Stainless Insights in China from April 28th to May 4th.

TREND || Down by 30! High-Nickel Pig Iron Latest Tender Price at 940, Stainless Steel Futures and Spot Markets Remain Steady

On the first trading day after the Labor Day holiday, stainless steel futures showed a slightly bullish trend with fluctuations. Prices climbed intraday to a high of US$1905/MT, touching the 20-day moving average. By the close of the afternoon session, the main stainless steel futures contract had risen by US$7.6/MT to US$1895/MT, an increase of 0.43%. Shanghai nickel also experienced a mild upward fluctuation, with the main contract closing up US$83/ton at US$17645/MT, an increase of 0.48%.

In the spot market, mainstream prices for private 304 cold-rolled four-foot coils in Wuxi were quoted at US$1885/MT, and hot-rolled coils at US$1880/MT — both unchanged from pre-holiday levels. Spot market transactions remained stagnant, inventories saw a slight buildup, and given continued macroeconomic uncertainties, most traders maintained stable offer prices in the morning.

As for mill pricing: This week, Delong (Xiangshui) in the Wuxi market priced 304 cold-rolled coils at US$1920/MT, flat compared to pre-holiday levels, with rebate policies yet to be announced. Similarly, in the Wuxi market, Liyang opened with four-foot and five-foot 304 cold-rolled coils both priced at US$1920/MT, and 304 hot-rolled coils at US$1905/MT — also unchanged from before the holiday, with rebate details pending.

Regarding market transactions, overall spot trading was moderate today. Some low-priced resources saw relatively better sales, and downstream end-users mainly purchased based on immediate needs. However, with a significant drop in steel mill high-nickel pig iron tender prices, the market has grown increasingly concerned about potential future price declines.

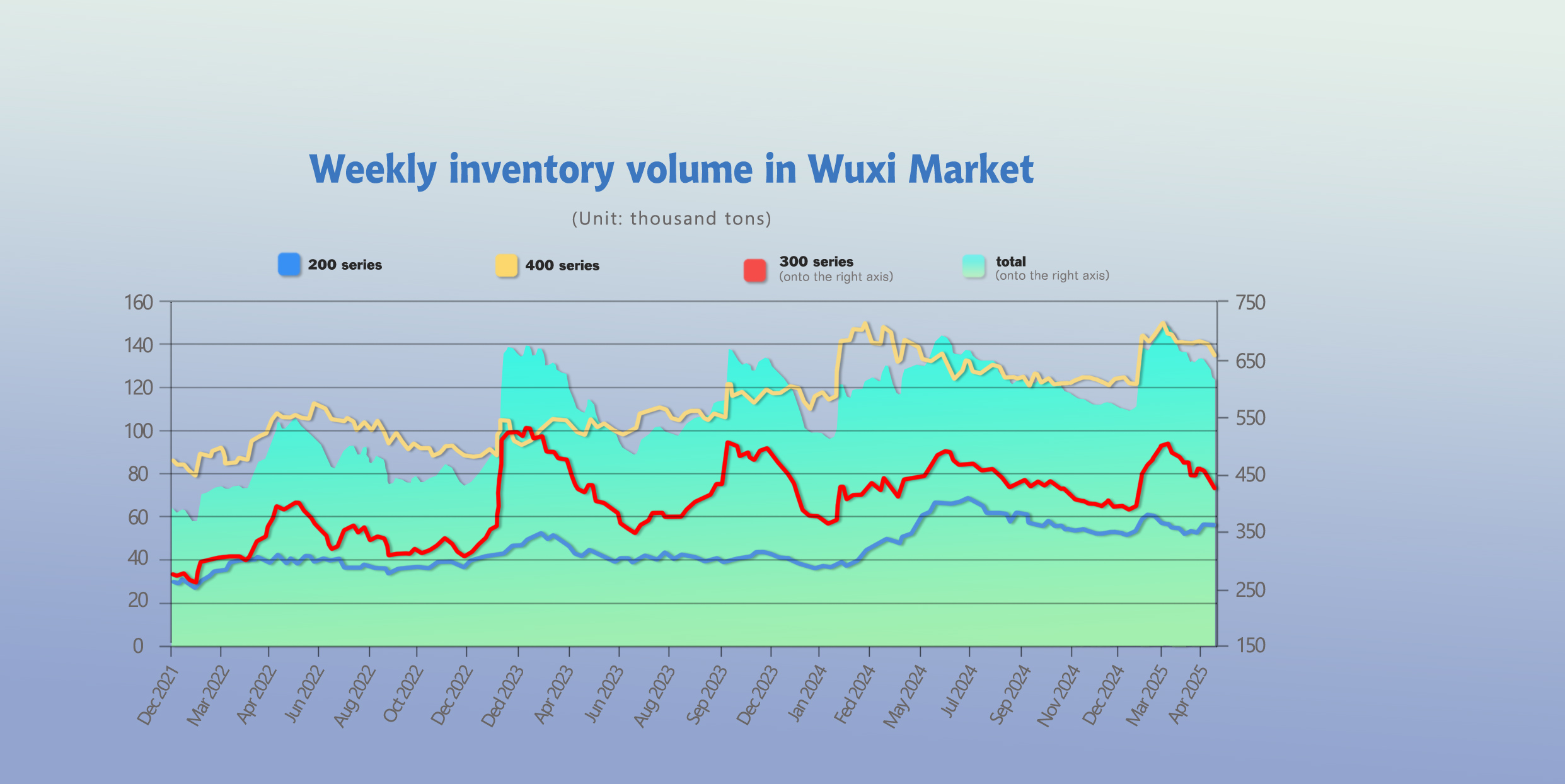

INVENTORY || Down 2.81%! Mills Halt Offers Before Holiday to Push Prices, Spot Market “Steady as a Rock”

As of April 30th, total inventory in Wuxi sample warehouses decreased by 17,548 tons to 605,950 tons. Breakdown:

200 Series: 642 tons down to 54,818 tons.

300 Series: 12,500 tons down to 418,452 tons.

400 Series: 4,406 tons down to 132,680 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Apr 24th | 55,460 | 430,952 | 137,086 | 623,498 |

| Apr 30th | 54,818 | 418,452 | 132,680 | 605,950 |

| Difference | -642 | -12,500 | -4,406 | -17,548 |

200 Series: Ongoing Shortages, Slight Inventory Drawdown

From the perspective of spot inventory structure, normal arrivals continued before the Labor Day holiday. During the week, the shortage of 201J2 cold-rolled thin-gauge materials slightly eased, but specifications like 0.29, 0.3, 0.38, and 0.48 mm remained at low levels. 201 cold-rolled spot prices were further reduced, with some traders offering May futures at a base price of US$1090/MT to move inventory. Buyers opted for lower-priced resources, leading to a week-on-week increase in transactions. 201 hot-rolled prices remained stable throughout the week, and downstream demand was released intensively before the holiday, resulting in a slight inventory drawdown. Due to semi-stagnant trading over the holiday and continued normal arrivals, traders cut prices to sell. After the holiday, 200 series inventory may see a small accumulation. Attention should be paid to upcoming mill pricing and overall market transaction trends.

300 Series: Lower Arrivals, Pre-Holiday Restocking Increases

Looking at the spot inventory structure, arrivals of hot-rolled materials in Jiangyin continued to decline, while TISCO cold-rolled stock also dropped slightly, easing market supply pressure. Pre-holiday demand release and speculative restocking led to accelerated inventory digestion.

Before the holiday, futures and spot prices remained low, and more low-priced resources entered the market. Downstream buyers seized the opportunity to purchase at lower prices, gradually digesting these resources. Overseas macro sentiment improved, boosting market confidence. During the week, TISCO suspended offers to stimulate consumption, resulting in better sales during certain periods and inventory drawdown.

With domestic and overseas macroeconomic factors intensifying and expectations rising for interest rate and reserve requirement ratio cuts, market investment sentiment improved. Steel mill production schedules fell slightly, easing supply-side pressure. However, demand remained weak and overcapacity persisted, with no significant improvement. After the holiday, inventories may slightly accumulate.

400 Series: Strong Cost Support, Active Trading Leads to Inventory Decline

Based on spot inventory structure, before the Labor Day holiday, both TISCO’s hot-rolled and cold-rolled spot inventories showed noticeable declines. JISCO’s cold-rolled stock also saw a sharp reduction, leading to a significant overall inventory decrease.

Before the holiday, just-in-time demand from downstream buyers for 400 series remained stable, and market transactions were relatively active. Coupled with fewer mill arrivals, 400 series spot inventory was rapidly drawn down. On the raw material side, high-chrome retail market prices trended weak to stable, but with major steel mills raising May purchase prices by US$70/50 reference ton, cost support for stainless steel remained.

As the holiday approached, downstream procurement slowed. It is expected that next week spot inventory will show slight fluctuations, and 400 series stock may rebound. As of April 30, 430 cold-rolled prices remained weak, downstream demand was stable, and inventory clearance accelerated. Cost support remained in place, but with expectations of a potential drop in high-chrome prices ahead, attention should be given to how raw material price changes might affect 430 prices.

RAW MATERIAL || Market Recovering After Holiday, Risk of Price Decline in May Increases!

Following the Labor Day holiday, the high-chrome market remains cautious. According to industry feedback, mainstream ex-factory prices are mostly unchanged from pre-holiday levels, holding steady at around US$1145-US$1173/50 reference ton.

In terms of costs, the current price of 40–42% South African chrome ore remains stable at US$8.5/MT, while 40–42% Turkish lump ore holds at approximately US$8.9/MT—both flat compared to pre-holiday levels.

In May, Tsingshan Group raised its high-chrome purchase price by US$70/50 reference ton, setting the price at US$1130/50 reference ton. However, retail prices in the high-chrome market declined slightly afterward. With more producers resuming production recently, retail prices have shown no clear signs of recovery and continue to trend weakly stable.

Apart from Tsingshan, representative northern steel mills have not yet released their May purchase prices for high-chrome. Still, the market expects pricing to be around US$1103/50 reference ton. Taking current chrome ore and coke costs into account, most high-chrome producers remain in a loss-making position. However, compared to April, losses have narrowed significantly, leading to a rapid rebound in output.

In the short term, high-chrome retail prices remain under pressure. On one hand, the market supply has increased sharply, making it difficult for prices to recover. On the other hand, the negative impact of tariffs on the stainless steel sector persists, spilling over into the raw materials market. Therefore, retail prices of high-chrome are expected to stay weak to stable, with an increasing risk of further decline.

As of May 6, mainstream domestic high-nickel iron ex-factory prices stood at US$134-US$136/nickel point, unchanged from pre-holiday levels. In the morning, a South China Q Steel Mill issued a tender at US$131/nickel point (tax-included, warehouse bottom), with delivery scheduled for late May. It is reported that a total of 40,000 tons were traded in this tender—30,000 tons supplied by Indonesian nickel iron producers and 10,000 tons by traders.

This round of tender prices is US$4.1/nickel point lower than the previous round, mainly aiming to lower the average price of long-term contracts this month and reduce raw material costs. At present, other mills are still inquiring in the nickel iron market at around US$135.4/nickel point, generally flat compared to pre-holiday levels.

Overall, macro sentiment has somewhat eased, but uncertainties remain. Transaction activity was stagnant during the May Day holiday, leading to increased inventories. Losses at the steel mill level continue to exert pressure on raw material prices. Stainless steel prices are expected to fluctuate, with attention focused on downstream restocking behavior and the pace of macro policy implementation.