’s weekly inventory increased by only 1,500 tons, far below surplus expectations—supply-side support for nickel prices will be more significant.”

SUMMARY | Stainless Steel Approaches Traditional Peak Season

Stainless steel prices ran weak last week. As the market approaches the traditional peak season, steel mills are about to complete maintenance, and supply pressure will gradually increase, testing downstream demand capacity. In the short term, demand release remains limited, and high prices continue to suppress purchasing enthusiasm, leading to a wait-and-see sentiment in the market. Going forward, attention will focus on actual demand improvement, steel mills’ production schedules, and changes in raw material prices. Stainless steel prices are expected to fluctuate within a wide range.

300 Series: The stainless steel market is currently under pressure from weak futures and rising warehouse receipts, with spot and futures prices continuing to test lows. Market sentiment remains cautious over the actual implementation of “anti-involution” policies. Prices are expected to remain volatile in the short term, with focus on macro sentiment trends and the strength of seasonal demand recovery.

200 Series: Last week, futures mostly declined, and spot prices continued to weaken accordingly. With raw material costs rising from copper and ferrochrome, production costs for 201 have increased, squeezing steel mills’ profit margins. Market inventories remain high, and supply pressure persists. In the short term, 201 prices are expected to remain stable to slightly weaker.

400 Series: Last week, retail prices of high-chrome raw material rose another US$21/50 reference ton, providing strong cost support for 400-series stainless steel. Cost support and seasonal demand expectations offer rebound momentum, but weak demand and export pressure will limit the upside. In the short term, 400-series stainless steel prices are expected to remain in a narrow fluctuation range, with focus on downstream demand recovery and the specific impact of tariff policies on exports.

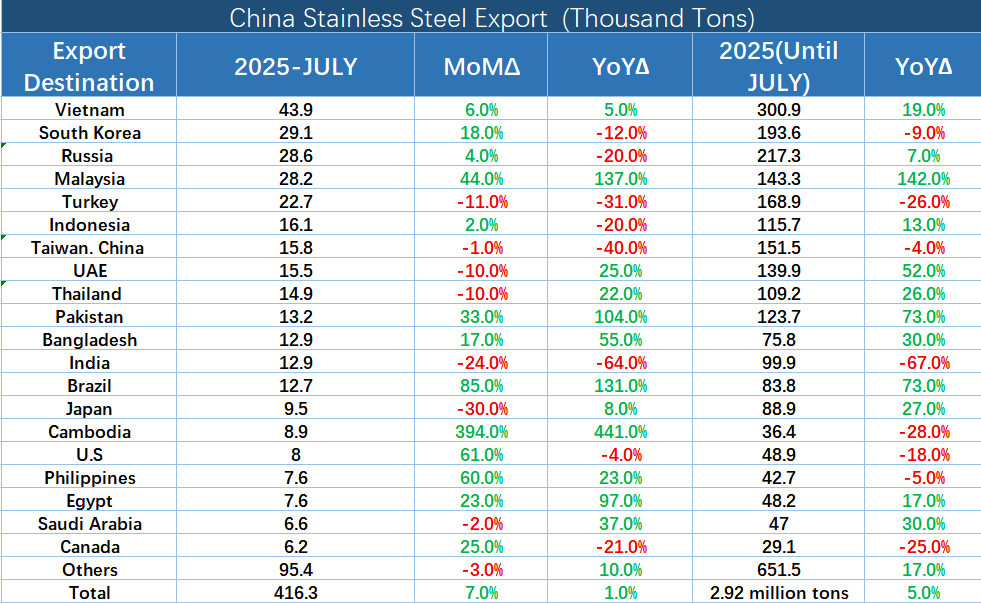

MACRO | U.S. Imports of Chinese Stainless Steel Surge 61% in July

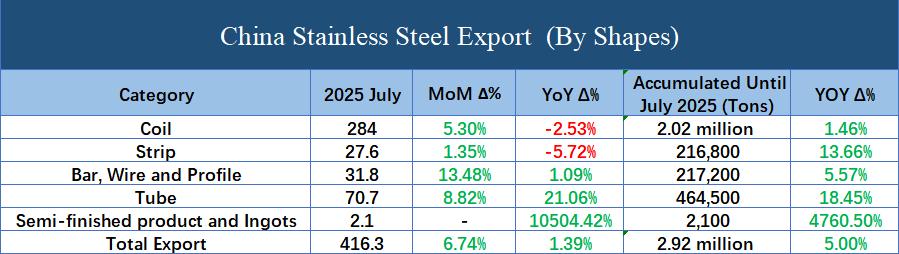

In July, China’s stainless steel exports reached 416,300 tons, up 6.76% month-on-month and 1.40% year-on-year. From January to July, cumulative exports totaled 2.9163 million tons, an increase of 5.08% compared with the same period last year.

As the largest destination for China’s stainless steel exports, Vietnam’s performance has drawn close attention. Since Vietnam removed its anti-dumping measures on Chinese cold-rolled stainless steel in November 2024, exports from China to Vietnam have risen significantly, making Vietnam the top export destination for Chinese stainless steel. In July 2025, China’s stainless steel exports to Vietnam reached around 43,900 tons, up 2,500 tons month-on-month, an increase of 6%; and up 2,100 tons year-on-year, an increase of 5%. From January to July 2025, cumulative exports to Vietnam amounted to around 300,900 tons, up 57,100 tons year-on-year, an increase of 19%.

Looking at the regional distribution of exports, in July 2025, the top 20 export destinations accounted for about 300,900 tons, or 77.08% of total exports that month. From January to July 2025, the top 20 destinations accounted for around 2.2648 million tons, or 77.66% of the total, indicating a high degree of export market concentration.

On August 18, the U.S. Department of Commerce announced the latest implementation rules for the Section 232 derivative tariffs. The new regulation centers on imposing punitive tariffs of up to 50%—and in some cases as high as 200%—on products exported to the United States that contain any steel or aluminum components, depending on the transparency of their raw material origin.

This measure, described by the industry as the “strictest trade barrier in history,” is expected to have a profound and disruptive impact on China’s stainless steel export landscape. Although exports to the U.S. in July 2025 surged 61% month-on-month (likely due to “front-loading” ahead of the policy’s implementation), they still fell 4% year-on-year. More tellingly, cumulative exports from January to July plunged 18% year-on-year, clearly showing that export momentum is weakening rapidly.

Unlike the earlier Section 232 tariffs, which mainly targeted primary steel and aluminum products, the new rule extends oversight to almost all downstream finished goods. According to the announcement, U.S. importers must provide three core documents when declaring imports:

1.Proof of the “melt and cast” origin of the steel or aluminum materials;

2.The value share of steel or aluminum components in the product;

3.The weight of steel or aluminum components in the product.

The severity of the new rule lies in its penalty mechanism: if the origin of raw materials cannot be verified (“origin unknown”), the steel and aluminum content of the product will face a staggering 200% tariff. Even if documentation is provided, a 50% tariff will still apply. For manufacturers whose profit margins are already thin, this represents an unbearable burden.

The new U.S. Section 232 rule will undoubtedly reshape the global stainless steel supply chain. It not only raises the cost and barriers for exports to the U.S., but also fundamentally forces Chinese manufacturers to improve supply chain transparency and traceability. Companies unable to prove the “clean origin” of their raw materials may be forced to withdraw from the U.S. market or turn to re-export routes as alternatives. The entire industry now faces a harsh round of reshuffling. The chain reaction triggered by this trade policy has only just begun.

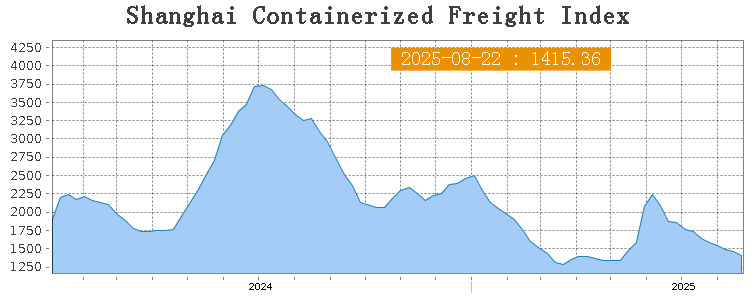

SEA FREIGHT | Market Remains Stable, Most Route Rates Decline

Last week, China’s export container shipping market continued to adjust, with freight rates on most routes declining, dragging down the overall index.

On August 22nd, the Shanghai Containerized Freight Index (SCFI) fell 3.1% to 1415.36 points.

Europe/ Mediterranean:

On August 22nd, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1668/TEU, which decreased by 8.4%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$2225/TEU, which dip 2.4% from previous week.

North America:

Last week, transport demand continued to lack upward momentum, and freight rates in most trade lanes adjusted downward.

On August 22nd, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$1644/FEU and US$2613/FEU, reporting 6.5% and 3.9% slide accordingly.

The Persian Gulf and the Red Sea:

On August 22nd, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf gained 7.1% to US$1479/TEU.

Australia & New Zealand:

On August 22nd, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand gained 2.3% to US$1267/TEU.

South America:

On August 22nd, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports decreased by 7% to US$3107/TEU.