Stainless Insights in China from September 1st to September 14th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,070 | -3 | -0.15% |

| Foshan | 2,115 | -3 | -0.14% | ||

| Hongwang | Wuxi | 1,970 | -1 | -0.08% | |

| Foshan | 1,995 | 6 | 0.30% | ||

| 304/NO.1 | ESS | Wuxi | 1,920 | 11 | 0.63% |

| Foshan | 1,925 | 7 | 0.39% | ||

| 316L/2B | TISCO | Wuxi | 3,830 | 11 | 0.31% |

| Foshan | 3,875 | 3 | 0.08% | ||

| 316L/NO.1 | ESS | Wuxi | 3,695 | 6 | 0.16% |

| Foshan | 3,690 | 4 | 0.12% | ||

| 201J1/2B | Hongwang | Wuxi | 1,255 | -1 | -0.12% |

| Foshan | 1,255 | 0 | 0.00% | ||

| J5/2B | Hongwang | Wuxi | 1,150 | -6 | -0.54% |

| Foshan | 1,155 | 0 | 0 | ||

| 430/2B | TISCO | Wuxi | 1,190 | 0 | 0 |

| Foshan | 1,190 | 9 | 0.80% |

TREND | Stainless Steel Mill Output Recovers, Positive News Lifts Stainless Steel Prices Again

Last week, stainless steel prices in the Wuxi market showed a stable-to-firm trend. In the first half of the week, futures fluctuated while downstream buyers remained cautious. By Friday, prices rebounded sharply and market transactions improved. As of Friday’s close, the main stainless steel futures contract settled at US$1955/MT in the night session, up 0.78% week-on-week, with an intraweek high of US$1960/MT. Overall, entering September, mills reported better order intake and September production schedules increased further. Expectations are building for higher availability of stainless steel 200- and 300-series resources, while inventory destocking has slowed. However, with Tsingshan offering discounts and demand showing seasonal recovery, the short-term outlook for September prices is mostly optimistic. In the medium-to-long term, with supply and demand remaining loose, prices still face downside risks. Market participants are watching macro policy signals and the pace of inventory changes.

Stainless Steel 300 Series: both hot and cold rolled witnessed a rise in price

The stainless steel 304 market posted modest gains last week. As of Thursday, four-foot cold-rolled stainless steel 304 by the mainstream private mill in Wuxi stood at US$1930/MT, down US$7/MT from last week. Private hot-rolled stainless steel prices were quoted at US$1920/MT, up US$7/MT from last week. Mill raw material procurement prices ticked higher, with spot prices outperforming futures. A persistent shortage of hot-rolled 304 kept its price firm, while cold-rolled arrivals from Indonesia’s Everbright since late August created more availability. As a result, cold-rolled prices were weaker than hot-rolled, and the price gap between the two narrowed further.

Stainless Steel 200 Series: Prices were weaker as futures prices dropped.

Stainless steel futures prices fluctuated last week, while spot prices saw slight declines. Both cold-rolled stainless steel 201J1 and J2 prices dropped US$7/MT week-on-week. At the start of the week, traders’ offers remained firm, with cold-rolled J2 shipments quoted at US$1130/MT. As futures weakened, downstream buying interest was limited, prompting merchants to cut offers by US$7/MT to around US$1135/MT. On Friday, futures rebounded, boosting transaction volumes. Inventories of both cold- and hot-rolled declined during the week.

Stainless Steel 400 Series: Prices remained steady as last week.

The stainless steel 430 market remained stable last week. In the Wuxi spot market, state-owned cold-rolled stainless steel 430 was quoted at $1,200 per metric ton, while hot-rolled stainless steel held steady at $1,055 per metric ton, with both prices remaining unchanged from the previous week. Additionally, retail prices for high-carbon ferrochrome increased by $14 per ton last week, reaching $1,320 per 50 reference tons, which provided stronger cost support for the 400 series.

Stainless Steel Bar Market Demand Muted, October Offers Edge Lower

Raw material prices showed mixed trends recently. Nickel rose slightly during the week, supported by earlier news from Indonesia. With September steel mill production increasing, overall demand is expected to recover, keeping prices stable in the short term. Ferrochrome prices held steady as coke eased slightly but chrome ore stayed firm and high-chrome tenders remained elevated. In contrast, ferromoly prices fell as molybdenum concentrate dropped, dragging spot prices down to around US$41560/60 reference ton, with end-users staying cautious.

Early last week, stainless steel futures weakened, before rebounding slightly over the weekend. Supported by seasonal demand, traders kept offers firm, but inquiries and transactions in recent weeks failed to improve significantly. As futures softened and mills cut October offers of stainless steel bar, sentiment turned less positive for late September and October. Futures prices are currently about US$21/MT lower than spot, with many deals based on futures contracts.

For stainless steel 316L bars, both molybdenum concentrate and ferromoly prices weakened, pulling retail quotes below US$41134/MT. Stainless steel mill tender prices have been slow to adjust, mainly in the US$40425 to US$40992/60 reference ton range. While traders’ offers remain high, downstream buyers have become increasingly cautious, leading to lower transaction volumes.

In summary, weaker raw material support has reduced cost backing for stainless steel bar prices, shifting market sentiment toward wait-and-see. In the short term, stainless steel 304 and 316L bar prices are expected to remain stable, with stainless steel 304 round bar (dia 65) quoted at US$1895/MT, and stainless steel 316L (dia 65) at US$3680/MT.

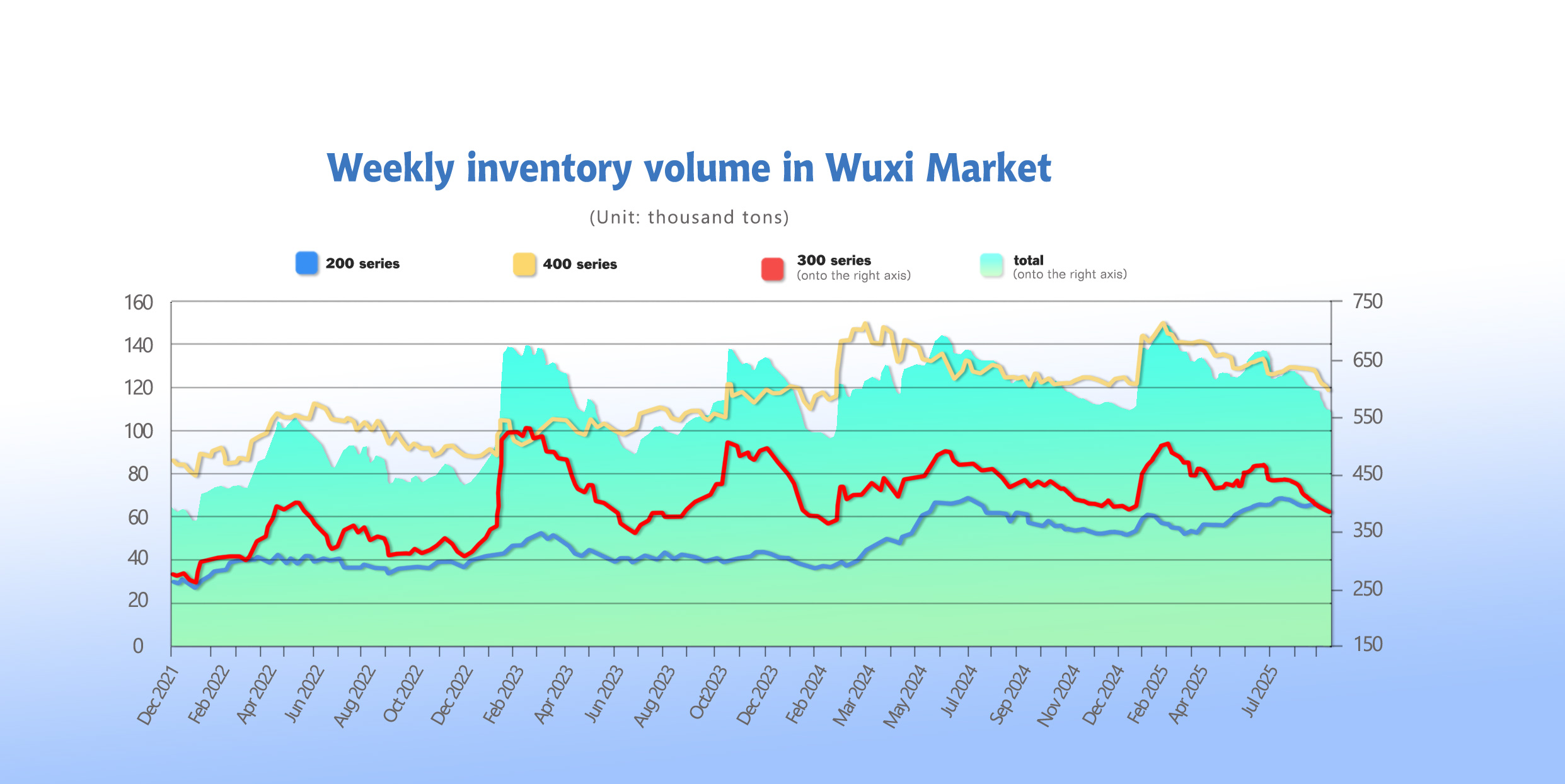

INVENTORY | Cold-Rolled Stainless Steel 300-Series Inventory Climbs

As of September 11th, total inventory of Stainless Steel in Wuxi sample warehouses decreased by 3,744 tons to 549,789 tons. Breakdown:

Stainless Steel 200 Series: 2,077 tons down to 60,459 tons.

Stainless Steel 300 Series: 4,133 tons up to 380,733 tons.

Stainless Steel 400 Series: 5,800 tons down to 108,597 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Sep 4th | 62,536 | 376,600 | 114,397 | 553,533 |

| Sep 11th | 60,459 | 380,733 | 108,597 | 549,789 |

| Difference | -2,077 | 4,133 | -5,800 | -3,744 |

As of September 11, total inventories in Wuxi sample warehouses decreased by 3,700 tons from the previous week to 549,800 tons. By series: 200-series stocks declined 2,100 tons to 60,500 tons; 300-series stocks increased 4,100 tons to 380,700 tons; 400-series stocks decreased 5,800 tons to 108,600 tons.

Stainless Steel 200 Series: Stable Transactions, Modest Drawdown

From the perspective of spot inventory structure, new arrivals of Hongwang material increased last week, boosting market supply. As futures prices rebounded initially, 201J2 cold-rolled spot offers firmed around US$1130/MT base, with traders showing strong price support. Active downstream buying lifted sentiment and encouraged inventory drawdown. 201 hot-rolled prices were unchanged week-on-week, with mill arrivals limited, keeping transactions acceptable and hot-rolled inventories edging down. Overall, 201 cold- and hot-rolled spot prices remained steady to slightly weaker, with steady arrivals creating supply pressure. Short-term 201 prices are expected to stay stable, pending transaction performance.

Stainless Steel 300 Series: Everbright Arrivals Drive Cold-Rolled Stock Build

From the perspective of spot inventory structure, recent Indonesian Everbright shipments continued arriving, with Jiangyin and Jingjiang pre-stock warehouses seeing an increase in cold-rolled volumes. This added supply pressure to cold-rolled stainless steel 304. Meanwhile, reduced mill output limited hot-rolled arrivals, tightening supply and sustaining hot-rolled drawdowns. Stainless steel entered the traditional peak season, but downstream demand fell short of expectations, leading to a stock build in the 300 series.

Macro sentiment has warmed recently, and stainless steel futures remained volatile. With September–October being the traditional consumption peak, demand expectations remain strong. At present, cold-rolled supply is abundant while hot-rolled remains tight. Going forward, attention will focus on mill production and end-user demand.

(Note: Including warehouse receipt resources, Wuxi 300-series cold-rolled social inventory plus receipts stood at 253,900 tons last week, up 7,500 tons or 3.06% from last week, but down 59,900 tons or 19.10% from the same period last year.)

Stainless Steel 400 Series: Mill Output Cut, Inventories Continue to Decline

From the perspective of spot inventory structure, both cold-rolled and hot-rolled stainless steel stocks declined last week, mainly due to reduced output from JISCO, which lowered Wuxi market arrivals. Meanwhile, with the stainless steel peak season arriving, downstream demand increased, further accelerating spot inventory drawdowns. Downstream procurement for the 400 series picked up, while mills cut supply, causing inventories to decline faster.

Looking ahead, 400-series inventories in Wuxi are expected to continue declining. With replenishment demand rising, inventories will likely fluctuate slightly.

SUMMARY | Peak Season Brings a Stainless Steel Market Recovery

Stainless Steel 300 Series:

Overall, entering September, stainless steel mill orders improved and production schedules picked up. Available circulation of 200- and 300-series resources is expected to increase, slowing inventory drawdowns. However, with Tsingshan offering discounted allocations and seasonal recovery on the demand side, short-term sentiment on September pricing remains optimistic. In the medium to long term, with supply and demand relatively loose, prices still face downside risk. Attention will focus on macro policy guidance and inventory movements.

Stainless Steel 200 Series:

Last week, raw material prices turned from red to green, with copper prices rebounding and cost support becoming evident. With peak season expectations, downstream transactions were acceptable, and both cold-rolled and hot-rolled 201 inventories declined. However, overall 200-series supply remains at high levels. Attention should be given to subsequent transaction performance. In the short term, 201 prices are expected to maintain stable operation.

Stainless Steel 400 Series:

Last week, retail high-carbon ferrochrome prices rose again, while September high-carbon steel tender prices increased US$43/50 reference ton, keeping 400-series stainless steel costs elevated. With 400-series spot inventories continuing to decline recently and “Golden September” demand increasing, mills strengthened their price-support stance. Next week, 430 prices are expected to have an upward trend.

RAW MATERIAL | Demand Recovers, but Margins Remain Under Pressure

Copper prices rose slightly week-on-week, strengthening cost support for 201. In September’s traditional peak season, downstream demand showed signs of recovery, with transaction activity improving compared with last month. However, most market participants remain cautious about October’s price outlook, with some leaning bearish. Short-term 201J2/J5 cold-rolled mill-base prices are expected to run in the US$1105 to US$1180/MT range.

Nickel Pig Iron (NPI):

Last week, high-grade NPI ex-works prices strengthened, closing Friday at US$136/nickel point, up US$1.4 unit from last Friday.

At the start of the week, Tsingshan’s high-grade NPI tender settled at US$135.4/nickel point (ex-works, including tax), with about 20,000 tons traded for late October delivery. Indonesia’s Dongte NPI plant sold over 10,000 tons to traders at US$135.8/nickel unit (ex-works, including tax). While tender prices rose compared with last week, mills remain close to breakeven and have limited acceptance of high-cost raw materials. Oversupply in the NPI market remains difficult to shift in the short term, and prices are expected to remain stable.

Ferrochrome:

Last week, mainstream high-carbon ferrochrome ex-works prices rose to US$1320/MT 50 reference ton, up US$14/50 reference ton from last week. Chrome ore spot prices held steady: 40–42% South African concentrate remained at US$7.9/MT, while 40–42% Turkish lumpy ore stayed at US$8.5/MT, unchanged week-on-week.

Recently, retail ferrochrome prices edged higher, supported by firm chrome ore costs. However, as ferrochrome prices rose, downstream procurement became more cautious, and with spot supply in the ferrochrome market increasing, the pace of price gains slowed. Next week, ferrochrome prices are expected to remain steady.

MACRO | China Stainless Demand Recovers, Korea to add Extra Tariffs on Chinese and Japanese Hot-Rolled Stainless Steel.

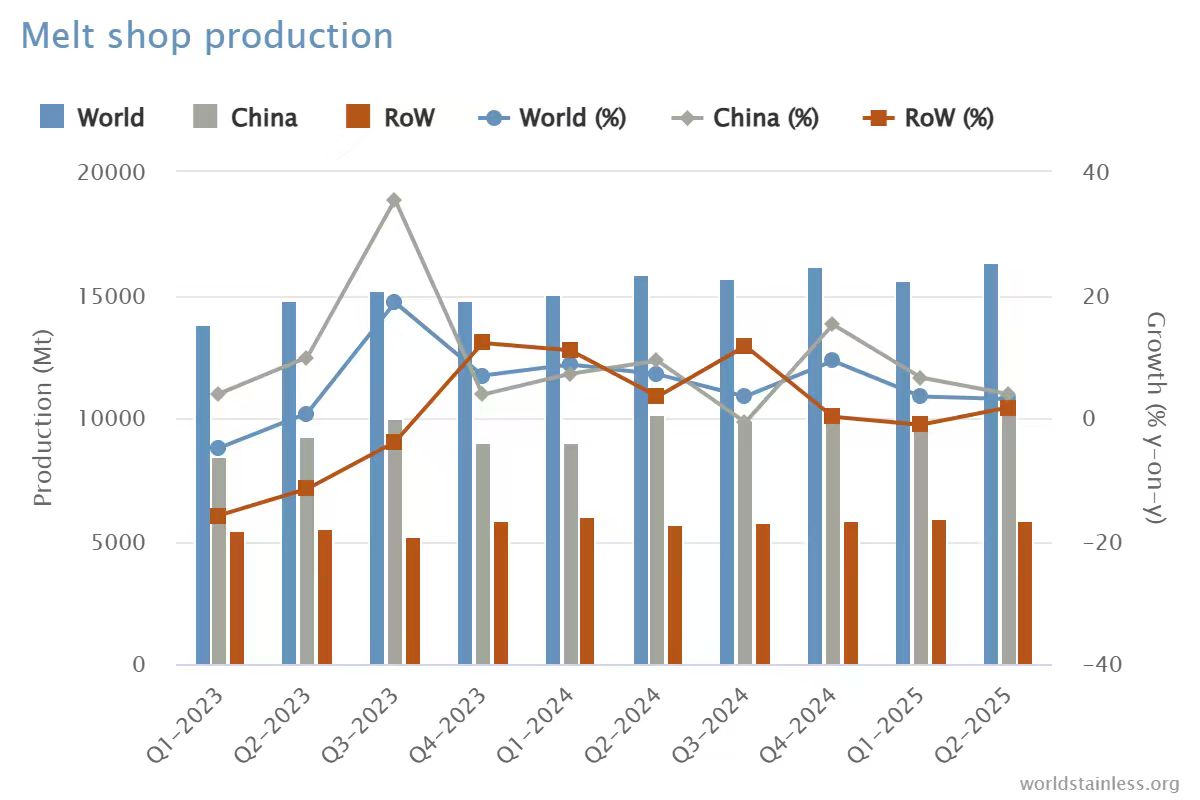

World Stainless Association: Global crude stainless steel output rose both year-on-year and quarter-on-quarter in Q2.

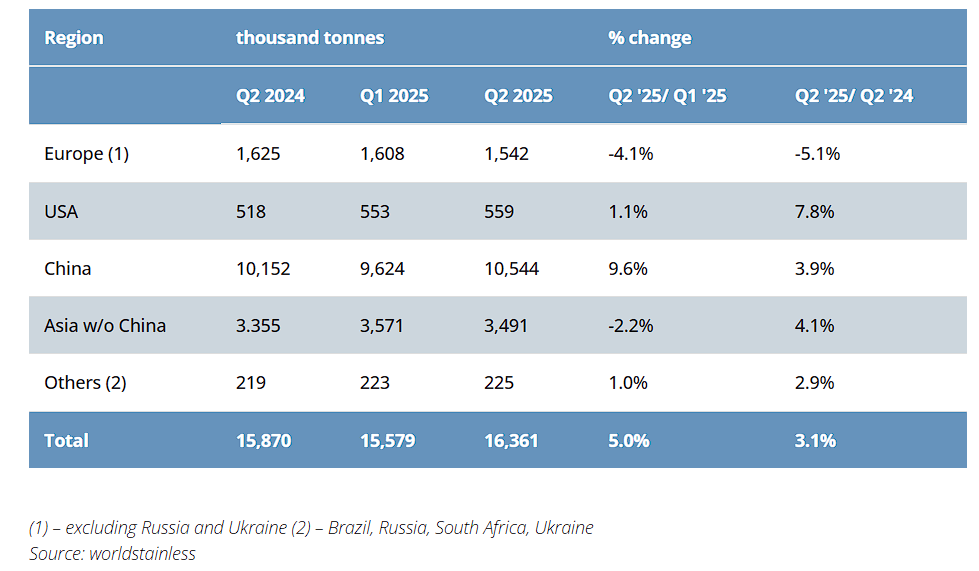

The World Stainless Association released global crude stainless steel output data for Q2 2025. Production totaled 16.361 million tons, up 3.1% year-on-year and 5% quarter-on-quarter.

Europe: 1.54 million tons, down 5.1% y/y and 4.1% q/q.

United States: 559,000 tons, up 7.8% y/y and 1.1% q/q.

Asia (excluding China and Korea): 3.49 million tons, up 4.1% y/y and down 2.2% q/q.

China: 10.54 million tons, up 3.9% y/y and 9.6% q/q.

Other countries (including Ukraine, Brazil, South Africa, Indonesia, Korea, and Russia): 225,000 tons, up 2.9% y/y and 1% q/q.

South Korea has imposed temporary anti-dumping duties on hot-rolled stainless steel coils from China and Japan

South Korea’s Ministry of Economy and Finance has imposed temporary anti-dumping duties on hot-rolled coils (HRC) made of carbon and alloy steel from China and Japan. This was reported by Mysteel Global.

The temporary duties will be imposed for a period of four months, starting September 1st.

The temporary anti-dumping duty rates range from 31.58% to 33.57% for Japanese companies and from 28.16% to 33.1% for Chinese companies.

The investigation was launched in March this year based on a petition filed by Hyundai Steel. The latter claimed that HRC from China and Japan was sold at dumping prices, which caused damage to the local industry.

In July, the South Korean Trade Commission (KTC) recommended that the Ministry of Economy and Finance impose preliminary anti-dumping measures on imports of Chinese and Japanese hot-rolled steel.

Vietnam imposed anti-dumping duties ranging from 23.10% to 27.83% on certain hot-rolled steel products originating in China after the expiry of a similar provisional tariff. The duties, which came into force on July 6, will apply for five years. Vietnam launched an anti-dumping investigation in July 2024 following complaints from local producers.

As GMK Center reported earlier, Taiwan imposed temporary anti-dumping duties on certain types of hot-rolled flat products from China for a period of four months. They came into effect on July 3 this year.

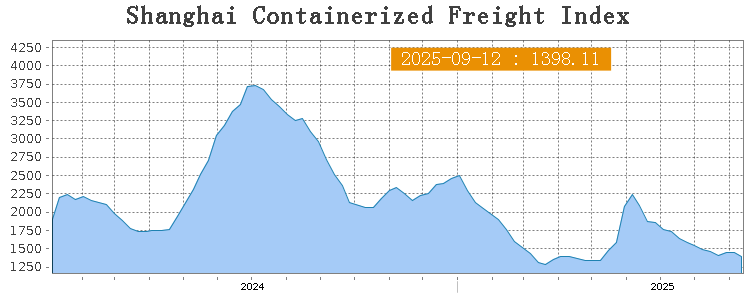

SEA FREIGHT | Market Largely Stable, Most Routes See Rate Declines

On September 12th, the Shanghai Containerized Freight Index (SCFI) fell 3.2% at 1398.11 points.

Europe/ Mediterranean:

Data from Customs showed China’s exports to Europe rose 10.4% year-on-year in August, with growth momentum continuing to accelerate. In the first eight months, the EU remained China’s second-largest trading partner, with total bilateral trade up 4.3% year-on-year, accounting for 13.1% of China’s total trade, reflecting steady improvement in China-EU trade. Last week, transport demand lacked fresh momentum, with supply-demand fundamentals offering limited support, leading freight rates to continue adjusting downward.

On September 12th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1154/TEU, which decreased by 12.2%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$1,738/TEU, which dipped 11.8% from the previous week.

North America:

Data from the U.S. Department of Labor showed that U.S. non-farm payrolls increased by 22,000 in August, well below market expectations, with the unemployment rate rising to 4.3%, the highest since 2021, signaling significant labor market weakness. In contrast to the steady growth of China-EU trade, China-U.S. trade has diverged, with China’s exports to the U.S. falling by more than 30% year-on-year in August. The outlook for the China-U.S. shipping market remains challenging. Last week, transport demand held steady, pushing market freight rates higher.

Last week, transport demand continued to lack upward momentum, and freight rates in most trade lanes adjusted downward.

On September 12th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$2,370/FEU and US$3,307/FEU, reporting 8.3% and 7.6% growth respectively.

The Persian Gulf and the Red Sea:

On September 12th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf plunged 16.2% to US$1273/TEU.

Australia & New Zealand:

On September 12th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand lost 4.1% to US$1259/TEU.

South America:

On September 12th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports decreased by 5.7% to US$3018/TEU.

JINLING METALS is dedicated to providing insightful market news and prices to assist you in making the RIGHT purchase decision. There are many market changes in China that you cannot reach anytime, and JINLING METALS is your eyes and ears in China's stainless steel market, catching, summarizing, and conveying the valuable information for you - who are a stainless steel expert or stakeholder like us. You are always welcome to talk and consult with us. :)