Stainless Insights in China from September 15th to September 28th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,085 | -3 | -0.14% |

| Foshan | 2,130 | -3 | -0.14% | ||

| Hongwang | Wuxi | 1,975 | -14 | -0.76% | |

| Foshan | 2,010 | -3 | -0.15% | ||

| 304/NO.1 | ESS | Wuxi | 1,920 | -9 | -0.47% |

| Foshan | 1,930 | -7 | -0.39% | ||

| 316L/2B | TISCO | Wuxi | 3,825 | -20 | -0.54% |

| Foshan | 3,870 | -11 | -0.30% | ||

| 316L/NO.1 | ESS | Wuxi | 3,660 | -38 | -1.08% |

| Foshan | 3,695 | 0 | 0.00% | ||

| 201J1/2B | Hongwang | Wuxi | 1,255 | -10 | -0.87% |

| Foshan | 1,265 | -3 | -0.25% | ||

| J5/2B | Hongwang | Wuxi | 1,155 | -10 | -0.95% |

| Foshan | 1,165 | -3 | -0.27% | ||

| 430/2B | TISCO | Wuxi | 1,205 | 6 | 0.53% |

| Foshan | 1,210 | 3 | 0.26% |

TREND | Stainless Steel Futures Weaken, Spot Prices Hold Firm

Stainless steel futures prices fluctuated weakly last week. At the beginning of the week, futures traded within a narrow range, but fell sharply with heavy volume later in the week, breaking below the previous trading band. Both trading volume and open interest in the main stainless steel futures contract declined compared with last week. With the “Golden September” peak season nearing its end and the China National Day holiday approaching, seasonal demand recovery has been limited, cooling stainless steel market sentiment. As of September 26, the main stainless steel futures contract closed at US$1,950/ton, up US$12.8/MT from last week, a gain of 0.71%.

Stainless steel 300 Series: Inventory Continues to Rise, Watch Pre-Holiday Restocking

Last week, Stainless steel 304 market prices edged down. As of Thursday, the mainstream base price for private cold-rolled four-foot Stainless steel coils in Wuxi US$1,935/ton, while private hot-rolled stainless steel prices stood at US$1,920/ton, both down US$7/ton from last week.

Stainless steel 200 Series: Futures Mixed, Spot Follows Adjustment

Prices for stainless steel 201 showed mixed performance. Early in the week, futures rose before retreating, dragging spot prices lower. Cold-rolled stainless steel 201J2 coils were mainly transacted at US$1,080/ton. On Thursday, boosted by a rebound in futures, traders lifted offers by US$7/ton to US$1135/MT, but downstream buyers resisted higher prices, limiting transactions. By Friday, as stainless steel futures retreated, stainless steel spot prices returned to around US$1125/MT. Both cold-rolled stainless steel and hot-rolled stainless steel inventories saw small increases.

Stainless steel 400 Series: Mill Deliveries Rise, Inventory Turns from Decline to Increase

Prices for stainless steel 430 remained stable last week. As of Friday, Wuxi spot prices for cold-rolled stainless steel 430 were US$1,175–1,185/ton, while hot-rolled prices stayed at US$1,025/ton, both unchanged from last week. Increased arrivals from mills added to the available supply, and with futures fluctuating, downstream demand cooled, leading to a small inventory build.

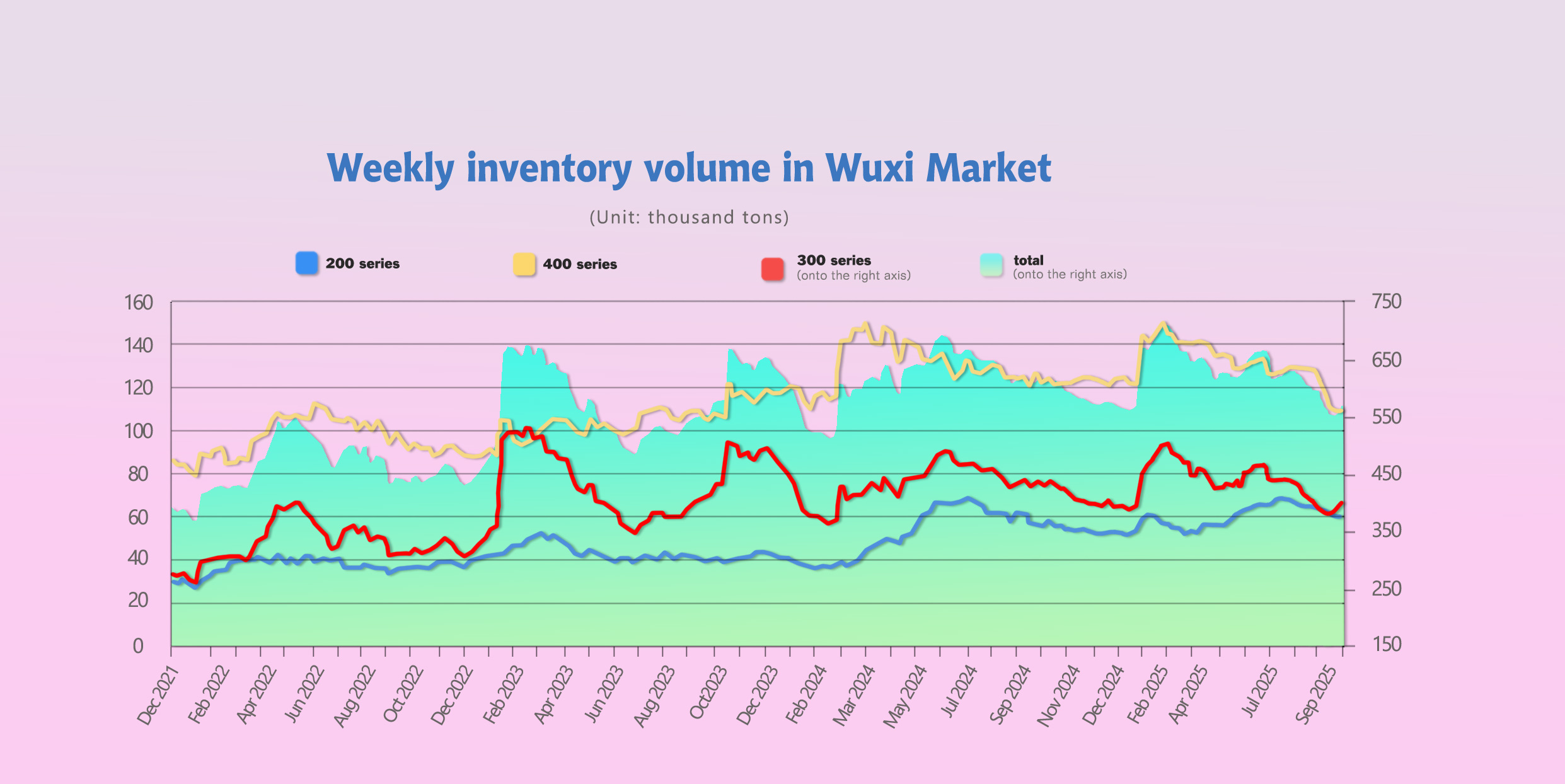

INVENTORY | Stainless steel Market Stocks Continue to Accumulate

As of September 25th, total Stainless steel inventory in Wuxi sample warehouses increased by 6,946 tons to 568,622 tons.

Breakdown:.

Stainless steel 200 Series: 428 tons up to 60,110 tons.

Stainless steel 300 Series: 5,716 tons up to 399,275 tons.

Stainless steel 400 Series: 802 tons up to 109,237 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Sep 18th | 59,682 | 393,559 | 108,435 | 561,676 |

| Sep 25th | 60,110 | 399,275 | 109,237 | 568,622 |

| Difference | 428 | 5,176 | 802 | 6,946 |

Stainless steel 300 Series: Continued Arrivals, Inventories Build Up

Wuxi 300-series inventory increased by 5,700 tons last week (cold-rolled stainless steel up 3,900 tons, hot-rolled stainless steel up 1,800 tons), bringing the total to 399,300 tons. Recent arrivals of Indonesian Yongwang, Xinhai, and Tsingshan resources significantly boosted supply. Cold-rolled stainless steel 304 inventories rose due to abundant arrivals, while tightness in hot-rolled supply eased. However, certain specifications remain in shortage. Despite the traditional peak season, downstream demand recovery has been weaker than expected, leading to continued stock accumulation.

Stainless steel 200 Series: More Available Supply, Slight Inventory Build

Wuxi stainless steel 200-series inventory increased by 400 tons last week to 60,100 tons (cold-rolled up 300 tons, hot-rolled up 100 tons).

1. Cold-rolled five-foot resources from Hongwang accumulated slightly, adding to the circulating supply.

2. Prices turned weaker midweek, trading sentiment was poor, and inventories edged up.

Spot prices for 201 mainly declined last week, and market caution grew. With the upcoming holidays, some restocking demand may emerge, but actual performance will depend on downstream transactions.

Stainless steel 400 Series: More stainless steel Mill Arrivals, Small Inventory Increase

Wuxi Stainless steel 400-series inventory increased by 800 tons last week to 109,200 tons (cold-rolled Stainless steel up 600 tons, hot-rolled Stainless steel up 200 tons).

1. End-of-month arrivals from JISCO and TISCO boosted the circulating supply.

2. Some pre-holiday restocking occurred, but overall demand was still based on rigid needs, and destocking lagged behind expectations.

With holidays approaching, stainless steel mills are entering a concentrated delivery cycle. Inventories in Wuxi are expected to continue building next week, with market attention focused on mill production schedules and transaction activity.

RAW MATERIAL | Chromium Ore Imports Remain Low in August, Upward Pressure on Ferrochrome Prices Continues.

Costs: Last week, mainstream high-carbon nickel ferrochrome ex-factory prices held steady at US$135/nickel point. Ferrochrome prices rose to US$1210/50 reference ton, while mill production remains unprofitable.

1. China’s Ferrochrome Imports Fell in August, Domestic Supply Gap for Raw Material Persists

In August 2025, China imported a total of 159,100 tons of high-carbon ferrochrome, down 29.9% month-on-month and 43.4% year-on-year. Imports from South Africa accounted for 60,900 tons, down 43.9% month-on-month.

The decline in imported ferrochrome has impacted steel mill procurement. Prior inventory consumption and limited domestic supply support upward price movement.

2. Stainless Steel Mill Procurement Prices Rise by US$28, Downstream Faces Pressure

Fueled by prior bullish sentiment in ferrochrome retail prices, many market steel tenders were expected to rise. However, this US$28 increase was lower than some mill expectations, mainly because stainless steel prices did not see significant gains from the “Golden September” effect. Meanwhile, nickel prices have also risen, putting procurement pressure on stainless steel and limiting raw material price increases, leading to only moderate rises in mill purchase prices.

3. Supply-Demand Gap Supports Profit Improvement

Based on monthly high-carbon ferrochrome balance calculations (excluding national stockpiles for 2025), cumulative ferrochrome shortages from January to September 2025 amounted to approximately 176,600 tons. Short-term imports cannot cover this gap, and new capacity this year is limited. Moving forward, the supply-demand gap is expected to continue supporting ferrochrome profitability into the last quarter.

SUMMARY | Stainless Steel Producers Restart, Put Stainless Steel Prices Under Pressure

Current stainless steel support primarily comes from raw material costs. However, as mill production ramps up, supply-side pressure is expected to intensify. With the traditional peak season now more than halfway through, attention is on downstream demand recovery and whether policies providing sufficient support will be introduced.

Stainless steel 300 Series: Overall, domestic demand recovery is slow, and external demand remains uncertain. With ongoing downward pressure on real estate, slower home appliance production growth, and uncertain export momentum, October stainless steel consumption is expected to remain stable month-on-month. Overall prices may continue in a range-bound pattern, with downside support largely dependent on raw material costs. Close attention should be paid to policy signals and inventory trends.

Stainless steel 200 Series: Last week, copper prices rose significantly due to raw material supply constraints, strengthening cost support. However, after the stainless steel 201 spot price increase, market acceptance was limited, and transactions remained moderate. Influenced by futures volatility, spot prices reverted to around US$1125. Macro sentiment remains moderately bullish, and some pre-holiday stockpiling may occur. Tracking subsequent transactions, stainless steel 201 prices are expected to remain stable in the short term.

Stainless steel 400 Series: High-chrome raw material prices rose slightly last week. Combined with continued increases in October high-chrome steel tender prices, cost support for Stainless steel strengthened. With the National Day holiday approaching, some downstream buyers began modest pre-holiday restocking, though overall transactions remain based on rigid demand. Given firm raw material prices providing strong cost support, stainless steel 430 prices are expected to maintain moderately strong performance in the short term.

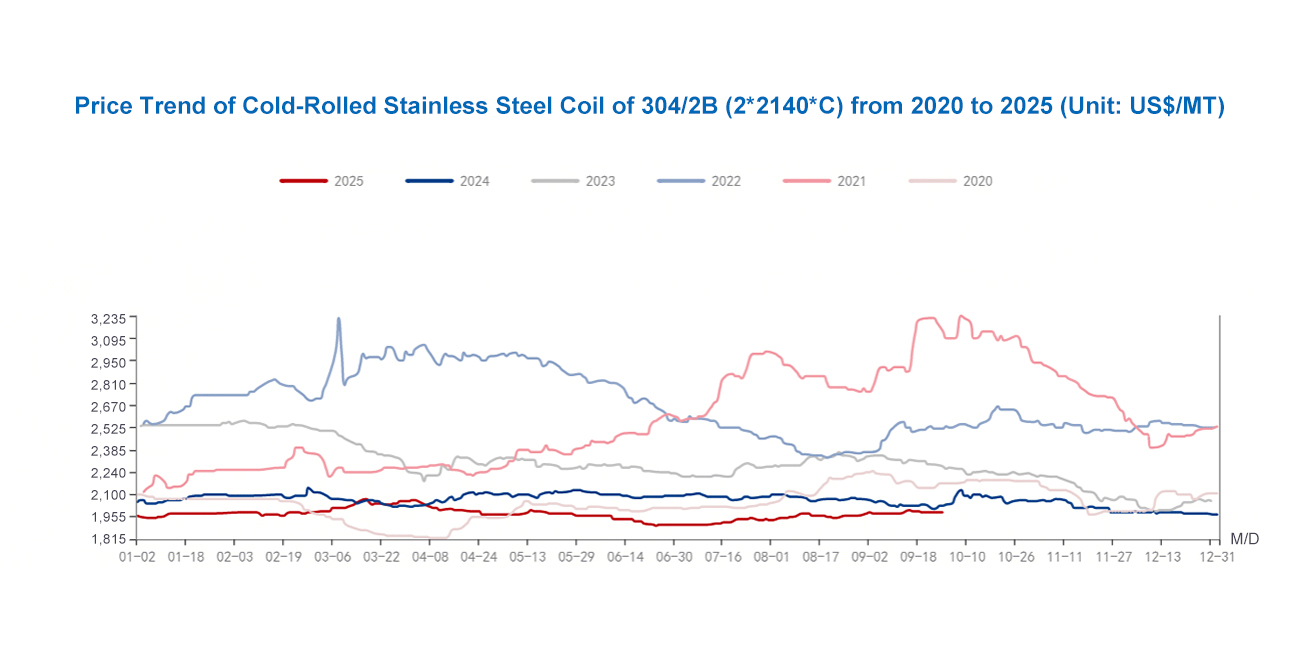

MACRO | Review & Outlook of Price Changes for Cold-Rolled Stainless Steel 304 from 2020 to 2025

Five Years of Price Fluctuations: From Pandemic Shock to a Return to Rationality

Over the past five years, cold-rolled stainless steel 304 (CRSS304) has experienced a complete market cycle. From the impact of the pandemic in early 2020 to the price peaks of 2021-2022, and then to a return to rationality after 2023, the stainless steel market has undergone a profound adjustment driven by a complex mix of factors.

The price peak occurred between 2021 and 2022, with Foshan Hongwang's CRSS304 price reaching a historic high of US$2,835-3,120/ton. This unusual market trend was primarily driven by two factors: a robust recovery in the manufacturing industry following the easing of global pandemic controls, and a broad-based rise in the prices of raw materials and energy such as nickel and chromium.

Starting in 2023, the market landscape shifted, with prices falling back to the US$1,975-2,405/ton range and continuing to fluctuate at a low level. Diverging and shifting demand, high transportation costs, and inflationary pressures gradually offset the cost-side support. Entering 2025, policy factors became the new market dynamics. The rise of global trade protectionism and China's implementation of its anti-involutionary and growth-stabilizing policies jointly shaped a new pricing dynamic.

Year-by-Year Evolution: Drivers and Market Reactions

2020: An Abnormal State Under the Impact of the Pandemic

Global stainless steel production dropped to around 50.9 million tons. The pandemic lockdown resulted in decreased downstream demand and logistics disruptions. Prices were generally under pressure; however, proactive capacity adjustments helped prevent an extreme collapse.

2021: A Retaliatory Rebound in Stainless Steel Prices

Global production quickly recovered to 56.3 million tons. Demand from manufacturing and infrastructure was concentrated, and coupled with raw material costs, prices for cold-rolled 304 stainless steel entered a rapid upward trend, reaching a new high.

2022: Geopolitical Impact Pushed Up Material Cost

The Russia-Ukraine conflict triggered an energy crisis, and raw material and logistics costs remained high, with the European market being particularly hard hit. Global production fell slightly to 55.3 million tons, with prices fluctuating widely at high levels and regional disparities widening significantly.

2023: A Year of Rational Return and Stainless Steel Prices stabilized

Market demand is structurally diverging, with differing paces of recovery on the engineering and consumer sides. Global production rebounded to 58.4 million tons, prices retreated from highs, and the market entered a phase of supply and demand rebalancing.

2024: Demand Fell Short while Stainless Steel Supply Rose

Global production further increased to 62.6 million tons, with China accounting for the majority of the rise. Although events such as the Red Sea incident pushed up some transportation costs, demand failed to keep pace, and prices continued to consolidate in a mid-to-low range.

2025: Policy Shifts will Shape the Stainless Steel Market in China

In the first half of 2025, global stainless steel production continued to grow strongly, reaching a total of 31.94 million tons. At the same time, China's industrial policy underwent a major shift—from prioritizing production to stabilizing growth, preventing internal competition, and prioritizing quality and high-end development.

The "Steel Industry Stable Growth Work Plan (2025-2026)" issued by the Ministry of Industry and Information Technology and five other ministries, along with the "anti-involutionary" guidance implemented by various regions, signals a profound shift in industry governance. The policy direction has clearly shifted from scale expansion to quality improvement, bringing new uncertainties to the cold-rolled stainless steel 304 market.

Q4 2025 Price Forecast: Three Scenario Analysis

Based on the current market price (approximately US$1,975-2,115/ton in the first half of 2025), combined with production control and policy impacts, the following price trends are predicted for Q4 2025:

Neutral Scenario (Highest Probability)

Policy support and export restrictions offset each other, leading to a slow upward trend or continued consolidation in the US$2,045-2,260/ton range. In this scenario, limited domestic supply provides a floor for prices, but weak end-user demand constrains upward momentum.

Optimistic Scenario

Strict policy implementation coupled with a rebound in demand could push prices towards US$2,260-2,545/ton in the short term. This scenario requires stronger-than-expected policy implementation and a significant improvement in demand from the manufacturing and construction sectors.

Pessimistic Scenario

Longer policy implementation or continued weak demand could lead to a price decline to the US$1,755-2,045/ton range. However, considering the obvious intention of policy support, the probability of a major price collapse is low.

Strategic Implications: Seizing Structural Opportunities from Price Fluctuations

For companies in the stainless steel supply chain, future market opportunities will arise more from structural adjustments rather than cyclical fluctuations. Short-term strategies should focus on opportunities arising from policy-driven supply contractions. China's production cap will limit downward pressure on cold-rolled stainless steel 304 prices, and the spot market may see a slight upward trend driven by tight delivery schedules. Jinling Metals will continue to closely monitor inventory and delivery schedules, seize market opportunities, and provide optimal stainless steel raw material solutions to global buyers.

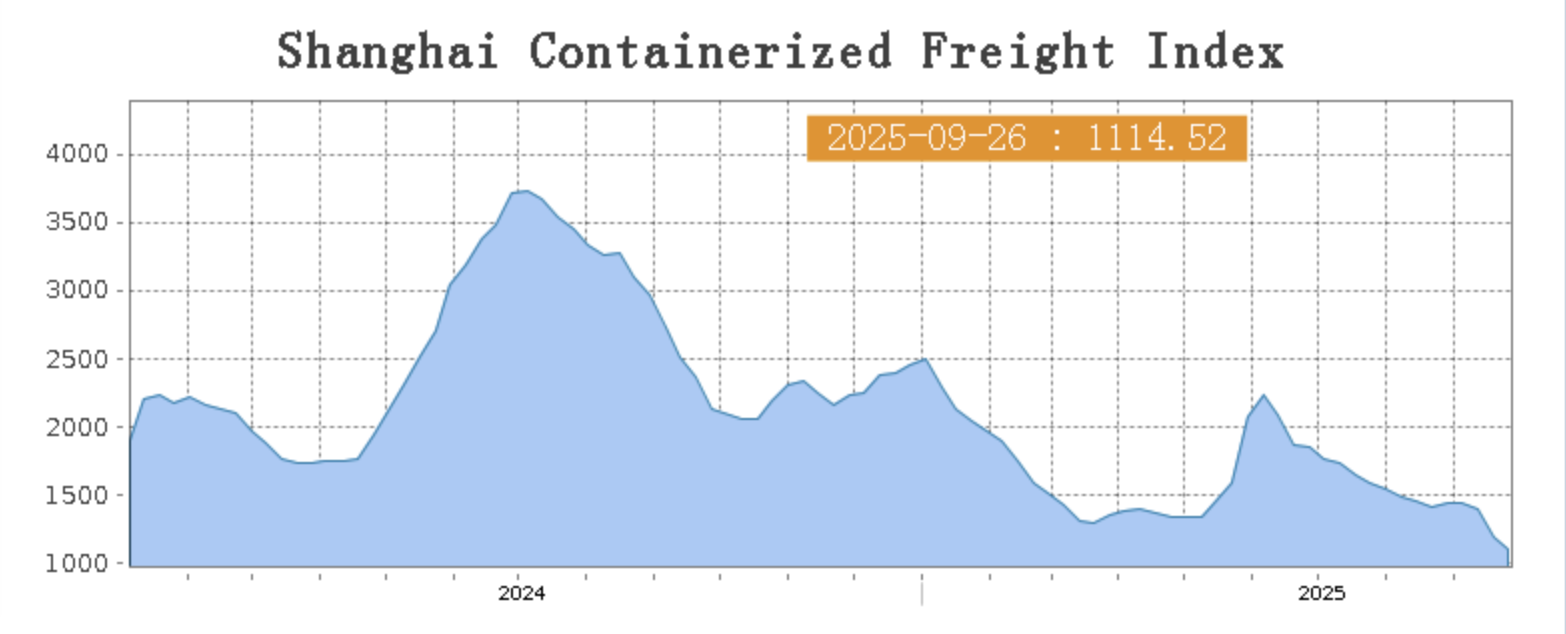

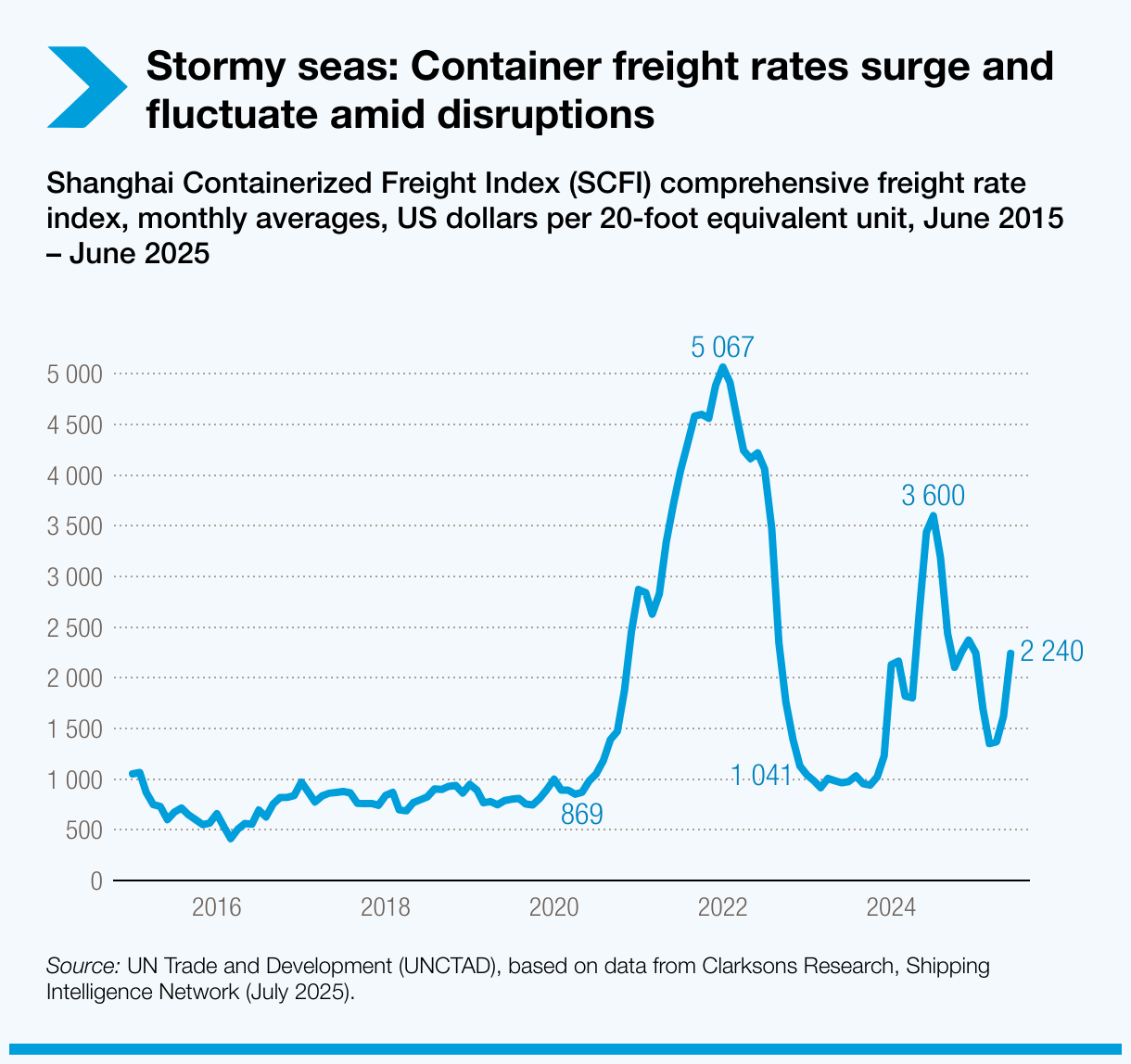

SEA FREIGHT | The global maritime trade saw its slowest growth in recent years in 2025, at only 0.5%.

Weakening demand for China's export container shipping has led to a continued adjustment in freight rates on long-haul routes, and the composite index remains on a downward trend. On September 26th, the Shanghai Containerized Freight Index (SCFI) fell 7% to 1114.52 points.

Europe/ Mediterranean:

Recent lackluster economic data from Europe indicates a lack of momentum in the transportation market's demand growth. Last week, the weak supply and demand fundamentals caused spot market booking prices to continue to fall.

On September 26th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$971/TEU, which decreased by 12.2%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$1485/TEU, which dipped 9.3% from the previous week.

North America:

Last week, transport demand continued to lack upward momentum, and freight rates in most trade lanes adjusted downward.

On September 26th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$1460/FEU and US$2385/FEU, reporting 10.8% and 6.7% loss, respectively.

The Persian Gulf and the Red Sea:

On September 26th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf plunged 14.9% to US$843/TEU.

Australia & New Zealand:

On September 26th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand lost 5.6% to US$1093/TEU.

South America:

On September 26th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports decreased by 14.6% to US$2133/TEU.

Maritime trade is set to slow to 0.5% in 2025

International maritime trade

Global seaborne trade is under pressure. After a modest 2.2% growth in 2024, maritime trade is set to slow to 0.5% in 2025, before averaging 2% annually over the 2026–2030 period.

By May 2025, tonnage through the Suez Canal was still 70% below 2023 levels. The Strait of Hormuz, through which 11% of global trade and a third of seaborne oil trade flow, also faces disruption risks. Rerouting onto longer routes increased carbon emissions from shipping in 2024.

Shipping lanes under strain

Rerouting’s climate cost: Longer routes have increased carbon emissions

New trade tariffs in the United States and elsewhere have added complexity. For developing economies, shifting routes could generate transshipment opportunities for some ports, but could also increase shipping costs.

By January 2025, the world fleet counted 112,500 vessels with 2.44 billion deadweight tons. Greece, China, and Japan control over 40% of capacity, while nearly 50% of capacity is registered in just three flag states – Liberia, Panama, and the Marshall Islands.

Fleet renewal, safe ship recycling, global rules on greenhouse gas emissions control, and skilled labour are key to a timely and just transition to low-carbon shipping.

Freight rates and maritime transport costs

Freight rate volatility has become the new normal. Container, bulk, and tanker freight rates have remained elevated and volatile in 2024 and 2025, swinging sharply amid geopolitical tensions, trade policy shifts, and supply–demand imbalances. This instability is driving up global trade costs.

Rerouting ships has lengthened voyages, cut effective capacity, and raised operating costs. Container shipping was hit hard with spot and charter rates nearing COVID-19 peaks by mid-2024 before easing, but still far above pre-crisis levels. Volatility has continued in 2025, amid new tariffs and the risk of disruptions in the Strait of Hormuz.

Dry bulk freight rates surged in 2024 on the back of strong coal, grain, and fertilizer demand, Red Sea rerouting, and limited fleet growth, before softening in 2025. Tanker markets, reflecting their sensitivity to geopolitical factors, were marked by volatility, with rates spiking in June 2025.

SOURCE: https://unctad.org/publication/review-maritime-transport-2025